Market:

STI weakened again in September, by 1.75%. We remain neutral on the market with STI year-end target of 3270. Attention has swung to Trump tax cuts and their ramifications. The odds of some tax cuts getting passed by the Republicans are fairly good, in our view, given the mid-term elections in November 2018. Politicians would need to deliver on some of their promises. There are various estimates on the effect of the Trump tax cuts and more importantly, deductions for capital spending – on US growth. The most optimistic estimate come from the US administration, namely a 1%-point uplift to US GDP. This sugar rush should benefit global growth. That said, we think a more significant influence will be the trajectory of interest rates. This fiscal impetus should provide cover for the Fed to raise rates in December. Even prior to the tax plan, the Fed dot plots were bandied around three rate hikes to 2.25% for 2018. The likelihood of this occurring has certainly crept up.

Turning back to macro data in Singapore, the external environment continues to be vibrant. PMIs are close to 3-year high with electronics PMI at 7-year high and exports are on pace for the fastest growth in 6-years. We believe this strength will eventually percolate down to better domestic demand. This would position Singapore banks for the triple tailwinds of rising rates (SIBOR now at 18-month high), strong loans growth (with an added boost from property sales) and vibrant capital markets (for the wealth management business). The event to note in October will be the MAS monetary policy statement. Despite the upside in economic growth, muted core inflation and a still subdued labour market, MAS is expected to maintain its neutral stance on SGD. Of less certainty is how much longer MAS will keep its neutral stance on a so-called “extended period”.

Recommendation:

In September, we initiated coverage on Micro-Mechanics. Its know-how and precision manufacturing capabilities allow it to enjoy massive 60% gross margins and 30% ROE. It is our proxy for the present surge in semiconductor sales. Another company we initiated was Dairy Farm. We believe its earnings are back to growth, supported by margin expansion from more fresh products, private labels and a streamlined supply chain.

Sector:

Echoing the recovery in Singapore exports, container throughput is similarly poised for 6-year high growth rates. We saw a large spike in the value of construction contracts awarded. This together with a reduced emphasis on pricing in awarding public projects should help sector margins. Property maintained its momentum with sales up 62% YoY in August. Sales volume is on track for its best performance in four years. Recovery in hospitality industry fizzled out as tourist arrivals eased in July. Nevertheless, RevPAR approached a 2-year high.

Technical Analysis: Straits Times Index – stuck in a range between 3274 range high and 3195 range low

Source: Bloomberg, Phillip Securities Research Pte Ltd

Red line = 20-period moving average, Blue line = 60-period moving average, Green line = 200 period moving average

September was another month bogged down with the Korea war scare as the US and North Korea exchanged heated words. North Korea stated that President Trump had declared war on North Korea and Pyongyang reserved the right to take countermeasures such as shooting down US bombers even if they are not in its airspace. The Straits Times Index (STI) remained depressed due to the escalating tensions between North Korea and the US. The STI was down -1.75% in September, and the price action suggests further downside if the 3189 critical support area gives way.

On the daily timeframe, more signs of weakness appeared after the 20-day moving average crossed below the 60 day moving average on 7 September while the 3195 critical support area held up once again proving its significance. We might see a range bound action between the 3274 range high and 3195 range low moving forward. Watch the range extremes closely as the breakout will dictate the next course of action. Keep in mind the weekly RSI is still in the midst of mean reversion off a recent overbought peak of 72 in July. Moreover, the average correction that follows after the overbought RSI mean reversion tends to drag the STI down by -7.7% suggests a bearish bias here.

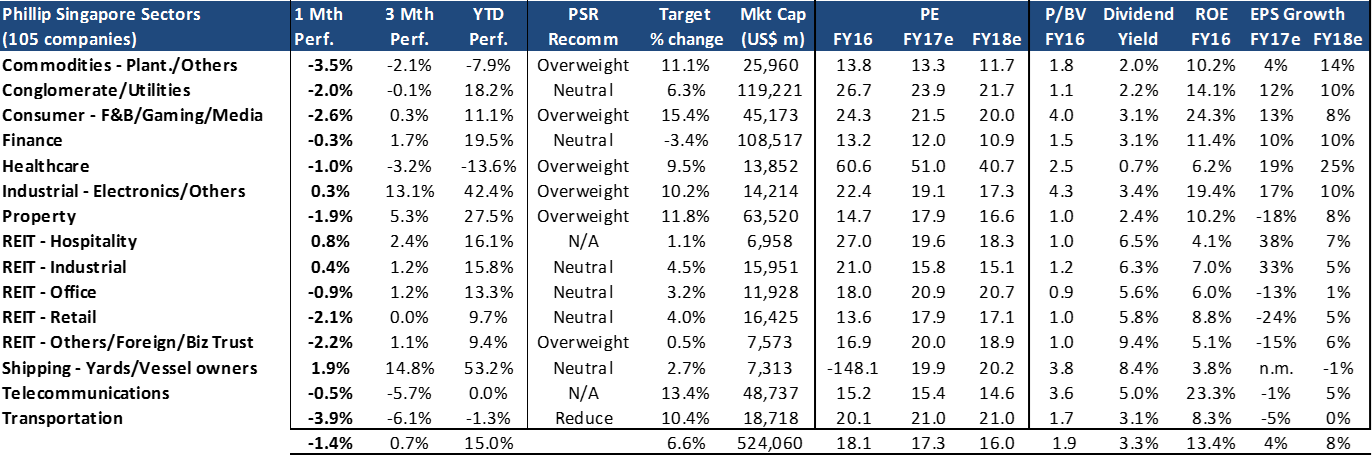

PHILLIP SINGAPORE SECTOR UNIVERSE

Best performing sectors in Sep’17 were: Shipping, REIT-Hospitality and REIT-Industrial. The gains in shipping were from both SembCorp Marine (+9.7%) and PACC Offshore (+13.3%). REIT-Hospitality modest gains was led by OUE Hospitality (+3.9%). REIT-Industrial managed to chalk up some gain, driven by Keppel DC REIT (+3.1%). The Top 3 gainers under our coverage were Cogent (+24.2%), Micro-Mechanics (+11.8%) and SembCorp Marine (+9.7%).

Worst performing sectors in Sep’17 were: Transportation, Commodities and Consumer. In Transportation, there were losses across, with biggest from ComfortDelgro (-9.2%) and SATs (-4.6%). Commodities fell due to plantation counters Golden Agri (-5.1%) and Wilmar (-4.2%). The decline from Consumer was due to Dairy Farm (-5.1%) and Thai Beverage (-3.2%). Major Top 3 decliners under our coverage include ComfortDelgro (-9.2%), CapitaLand Mall Trust (-7.8%) and CapitaLand (-5.3%).

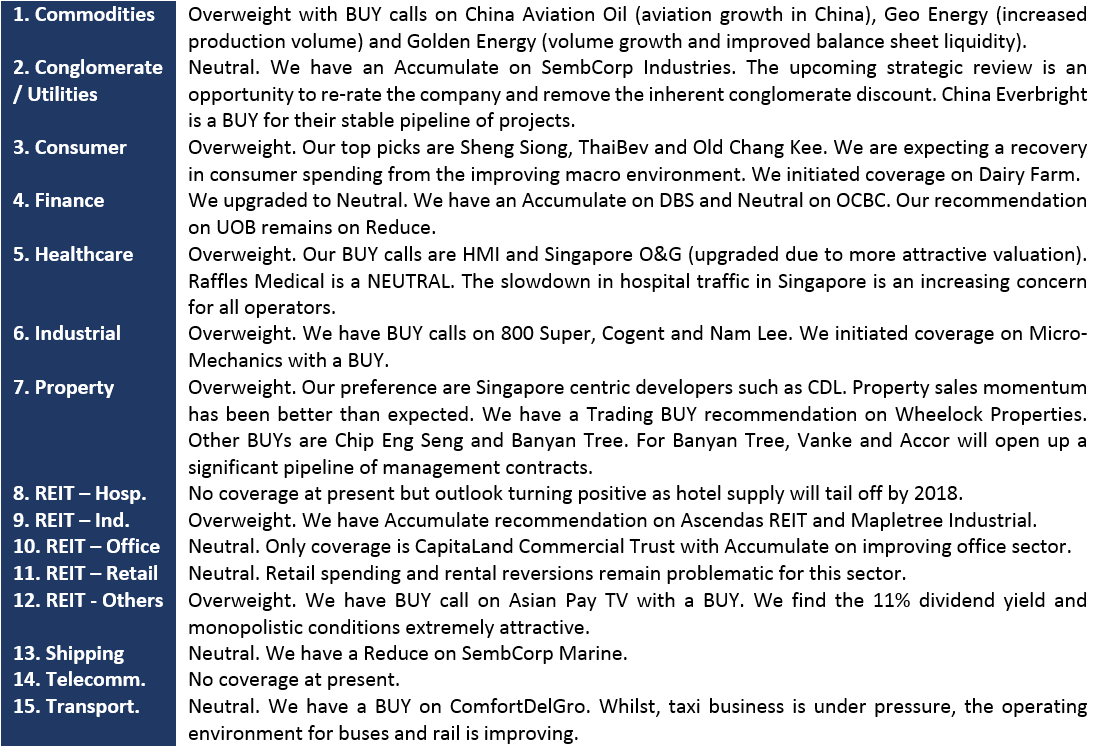

SUMMARY OF SECTOR AND COMPANY VIEWS

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.