Market: STI was down 4.65% in June. It has shed almost 10% over two months. Escalating trade tensions was the culprit. It was supposed to be mere posturing, but President Trump has taken the trade-war tail risk a notch closer to the base case. He will likely be emboldened by a strong US job market, fiscal stimulus support and firm approval ratings. Hard to fathom the economic impact of this because there is little precedent. We looked at some IMF studies on the impact of tariffs. A 10%-point rise in import tariffs by both the U.S. and the rest of the world could lop 1% off world trade and 0.5% off world GDP. The slower growth will stem from less trade, fewer goods produced and decreased business spending. The damage on individual countries will depend on how quickly their currencies adjust to the new terms of trade.

The trouble with turning completely bearish on equity markets is that Trump could reverse his tariff stance virtually overnight. For now, the odds are that the tariff net will be cast wider. The next two dominoes will be US$400bn of Chinese imports plus US$200bn of auto and auto-parts imports. Another impetus to raise the rhetoric on China is the recent weakening of the renminbi against the US dollar. It is fuel for China sceptics, Ross and Navarro. There is also the unresolved issue of NAFTA. Political agendas now dictate the outlook of markets rather than economic rationality or any obvious data points. And they are highly unpredictable. We expect investors to demand higher risk premiums.

Our strategy was to go more local and seek relative shelter from the tariff impact on global growth. However, another tail risk has emerged in the past few days. The authorities have slapped additional stamp duties on property transactions and demanded higher LTV for mortgages. Like everyone else, we were surprised. With HDB prices moving sideways and the property upcycle only four quarters old – the previous two lasted 17 quarters, we did not see the urgency. Obviously, we are not as clairvoyant.

As we review 1H18, we had our share of hits and misses. Global growth was resilient, as envisaged. Improvements in capital spending spurred aggregate demand. Interest rates did rise but there was no runaway inflation to trigger pre-emptive rate hikes. The biggest miss for us was Trump’s willingness to enter into a trade war. Sector-wise, banks, consumer staples and land transportation were the performers. Our misses were property, coal and dividend-paying stocks. The two initiations that performed well for us were Y-Ventures and China Sunsine Chemical.

Recommendation: We are lowering our STI target to 3700. While our bottom-up computation is still at 3900, we are now benchmarking against the lower end of the respective STI stock target prices. This discount is to incorporate the upcoming macro headwinds as trade tensions rise. Banks are our favoured sector, together with consumer staples. Fundamentals for coal remain positive, power consumption in China is rising at its fastest pace in 7-years. As electronics loses its leadership, we look for some rotation to the oil and gas sector. We have yet to find suitable proxies. Commercial and industrial property should see some recovery in investment flows as the residential route has been blocked.

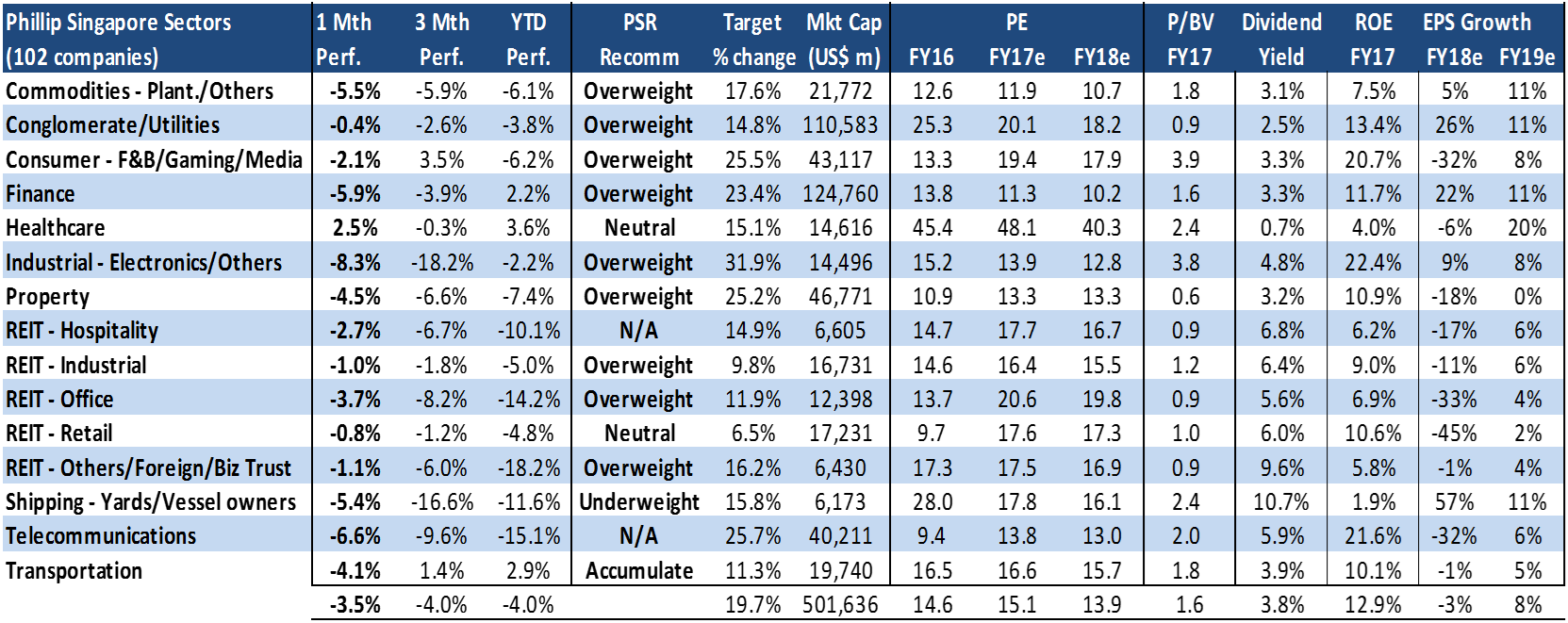

PHILLIP SINGAPORE SECTOR UNIVERSE

Best performing sectors in Jun18 were Healthcare, Conglomerate and REIT-Retail. Healthcare was helped by a 3.5% gain in IHH. The other stocks in the sector fell Raffles Medical (-3.8%) and HMI (-4.8%). Conglomerates experience selling across all stocks except Jardine Matheson (+1.1%) and Jardine Strategic (+1.9%). REIT-Retail benefited from a flat performance in CapitaLand Mall Trust (0%) and Mapletree Commercial (0%).

Worst performing sectors in Jun18 were Industrial, Telecommunications and Finance. The three largest names in industrial were sold down ST Engineering (-5.5%), Venture (-15.5%) and Hi-P (-15.0%). All three telcos faced declines with Starhub (-14%) enduring most of the weakness. SingTel (-6.1%) and M1 (-10.1%) also plunged. The 3 banks were down this month – OCBC (-7.2%), DBS (-6.2%) and UOB (-4.9%).

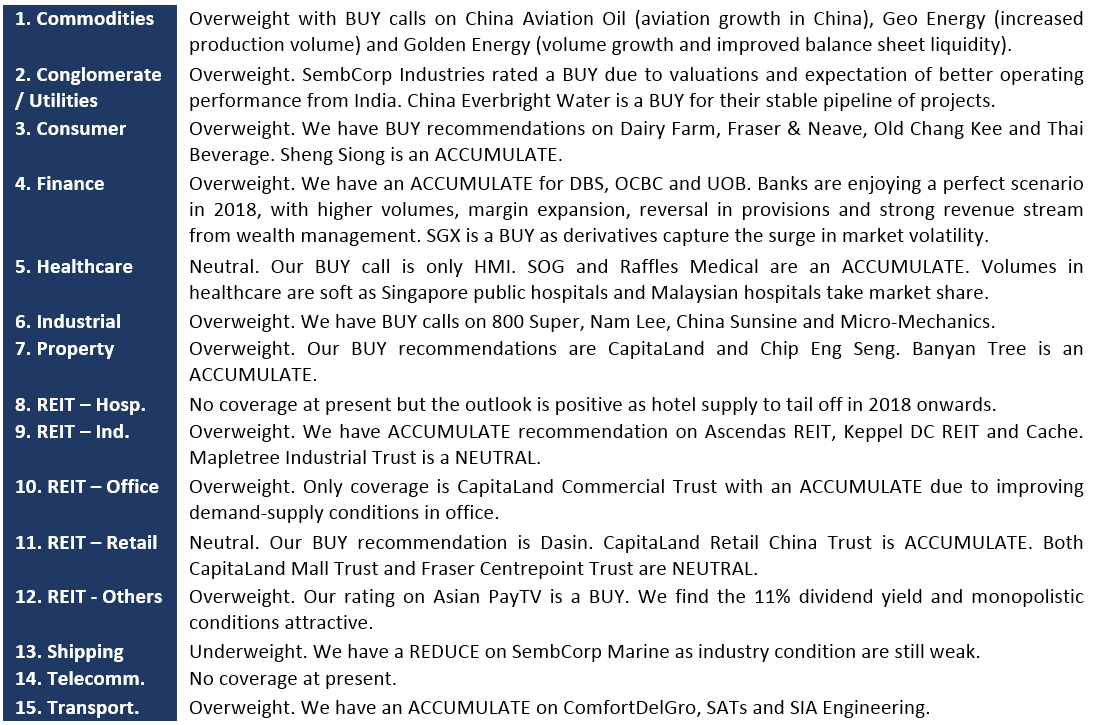

SUMMARY OF SECTOR AND COMPANY VIEWS

SECTOR COMMENTARY

1. Oil and Gas

SembMarine (SMM) bags 1st polar expedition cruise ship design contract

SMM has secured its first polar expedition cruise ship design contract. The contract signed between SMM’s subsidiary, LMG Marin and Croatia’s Brodosplit Shipyard, is for the design of a ship to be built for Quark Expeditions. It calls on LMG Marin to deliver a basic design package for the 128-metre ship, which can carry up to 200 passengers and 116 crew members. The ship is scheduled for completion by the third quarter of 2020. It would join Quark’s pool of purpose-built vessels for expeditions to the Arctic and Antarctic.

Comment: The cruise ship design contract marks a milestone for SMM in terms of breaking into a new market. However, the core business, offshore and marine engineering is still challenging. We are expecting only a gradual recovery from offshore drilling and production activities. We believe that SMM will have a turnaround when upstream capex resumes substantially. Therefore, it will take some time for SMM to pick up its performance. More critical will be penetrating the FLNG market.

2. Property

CapitaLand bags 2 mall management deals in China

CapitaLand Retail, will manage the retail component of The Grand City, a landmark integrated development in Wanbo CBD in Panyu District, on behalf of Guangzhou Wan Shun Investment Management Co Ltd. On winning this contract, CapitaLand is adding a third mall in Guangzhou. Its retail network in South China now spans a total retail gross floor area (GFA) of 3.6 million square feet.

Comment: Since announcing the intention to grow its retail footprint through the asset-light management contracts strategy, CapitaLand has signed 10 agreements with a total GFA of about 5.3mn sq. ft in less than two years. While this is still a small fraction of the total 91 malls CAPL currently runs and insignificant contributor to earnings, we are positive on this strategy, as it allows CAPL to scale up in a less capital intensive manner while leveraging on its strength as a reputable mall operator.

CapitaLand acquires prime mixed-use site in Chongqing worth 5.7b yuan

Capitaland has acquired all the shares in a company that owns a 32-hectare prime mixed-use site in Chongqing, in a move that will boost its residential pipeline in China by more than 2,100 units. The amount payable is 2.2 billion Chinese yuan (S$454.3 million), which includes the agreed value of the property at 5.7 billion yuan

Comment: This translates to a land price of RMB17,800 per square metre of land. The land parcel also includes two greenfield sites and a brownfield site which would yield office and retail space on top of the 2,100 residential units. We note average selling prices for residential prices in Chongqing have picked up pace since 1Q17, with an average YoY growth of 24%. We maintain our Accumulate call on CAPL with unchanged TP of S$4.19. Residential sales of RMB10.6bn in China expected to be handed over in the next 9 months will further provide support to earnings in FY18 on top of the recurring portfolio income.

Ho Bee Land acquires freehold Grade A London property with £650m investment

Frasia Properties Sàrl owns the property known as Ropemaker Place, a 21-storey Grade A office building comprising approximately 602,000 square feet of commercial space. Ropemaker Place occupies a substantial freehold island site of about 1.37 acres (about half a hectare) in the City of London.

Comment: With this S$1.2bn investment, Ho Bee’s has doubled its investment properties portfolio size in UK to S$2.4bn. This is close to half the Group’s total investment portfolio size. At a net yield of close to 5%, and a long WALE of close to ten years, this investment will provide recurring income that will further support. Forex losses have been mitigated with a natural hedge by funding the acquisition though pound-denominated loans. We estimate with this rental property, total recurring income for FY18e would be sufficient to support close to 4x estimated dividend of SG 8cents for the same year.

REIT

ARA Asset Management (ARA) to acquire all the shares that it does not already own in the Reit manager and property manager of Cache Logistics Trust (Cache)

This will end the sponsor-Reit relationship between global logistics player CWT and Cache. – CWT currently owns 40% of the issued shares of the Reit manager, ARA-CWT Trust Management (Cache) Limited, and 60% of the issued shares in the property manager, Cache Property Management Pte Ltd.

Comment: There is no longer a Right of First Refusal (ROFR) over CWT’s assets. However, to put things in context, Cache’s track record has been 23 acquisitions since IPO, out of which only two were ROFR assets from CWT. Cache has not been heavily reliant on the ROFR assets for inorganic growth.

It is worth noting that Warburg Pincus has a stake in both ARA and e-Shang Redwood (ESR). In view of the ongoing merger between ESR-REIT and Viva Industrial Trust, it appears that Cache could soon be part of the consolidation theme alongside Sabana Shari’ah Compliant REIT (9.05% stake held by ESR).

Technology

Y Ventures signs exclusive online distribution for Disney merchandise in South-east Asia

Y Ventures Group said that it has entered into an agreement with Beast Kingdom Co Ltd, a licensee for official Disney products in Asia, to act as its exclusive online distributor in South-east Asia for three years. Y Ventures said that it aims to be the largest online retailer of official Disney products in the region with this deal – which will see the company’s online stores stocked with official Disney, Marvel, Star Wars and Pixar merchandise.

Comment: Y Ventures entered into a three-year distribution agreement with Beast Kingdom Co. Ltd for the exclusive distributorship in Southeast Asia. Beast Kingdom is a major Disney licensee with products ranging from Disney, Marvel, Star Wars and Pixar; this will allow Y Ventures to extend its product range beyond academic textbooks and private label brands and is a huge step in expanding its distribution portfolio. Y Ventures will now have access to a variety of popular figurines, toys, novelties and stationery alongside with Beast Kingdom’s trending figure series Egg Attack Action to add to its arsenal of products. Y Ventures will provide its expertise in data analytics to augment product selection, optimise online marketing, ensure an end-to-end delivery and handle after-sales support to customers. This partnership signified Y Ventures data analytics capabilities and strengthened its foothold to be a leading e-commerce company in the region.

Source: Business Times, Straits Times

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.