Market: STI fell 3.2% in August, surrendering all its gains from the prior month. As we enter the 10th anniversary of the GFC, predicting the next crisis has been the foremost preoccupation of the media. The most interesting scenario mentioned has been higher interest rates and an economic slowdown sparked by a growing U.S. fiscal deficit. The positive impact of fiscal stimulus on the U.S. economy should wear out over the next two years. But this deficit spending will remain and the U.S. will need to borrow and sell even more Treasuries. To attract foreigners into buying these Treasuries, interest rates will need to rise, which will dampen economic growth. In turn, this will weaken the US dollar, negating the effects of higher rates on the dollar. A negative spiral will then ensue. Another notable concern is the side effects of quantitative easing. The wealthy have benefited from central-bank purchases of financial assets. This has widened the wealth gap and fuelled the rise of populist and nationalist-led regimes. The danger of such regimes is the higher chances of conflict within and between countries.

Two years is an eternity for most of us “investors”. Foreigners’ tolerance for U.S. government bonds despite a $1tr fiscal deficit will always be artificially high. The US dollar may be flawed, but it will be hard to lose its global reserve currency and trade settlement status unless a better liquid alternative is found. Therefore, for run on Treasuries to materialise, it needs to be accompanied by higher risk-free yields appearing out of Europe and Japan.

In Singapore, inflationary pressures are piling up. MAS core inflation in July was 1.9%. This was a 4-year high and at the upper end of the MAS’ 1-2% expectation. The bulk of the rise in July was due to a 12.5% spike in fuel and utilities. Electricity and water prices have risen 16.5% and 15% respectively this year. Next will be public-transport fares. The maximum increase is 4.3% next year. Our worry is the transmission of costlier fuel and utilities into the food index. The hawker and restaurant price indices carry a large 20% weight on core CPI and prices have been rather benign in the past two years. The MAS’ last policy statement in April signalled a rise in the slope of the NEER (we refer as SGD). Its next statement in October should at least see them maintaining modest and gradual appreciation. With the trade war looming larger and larger, Singapore’s still-nascent recovery and currency weakness across Asia, it may be too aggressive to raise the slope or even re-centre the band of the SGD.

Recommendation: The backdrop for equities in Singapore is turning weaker. News flow is negative as the trade spat worsens. And as we enter U.S. mid-term elections on 6th November, we expect the market to trade even more cautiously. Other economic conditions are not encouraging. We can expect emerging-market economies to weaken as their currencies get pummelled. The slightest signs of higher imports or weaker trade balances will result in the selling pressure on their currencies. Near-term solutions for emerging markets will be contracting consumption and raising interest rates. In developed countries, with the exception of the U.S., Europe and Japan are stuttering. Our position is to remain defensive.

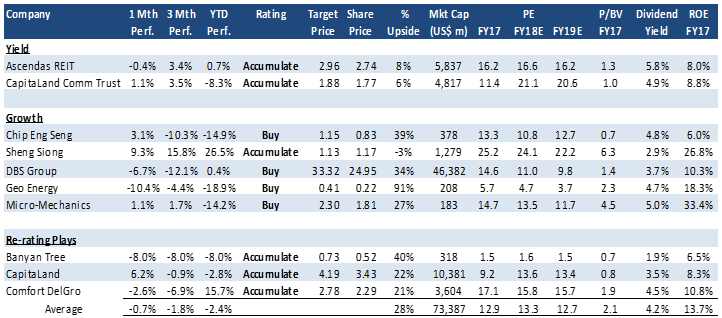

PHILLIP ABSOLUTE 10 – Our top 10 picks for absolute returns

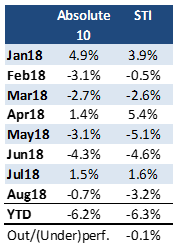

Source: Bloomberg, PSR. Phillip Absolute 10 performance assumes equal weight to every stock in the portfolio. Any change to Phillip portfolio is only conducted at month end. Performance of the portfolio and STI does not take into account gains from dividends.

HISTORICAL PERFORMANCE

Portfolio Review:

Our inaugural Phillip Absolute 10 Model portfolio began in January. It started well with a rise of 4.9% in January. Banyan Tree and CapitaLand led gains in January. DBS has been a significant contributor to our performance with a gain of 15% for the period of Jan-Feb18. We then switched to OCBC in March due to the higher upside to our target price and a beneficiary of higher interest rates (in particular through insurance business). In July we swapped out AsianPay TV, Dairy Farm and OCBC, with CapitaLand Commercial Trust, Sheng Siong and DBS.

In August, we recovered much of the lost ground this year to the STI. Our largest gainers were Sheng Siong, CapitaLand and Chip Eng Seng. Weakness was in Geo Energy, Banyan Tree and DBS.

We are still comfortable with our portfolio and no changes will be made. Geo Energy performance was affected by the weather slowing production and one-off cost surge in operating cost from production of a new mine. Banyan Tree’s Maldives resorts still reeling from effects of state of emergency. And Phuket will experience some near-term loss of traffic flow following the tragic accident affecting a group of Chinese tourist. DBS share price under pressure over the impact of the escalating trade tensions and recent property cooling measures slowing down loans growth.

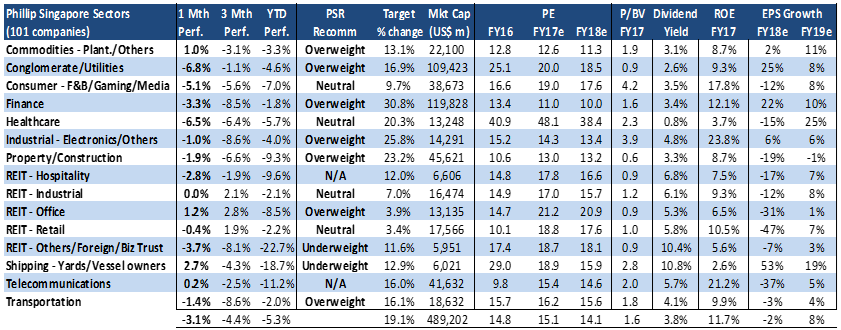

PHILLIP SINGAPORE SECTOR UNIVERSE

Best performing sectors in Aug18 were Shipping, REIT-Office and Commodities. Shipping benefited from 13.2% surge in Yangzijiang. Other marine stocks were weak. REIT-Office enjoyed modest gains in Keppel REIT (+1.7%), SUNTEC REIT (+1.6%) and CCT (+1.1%). Commodities benefited from resilient Wilmar (+2.2%) and China Aviation Oil (+4.0%).

Worst performing sectors in Aug18 were Conglomerate, Consumer and REIT-Others. Conglomerate suffered from selling in Jardine Strategic (-9.0%) and Jardine Matheson (-6.5%). Consumer suffered from large losses in Thai Beverage (-18.4%) and Genting Singapore (-16.4%), which could not offset gains in Dairy Farm (+13.5%) and Sheng Siong (+9.3%). REIT-Others fell on the back of selling in Hutchison Port Trust (-3.9%) and Parkway Life (-2.9%).

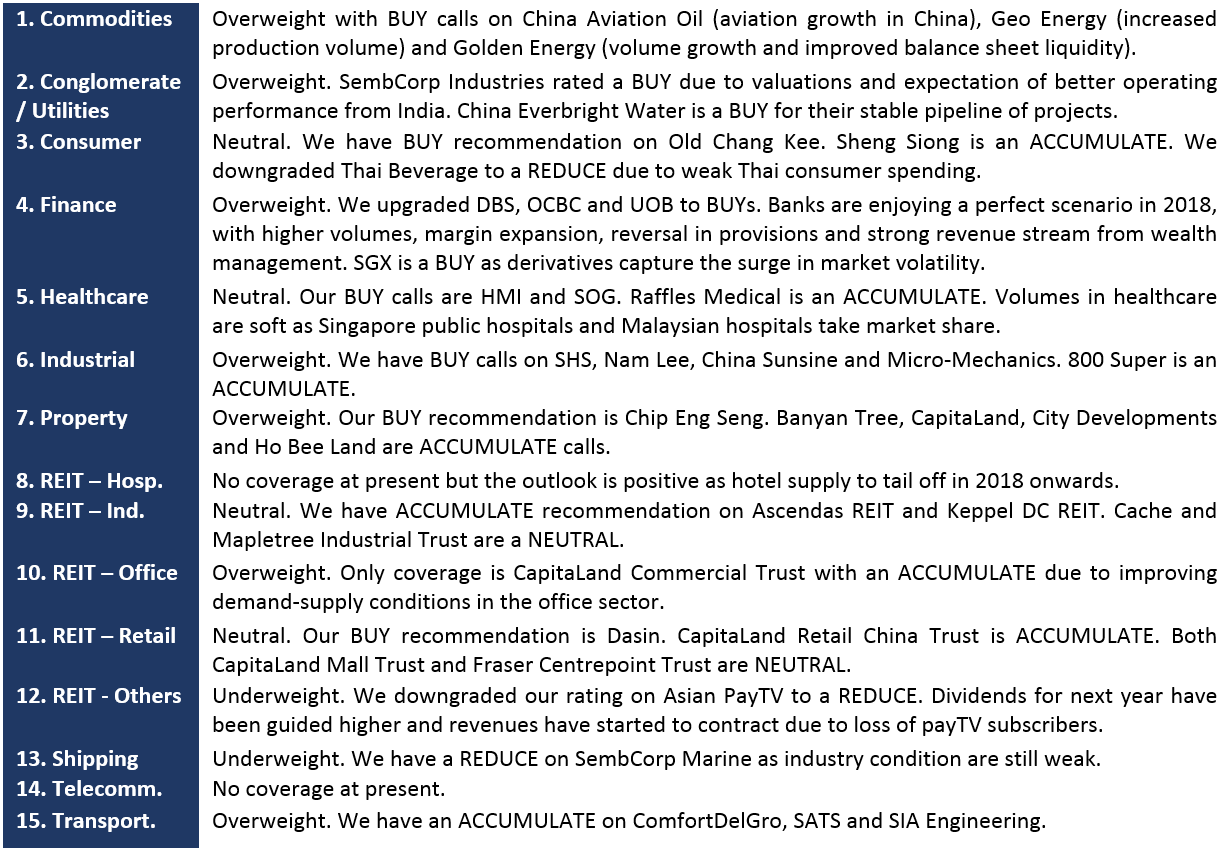

SUMMARY OF SECTOR AND COMPANY VIEWS

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.