Market: STI was down 2.6% in March and up 0.7% in 1Q18. Last month, we faced a deluge of bad news. The US administration slapped tariffs on $50bn worth of Chinese imports, mainly in machinery and equipment. China threatened to respond in the same proportion, scale and intensity. Trump triggered further nervousness by attacking Amazon, threatening to exit NAFTA, appointing a new security adviser whose views included a pre-emptive strike on North Korea and welcoming the visit of Taiwanese officials, to the ire of the Chinese. I guess that two-legged tail risk is unravelling. Only a de-escalation of reciprocal tariffs will calm the market, in our view. An upcoming 15 May public hearing on tariffs imposed on China could see the peak of punitive tariffs. With looming mid-term elections, it is unlikely that the Republicans will want China’s targeted tariffs on agriculture and food products to hurt their red states, in our opinion. If we assume $100bn of two-way trade and a 0.24ppt impact on GDP – using the Peterson Institute’s policy-brief assumptions – the effect is less than 0.2% on the combined US and Chinese economy of $31tr. The market knows the impact will be modest. The bigger damage is uncertainty over how far this war will go. A positive from all the noise has been a decline in US Treasury yields and inflation expectations.

On the economy, there has been only a milder patch of data. US PMI has gone softer, but this is from multi-year highs. Retail sales have moderated, though still growing at 2017 rates. Vibrant employment together with a pick-up in wages should provide upside to consumer spending in the US. We see corporate expenditure gaining momentum. Our Singapore indicators are mixed. Exports have trended down, but industrial production and PMI hold their ground.

Separately, it was no surprise that the Fed raised interest rates by 25bps. The dot plots did show more members – four to seven – expecting four rate hikes in 2018. Curiously, the inflation forecast was only raised marginally to 2.1%, a tad above the Fed’s 2% target for 2019. We think higher rate expectations have been baked in by the market. Singapore’s REIT index was down 4% in 1Q18. The probability of three rate hikes in 2018 has climbed to 41%, according to Bloomberg.

Recommendation: We have not changed our bottom-up 3,900 STI target, for 13.8% upside potential. We think banks will provide support with their earnings. While loan growth in Singapore is 4.6%, below our 7% expectation, we expect significantly better NIMs from YoY rises in both the SIBOR (+38%) and SOR (+55%) this quarter. Another leg to growth could be provided by Hong Kong, where loans are expanding 16% and the HIBOR, up 54% YoY. Property sales in Singapore are resilient. Take-up in a recent residential launch by CDL was strong, at almost 40% over a weekend. And the product was priced more than 20% above transactions in the adjacent area. Another sector we like is coal. Coal prices have been resilient as China plans to cut supply while its power consumption is rising. Chinese imports of coal from Indonesia are up 55% YTD. Our Buys in the sector are Golden Energy and Gear. The production from both companies is expected to be up 33% in 2018.

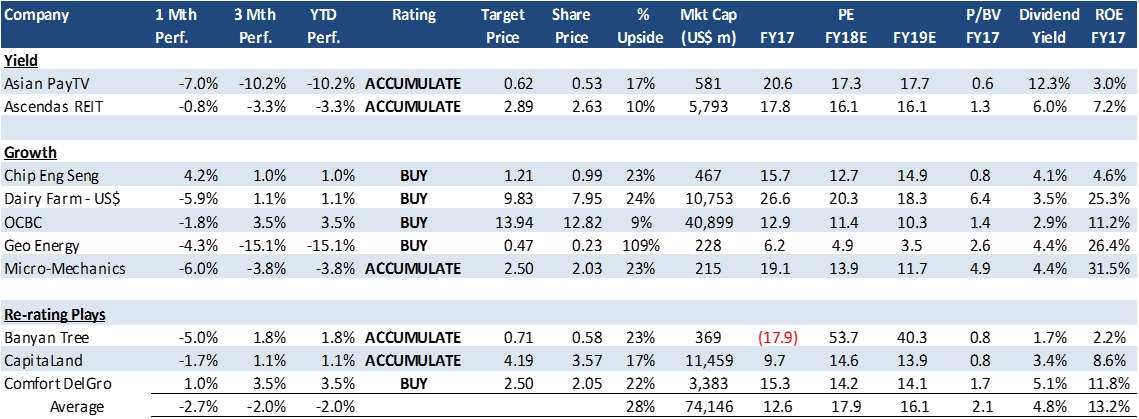

PHILLIP ABSOLUTE 10 – Our top 10 picks for absolute returns

Source: Bloomberg, PSR

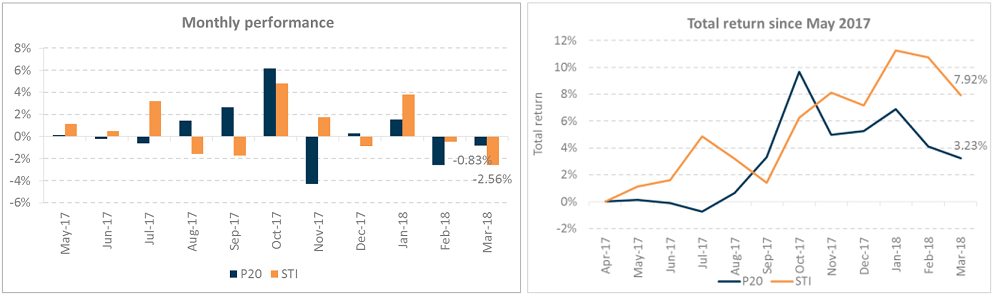

Phillip Absolute 10 performance assumes equal weightage to every stock in the portfolio. Any change to Phillip portfolio is only conducted at month end. Performance of the portfolio and STI does not take into account gains from dividends.

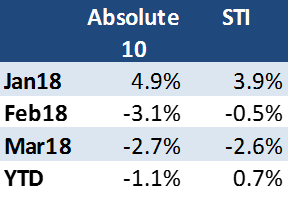

HISTORICAL PERFORMANCE

Portfolio Review:

Our inaugural Phillip Absolute 10 Model portfolio began in January. It started well with a rise of 4.9% in January. Banyan Tree and CapitaLand led gains in January. DBS has been a significant contributor to our performance with a gain of 15% for the period of Jan-Feb18. We then switched to OCBC in March due to higher upside to our target price and a beneficiary of higher interest rates (in particular through insurance business). We have now seen two consecutive months of decline. Dragging our YTD performance has been Asia Pay TV and Geo Energy.

APTV: No change in our recommendation. Operationally we are expecting a stable outlook. Broadband is a potential source of upside. It is the highest margin product which has started to gain some subscriber momentum. On macro factors, Taiwan dollar has actually appreciated against Singapore dollar. There is also no pressure on interest rates, as TAIBOR is trading sideways.

Geo Energy: No change in our recommendation. 4Q17 performance was disappointing due to weaker production growth due to poor weather conditions and higher interest expense as they build up cash reserves for an acquisition. We are still positive on the company. Coal prices are resilient and we expect production to rise by 40% to 10.8m MT in FY18e. Stock is trading at around 5x PE and in net cash position with a dividend yield of 4%.

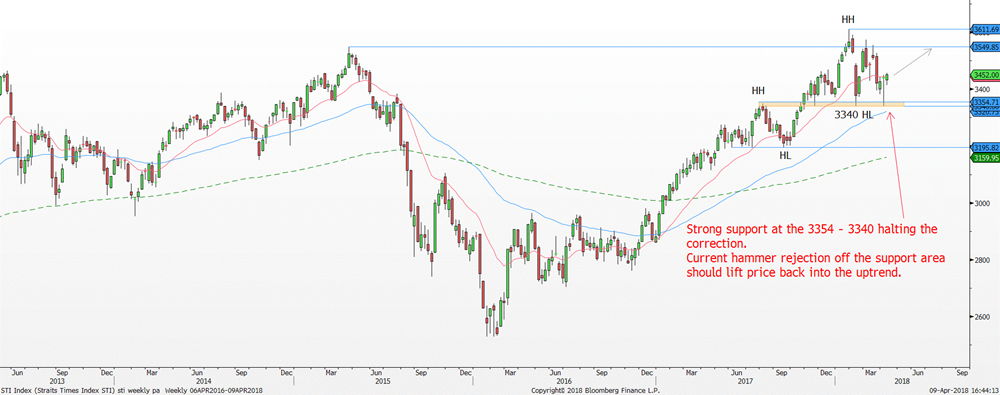

Technical Analysis: Straits Times Index – hammer rejection off the 3,354 – 3,340 support area suggests a rebound higher

STI Weekly Chart Current Sentiment: Bullish

Source: Bloomberg, Phillip Securities Research Pte Ltd

Red line = 20-period moving average, Blue line = 60-period moving average, Green line = 200-period moving average

March was another disappointing month as the Straits Times Index (STI) failed to follow through with bullish momentum from the last two weeks of February. As a result, the STI was down -2.50% in March mainly caused by the general risk-off sentiment across the world.

From a longer-term price action perspective, the general risk-off sentiment has dragged the STI into a prolonged correction that began in January, but the long-term uptrend remains intact. Even with the severe correction of –7.5% off the 3,611 high in February, the STI managed to keep the structure of the uptrend in place as it continues to form a series of Higher Highs (HH) and Higher Lows (HL). More importantly, the 3,354 to 3,340 support area needs to hold for the uptrend to regain strength.

On the weekly timeframe, the 3,354 to 3,340 support area held up once again for the week ended 06/04/18 proving the significance of the support area. Moreover, the strong bullish rejection resulted in price forming a hammer suggests a possible reversal higher back into the uptrend. Further clues of bullishness can be seen when the STI closes back above the 20-week moving average.

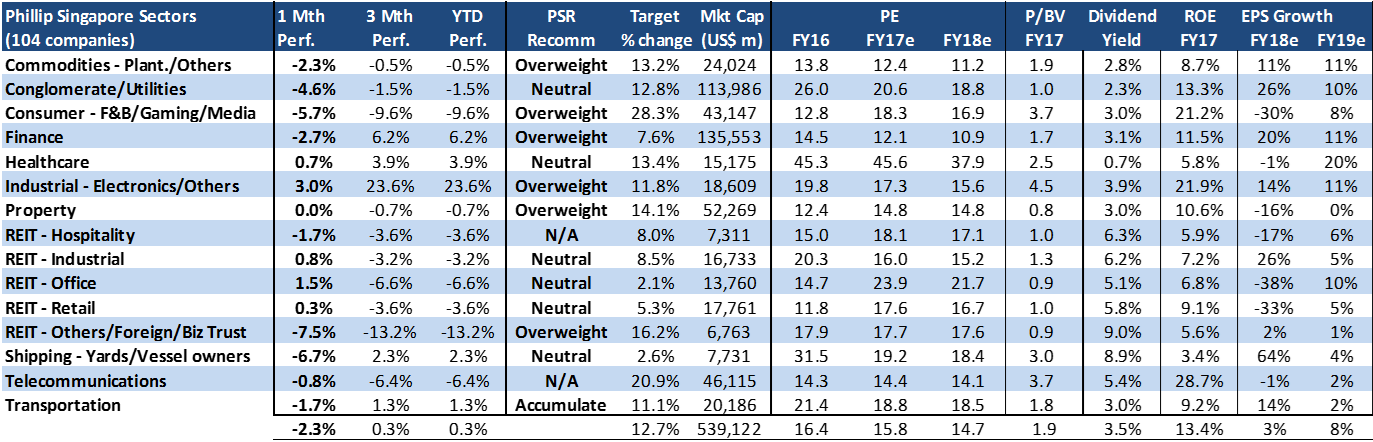

PHILLIP SINGAPORE SECTOR UNIVERSE

Best performing sectors in Mar18 were Industrial, Healthcare and REIT-Retail. The gains in industrials came from electronics names such as Memtech (+23.0%), Valuetronics (+11.9%) and China Sunsine (7.8%). Gains in Healthcare was only in IHH (+1%) REIT-Retail outperformed due to gains in CapitaLand Mall Trust (+3.0%).

Worst performing sectors in Mar18 were REIT- Others, Shipping and Consumer. Sell-down in REIT-Other was due to 19.2% fall in Hutchinson Port Trust. Shipping weakness was led by Yangzijiang (-19.9%). Consumer declined on the back of declines from F&N (-9.3%), Genting Singapore (-6.9%) and Thai Beverage (-6.6%).

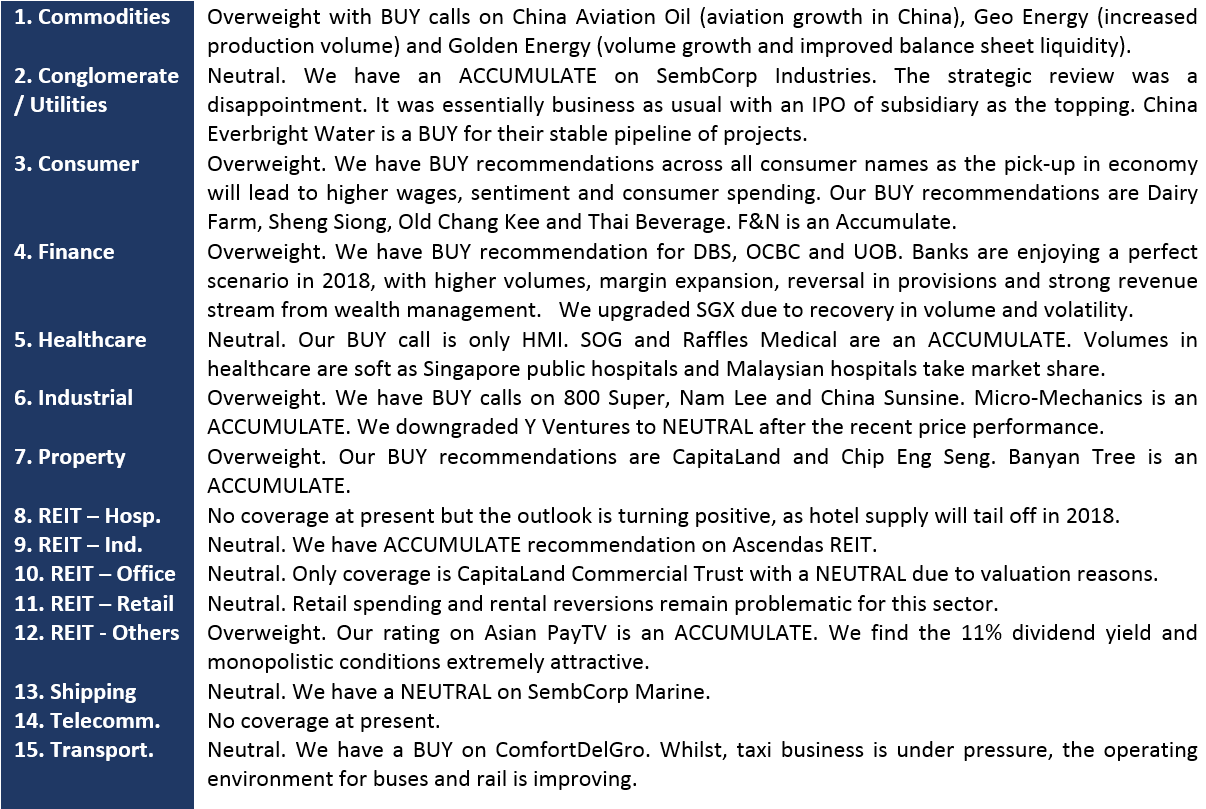

SUMMARY OF SECTOR AND COMPANY VIEWS

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.