What happened

U.S federal government shut down for the 19th time since 1976. This was hardly a novelty for the markets as reaction on Monday’s trading activity were muted if anything. The shutdown was due to the “spending gap” as the government funding was deemed insufficient for the full operation of the Federal Government. This results in hundreds of thousands of federal employee being on furlough on Monday.

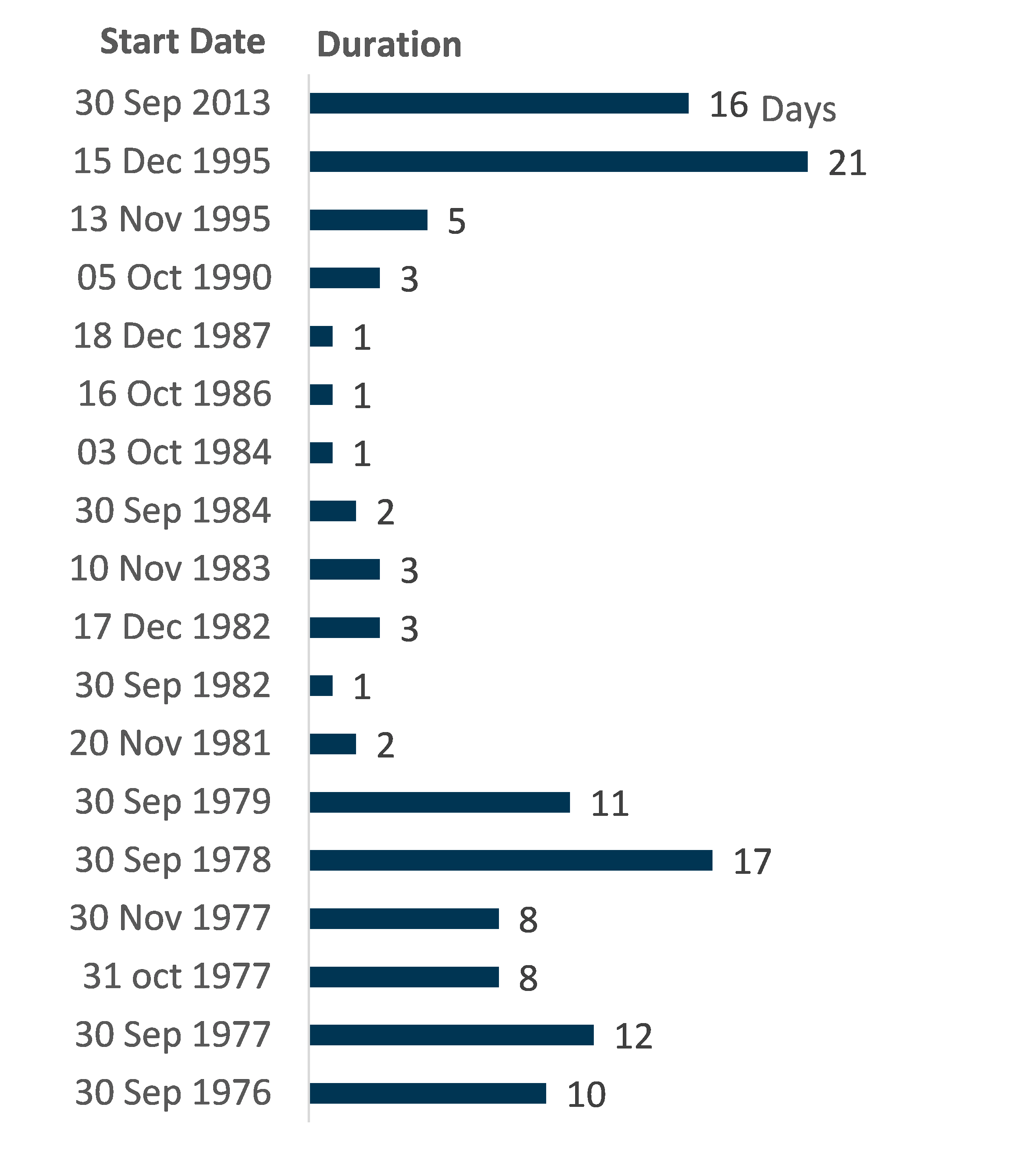

The last government shutdown occurred in September 2013 under President Obama, resulting in a 16 days shutdown. These shutdown are generally due to the dispute over the use of funds between the Democratic and Republican party.

Fig 1: Length of Government shutdown since 1976

Source: US Federal Government, PSR

How did the market react

The recent shutdown was too short for us to have any meaningful analysis of the full market reaction as 2 out of the 3 days of shutdown were on the weekend. Technically, the shutdown only affected the federal government operation on Monday before President Trump’s sign the temporary bill to extend the spending till 8 Feb 2018 that same evening. However, we can take cue on the previous shutdown periods to grasp a better understanding of the market reaction if the government was to shut down again on the 8 February 2018.

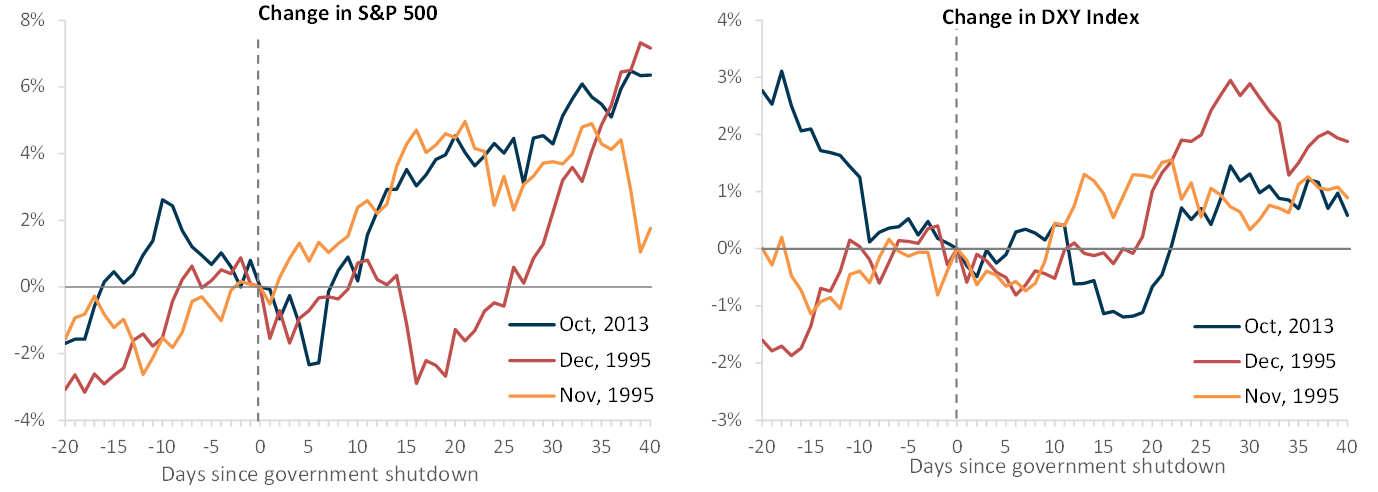

Fig 2: Previous Shutdown have modest effect on Financial Markets

Source: Bloomberg, PSR

Equity markets: From the graphs above, we can safely conclude that a government shutdown has modest impact on the financial market. Equity market fell no more than 2% in the first ten days after the government shut down. The Nov 1995 case saw equity market rallying during the closure.

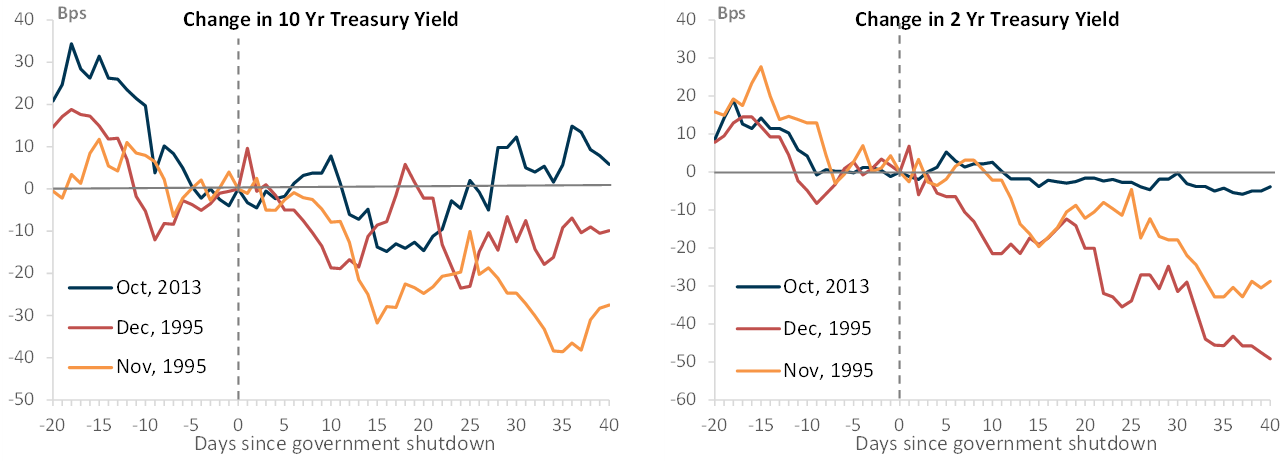

Bond yields/currency: There was no volatile spike in Treasuries yield as one would typically expect from a government that is on the verge of default. In fact, Treasuries yield slide back to its downward trajectory even before the government resume operations. The immediate impact was observed in the Dollar Index (DXY) as the DXY decline immediate in all three cases ending lower in two cases before the government reopened.

If we were to extend our observation to 40 days after the shutdown, we note that in all previous three cases, equity market ended positively and the dollar strengthened as well. Treasuries yield headed lower except in the 2013 case when yield remain higher after the shutdown.

The recommencement of government operation was almost always due to a bi-partisan resolution of the budget spending after which a longer-term bill can be passed. Therefore it will be imperative for one to understand the pivotal point for the current budget negotiation. A failure to conclude on the budget bill can lead to a potential U.S. default as the U.S Treasuries not only run out of funds to operate, but they will also fail to fulfil their debt obligations.

Undocumented Immigrant child in exchange for $25 billion on border security

The two biggest issues delaying the current budget negotiation is on the Deferred Action for Childhood Arrivals (DACA) and defence spending. The Democrats demand that the relief for DACA be tied to any longer-term budget. At the other end, the defence hawks from the Republicans want a larger budget on defence spending.

Both parties are eager for a long-term budget agreement, and any legislation to boost spending by upwards of $250 billion over two years would likely need broad bipartisan backing in both chambers, the Senate as well as the House of Representatives. Although Senate Democrats were willing to give in and not include the DACA in the negotiations, the House Democrats have voiced their disapproval of any deal without a firm commitment to the DACA relief.

On 26 Jan 2018, President Trump threw a lifeline by offering a “legislative framework” for Congress to rely on as an outline for a draft bill. In the framework, Trump was willing to support a path to citizenship for as many as 1.8 million undocumented immigrant children. In exchange, Trumps wants Congress to provide $25 billion for the southern border wall and enhanced security at ports of entry.

Ultimately, a bipartisan budget deal has to be made and signed into law by President Trump to avoid a prolonged government shutdown after 8 Feb 2018.

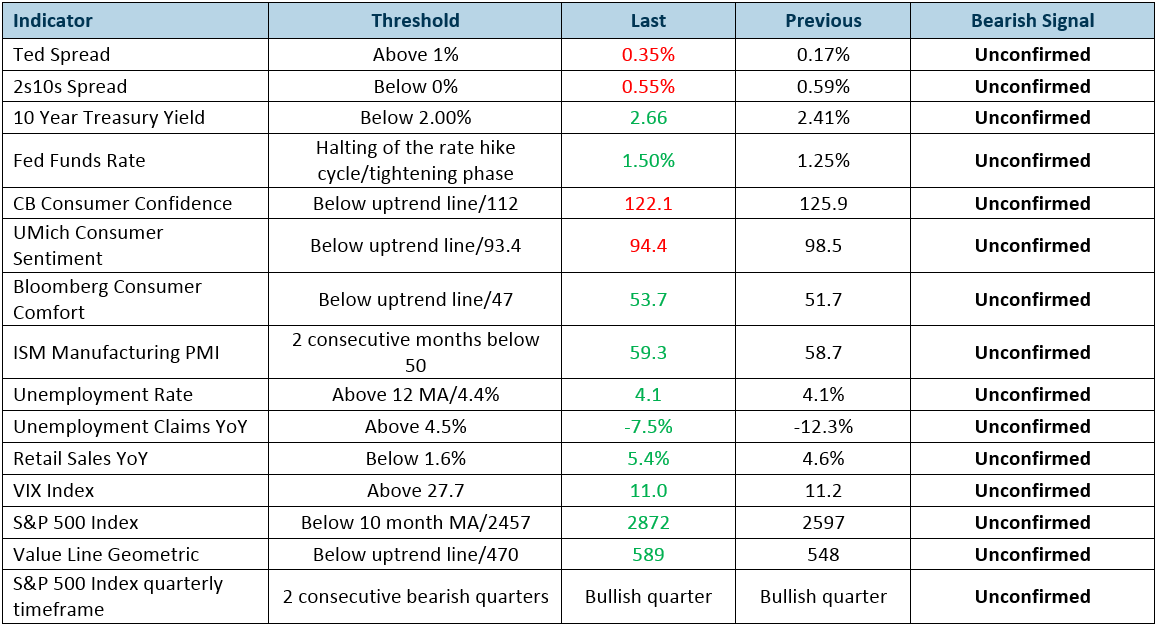

Economy still buoy base on our Recession Indicators

Based on our recession indicators, we are still positive about the US economy and the financial markets.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Sai Teng covers the global macro research. He has more than 6 years investment experience primarily in portfolio construction and asset allocation. He graduated with Bachelor of Science in Banking and Finance from University of London.