Market: STI was down 5.1% in May, returning all its gains of the previous month. YTD, it is virtually unchanged. There was selling across the sectors, spooked by one crisis or another. Hogging the headlines has been a spike in Italian bond yields and US trade tariffs. Italy’s troubles are more political than economic, unlike the euro-sovereign crisis in 2012. The base case is that the Italian electorate did not vote for an Italexit but rather, more fiscal largess and tighter immigration. An exit from the Eurozone could be devastating for the Italians, since they own 2/3 of Italian sovereign bonds. Such debt would have been devalued, as it is re-denomination in the old Italian lira and will be priced at much higher interest rates. Even before such an event, there would have been a paralysing run on the country’s banks and government debt. But while unemployment in Italy is bleak – no better than when it joined the Eurozone 19 years ago, it is unclear if the country is willing to take so much upfront pain for perhaps an even more uncertain future. Nevertheless, this remains a long fuse. The EU needs fiscal union among its members. The economic cycle among its members are not even and a common currency exacerbates imbalance. The euro crisis has shown, there is little fiscal legroom given by the market to individual countries when sovereign debt shocks occur.

A shorter fuse will be President Trump’s trade skirmishes with everyone, including so-called allies. Our two-legged tail risk recently initiated another national-security investigation. The target now is US auto and auto-parts imports. Public hearings have been scheduled for July. To sum up, Trump has so far imposed tariffs on around US$55bn of imported solar panels, steel and aluminium. The economic impact may be minimal but another US$350bn is under consideration, stemming from s.301 unfair trade practices (US$46bn of China imports) and s.232 national security concerns (US$100bn of Chinese products plus US$208bn of auto and auto parts). All the above could be even eclipsed by a possible collapse of Nafta. Trade is the dominating dark cloud over the market where there is little clarity on the outcome.

Away from politics, 1Q18 GDP from developed countries was not pretty. There was a deceleration in the US, Europe and Japan. Asia bucked the trend. On a YoY basis, the pace of GDP growth for Singapore and Hong Kong picked up pace from the prior quarter. Recent data suggest global-growth improvement in 2Q18. In Singapore, most indicators support a healthy economic momentum, such as the manufacturing PMI, tourism, transportation, construction and loans growth. Less encouraging is still stubbornly modest wage growth. Another weakness is private-sector hospital admissions, where there is a clear loss of patient flow to public hospitals.

Recommendation: Our bottom-up STI target of 3,900 remains premised on a growing economy, which will pull up banks’ earnings and with a lag, the other domestic sectors. The latest data suggest improving loan growth and margins for the banks. That said, general sentiment continues to be whipsawed by the constant troubles in Europe, emerging markets and trade. Separately, we initiated coverage of SHS Holdings. We expect strong earnings growth from a surge in demand from New Zealand for its steel-precast products. An added earnings driver will be the commencement of its solar project.

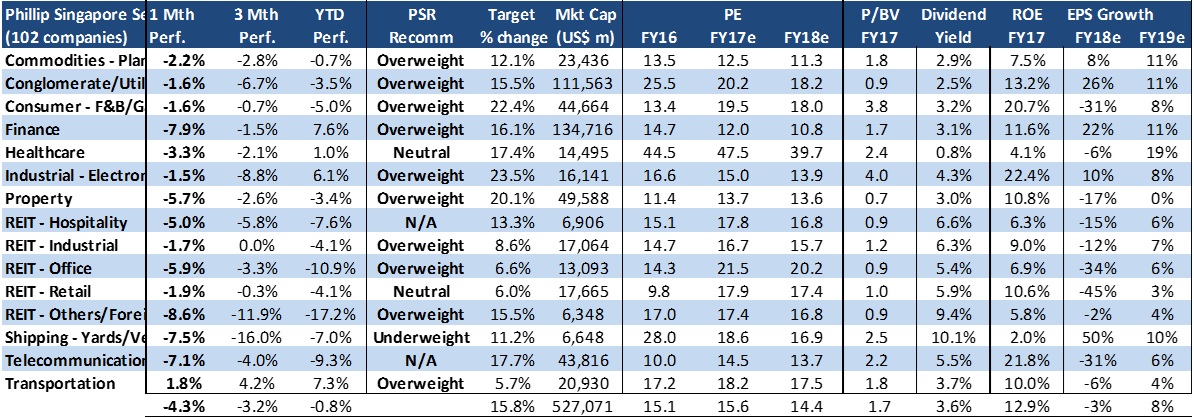

PHILLIP SINGAPORE SECTOR UNIVERSE

|

Best performing sectors in May18 were Transportation, Industrial and Consumer. Transportation enjoyed gains from ComfortDelgro (+9.3%) and SIA (+3.7%). Industrials fell but still outperformed other sectors. There were positive gains in China Sunsine (+2.7%), Valuetronics (+2.5%) and Venture (+0.7%). Consumer outperformance came from Genting Singapore (+7.7%) and Dairy Farm (+1.8%). Worst performing sectors in May18 were REIT – Others, Finance and Shipping. REIT – Others suffered from declines in Hutchinson Port (-17.9%) and Asian PayTV (-12.2%). Finance saw across the board selling in all three banks, OCBC (-9.1%), DBS (-8.0%) and UOB (-6.6%). Shipping declined due to the drop in Yangzijiang (-17.5%). |

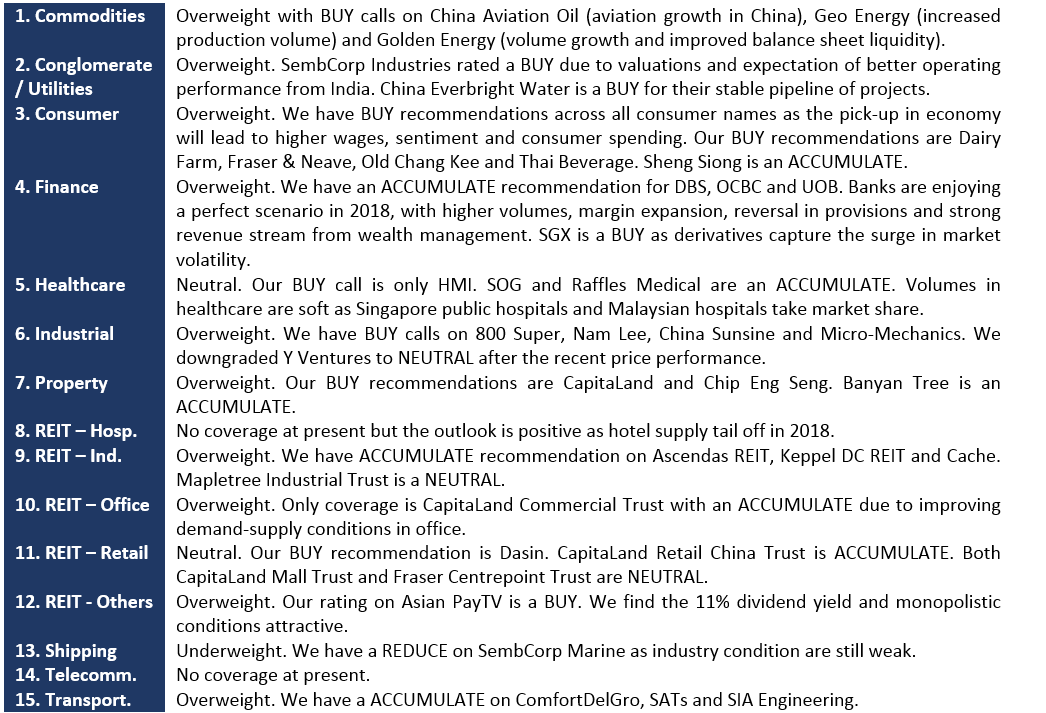

SUMMARY OF SECTOR AND COMPANY VIEWS

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.