Market: STI was down only 0.5% in March. But this masked broader weakness in the market. Of its 30 component stocks, only eight posted positive returns. Half were banks and electronics. The market had a whiff of President Trump’s stance on international trade when he withdrew the US from the TPP shortly after his nomination. Since then, he has played down his trade rhetoric. It is now back on. He has declared trade wars as good and that they can be won. He has also exercised the US’ so-called nuclear option in trade by invoking national security as the reason for import tariffs. This is supposed to be used in times of emergency or war. While steel and aluminium only comprise 2% of the US’ imports and nothing concrete has been rolled out, his rhetoric has fanned new uncertainties. The fear is retaliation and an escalation of trade protectionism. Of concern will be the current US investigation into China’s violation of intellectual-property rights. It may result in the US restricting Chinese investments in US companies, tariff penalties on imports, and visa controls. What could hold back the President would be his own Republican Party members who have no interest in dialling back the current economic momentum as they head out to the 2018 mid-term elections.

A Peterson Institute for International Economics policy brief laid out the advantages of cross-border trade. Trade allows industries to exploit economies of scale and generate technological spillovers (spread of innovation), import competitiveness (curtailment of monopolies) and comparative advantages (through specialisation). Studies suggest a $0.24 gain for GDP for every $1 rise in two-way trade. Admittedly, there are adjustment costs from jobs lost. However, the ratio of economic gains from trade to the cost of displaced workers is 5 to 1. Any gains for the domestic steel sector in the US will be at the expense of steel-consumption sectors such as auto, construction and machinery.

In Singapore, the headline news was the FY18 budget and completion of the reporting season. Most impactful was an incremental rise in buyers’ stamp duties for property and an extension of tax transparency to REIT ETFs. Increases in GST have been deferred. Banks surprised the market with a large jump in ordinary dividends. The three raised their aggregate ordinary dividends by 25% or S$1bn, 90% alone from DBS. Electronic companies beat expectations with sales and earnings growth of 30% and 100% respectively in 2017.

Recommendation: We remain Overweight on banks, property, electronics and the consumer sector. DBS’ strong performance has tilted our preference to OCBC. The latter’s insurance business is another beneficiary of rising interest rates. Its Hong Kong loan growth remains above trend. The property sector succumbed to some weakness after the recent rise in stamp duties. Still, we are positive, as en-bloc liquidity has yet to surface. Electronics continues to enjoy a positive outlook, though USD weakness may take a bite off their earnings. The consumer sector still reels from sluggish consumption in the region. A stock we upgraded was SGX. It will be a beneficiary of the recent spike in volume and volatility. In addition, it pays a 4% dividend yield. Our STI target of 3900 has been maintained.

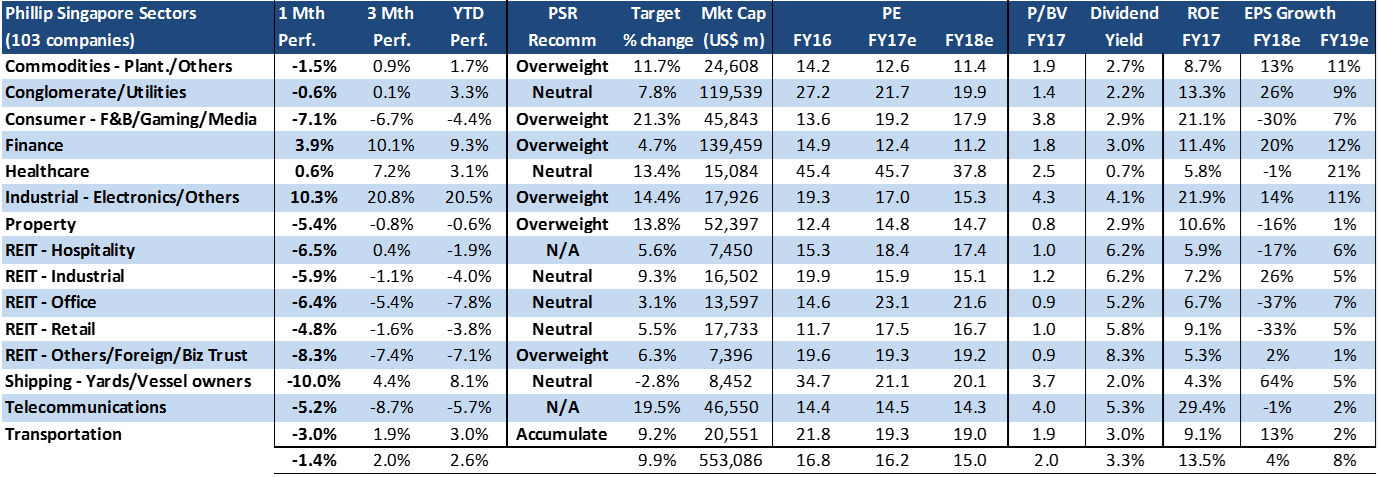

PHILLIP SINGAPORE SECTOR UNIVERSE

Best performing sectors in Feb18 were Industrial, Banks and Healthcare. The gains in industrials came from electronics names such as Hi-P (+29.3%), AEM (+28%) and Venture (19.5%). Positive returns on financials was predominantly due to DBS (+8.7%). The other two banks were up less than 2%. SGX dropped 7.9%. Healthcare was virtually flat due to rise in Raffles Medical (+3.6%).

Worst performing sectors in Feb18 were Shipping, REIT- Others and Consumer. Shipping faced weakness from SembCorp Marine (-15.2%) and PACC Offshore (-14.8%). REIT-Others tumbled on the back of selling in Hutchinson Port (-12%), and Accordia (7.2%). Leading the losses in consumer were Genting Singapore (-14.1%) and Thai Beverage (-9.2%).

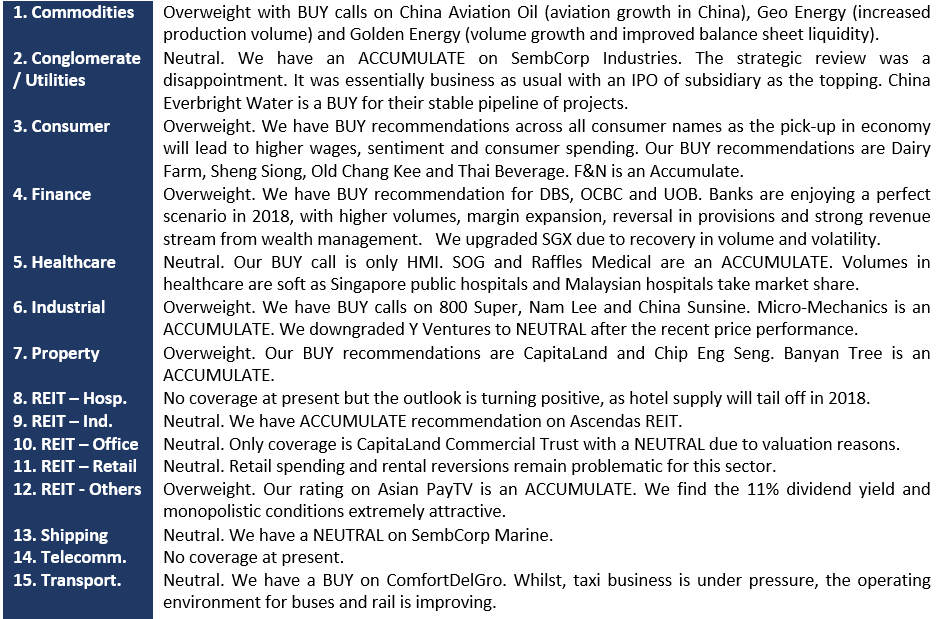

SUMMARY OF SECTOR AND COMPANY VIEWS

SECTOR COMMENTARY

PROPERTY

Real Estate Developers’ Association of Singapore: BSD tweak unlikely to derail housing recovery

As part of Budget 2018, the government has raised the Buyer Stamp Duty (BSD) rate on the portion of residential property value in excess of S$1 million. The existing 1 to 3 per cent BSD rates still apply to the portion of residential property valued at S$1 million and below.

Comment: Bigger ticket purchases and en bloc purchases will be impacted more as the incremental 1% tax is only on the portion of home values above S$1mn. Over the last 2 years, the average transaction value was slightly below S$1.5mn, with average size condominium units sold at c.100sqm. For the average transaction, impact will be smaller – 0.3% or S$5,000 extra for a $1.5mn house. As the quantum goes higher, the closer the impact to the full 1% of purchase price. We do not expect a material negative impact on demand given the relatively small full impact vs purchase price for the average transaction. En bloc sales momentum, which has slowed lately with lower premiums paid vs reserve prices, could see further slowdown as the additional BSD eat into redevelopment margins.

TRANSPORT

SBS Transit lands Bukit Merah bus contract with S$472 million bid

SBS Transit, Singapore’s largest bus operator, has clinched an S$472 million deal to run 18 services in the Bukit Merah area, with three being cross-border routes into Johor Baru. It beat five other bidders in a competitive tender called by the Land Transport Authority last April. They were Singapore rail operator SMRT, the UK’s Go-Ahead and Australia’s Tower Transit – which operate existing bus routes here – as well as Chinese operator Shenzhen Bus Group and a consortium between Jiaoyun Group and Travel GSH.

Comment: SBS Transit is the incumbent for the Bukit Merah package, which started as one of the 11 negotiated packages since September 2016. The first three packages tendered through competitive bidding were the Bulim, Loyang and Seletar packages. The Bukit Merah package is now the fourth to be tendered through competitive bidding. With the award of the contract, there is continuity in the revenue stream for SBS Transit.

The next SBS Transit negotiated package to be up for tender is the Sengkang – Hougang package in 2021. The Bulim (Tower Transit Singapore) and Loyang (Go-ahead Singapore) packages will also be up for tender in 2021 if they are not extended. The next SMRT Buses package that will be up for tender is the Sembawang – Yishun package in 2020.

Phillip On The Ground – excerpts from our various conversations

Telecommunications

Utilities

Consumer products

Coal

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.