Market:

The STI took a breather in August; it was down 1.6%. We remain Neutral, leaving our STI target at 3,270 (15x FY17e PE). We continue to see strong economic data across the globe. World economic growth is at 6-year highs. After a softer Apr-May, economic momentum is re-accelerating. We believe this will help sustain equity markets, despite many well-flagged fears. These include a potential Korean Peninsula conflict and a US government shut-down due to monetary tightening.

On Korea, the base case is that tensions could be elevated, but confrontation will be avoided. Any first strike by North Korea can only be deemed suicidal if we assume the regime’s objective is just to shore up its nuclear capabilities. Early signs of an imminent war will be an evacuation of residents or a movement of troops by the US (or even China).

Over in the US, with the Republican Party controlling both houses of Congress, we can only conclude that its debt ceiling will likely be passed. Albeit with plenty of political drama. The politicians are, after all, approving their own spending plans. We are less anxious about tightening by central banks. This is because they would only be responding to healthier economic data, not runaway inflation that requires a pre-emptive squeeze of monetary policy. In the coming 19-20 September Fed meeting, the market has pencilled in some form of balance-sheet tapering. Despite this high-probability event though, US Treasury yields have corrected to year lows.

Recommendation:

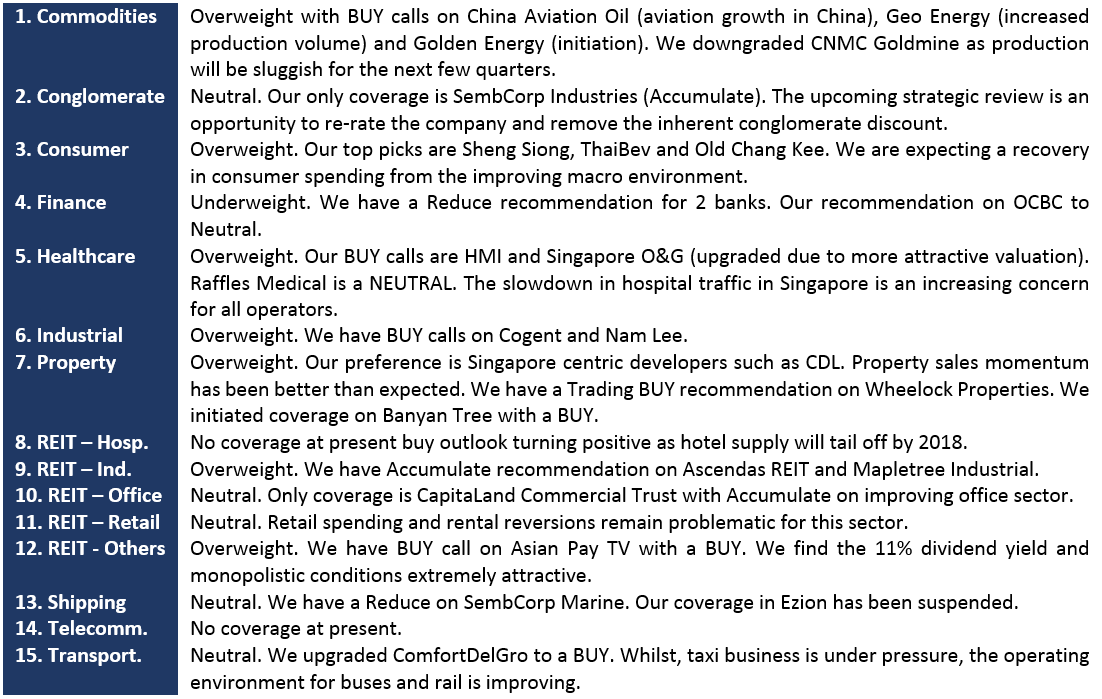

In August, we initiated coverage of Banyan Tree with a BUY. Its recent partnership with China Vanke and Accor opens up a large pipeline of hotel-management contracts for the next several years, at least. Both parties’ commitment to this partnership has even culminated in their acquisition of significant stakes in Banyan. We also initiated coverage of Singapore’s coal sector, with Buys on Golden Energy and Geo Energy. We think coal prices will stabilise in a range, which should be acceptable to the Chinese authorities.

We find Singapore-listed coal producers attractive as they are the fastest-growing in the region, with production expected to almost double in the next two years. Our other key picks for sustainable dividend yields are Asian PayTV, Mapletree Industrial Trust, Ascendas REIT and CapitaLand Commercial Trust.

Sector/Corporate:

Property sales in Singapore stayed buoyant. Average unit sales per month are now double of 2014-2016 levels. We keep our Overweight recommendation on the sector. Another important development is the rise of SIBOR, to an 18-month high. Higher interest rates, healthy capital markets and an improving economy would be potential re-rating catalyst. Hospitality appears to have turned around, with spikes in tourist arrivals and RevPAR in June. It is unclear at the moment whether this was a mere festive-season bump.

Technical Analysis : Straits Times Index – stuck in a correction with all eyes on 3195 support area

Source: Bloomberg, Phillip Securities Research Pte Ltd

Performance of the Straits Times Index (STI) in August 2017 was rather sluggish. It ended with an inside monthly bar, down 1.5% in August. That was partly due to the ongoing fears of conflict in the Korean Peninsula as North Korea recently tested a Hydrogen bomb that was five times greater than the atomic bomb used in World War 2.

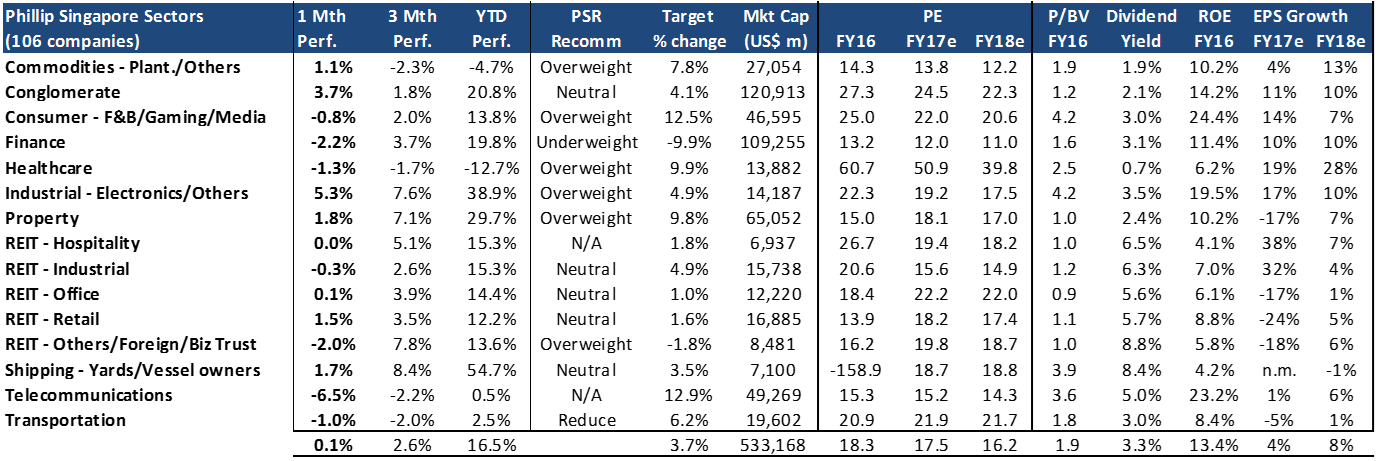

PHILLIP SINGAPORE SECTOR UNIVERSE

Best performing sectors in Aug17 were: Industrial, Conglomerate and Property. The gains in Industrial came from Hi-P (+38%) and Venture (+20%). Conglomerate rose on the back of Jardine Strategic (+7.5%). The Property sector increase was due to Guocoland (+25%). Major gainers under our coverage were Banyan Tree (+11.8%), CapitaLand Mall Trust (+8%) and F&N (+6.7%).

Worst performing sectors in Aug17 were: Telecommunication, Finance and REIT-Others. In Telecommunications, SingTel (-6.8%) and Starhub (-4.4%) led the losses. Finance weakness came from DBS (-4.6%). The decline in REIT-Others was due to Hutchinson Port (-4.2%). Major decliners under our coverage include Raffles Medical (-14.4%), 800 Super (-11.3%) and Hock Lian Seng (-10%).

SUMMARY OF SECTOR AND COMPANY VIEWS

For more in-depth news on the specific sectors, sign in to download the full report!

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.