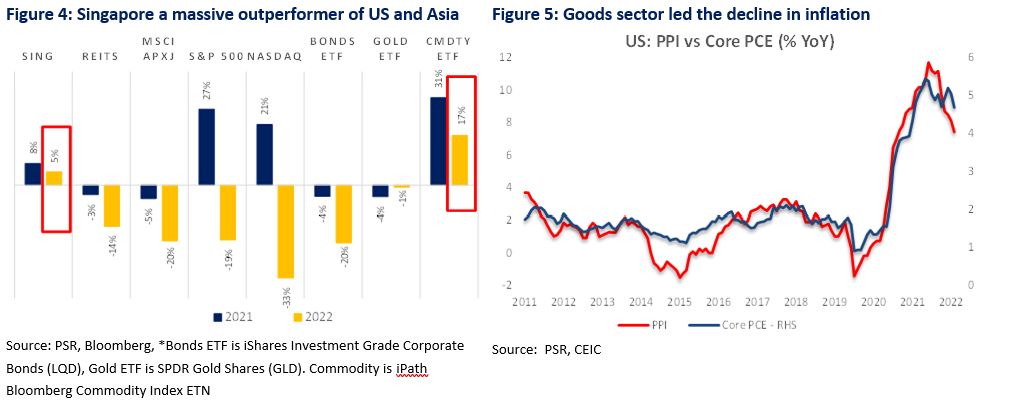

Review: Singapore was a standout outperformer in 2022. In US dollar terms, Singapore equities were up 4.8% in 2022, (2021: +7.7%). A huge 24-25% points outperformance over US and Asia (Ex-Japan) equities. Banks’ performance was resilient as major beneficiaries of rising interest rates and healthy asset quality.

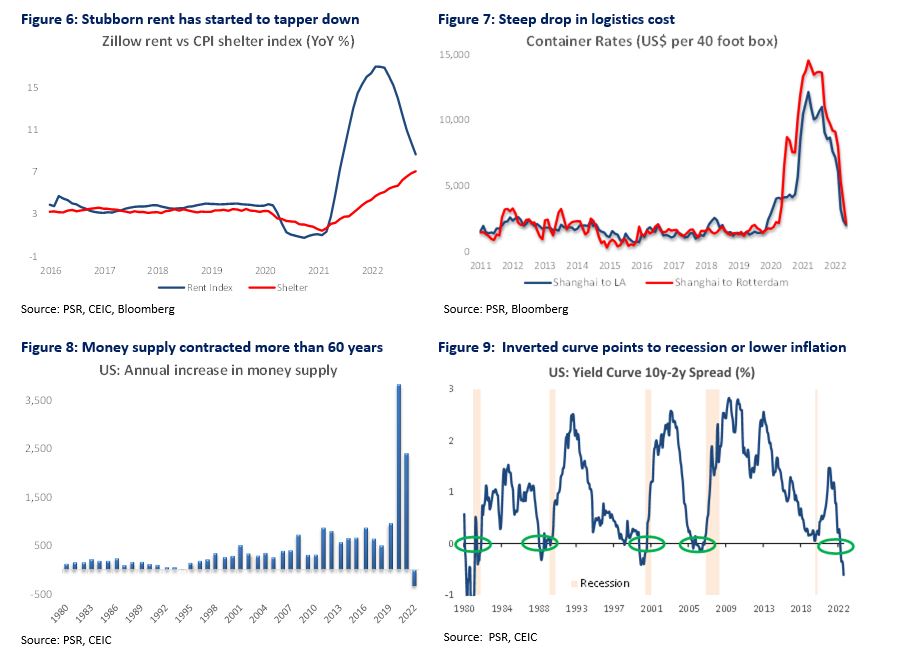

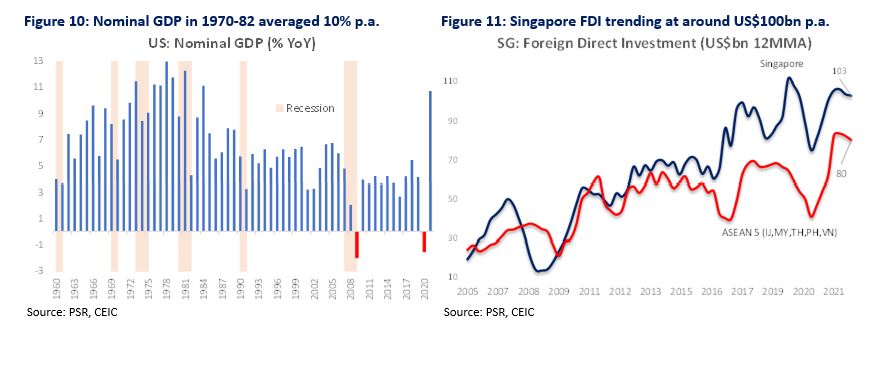

Outlook: The largest pressure point for all asset types in 2022 was larger-than-expected spike in interest rates. We started the year expecting only 0.75% rise by end-2022. Instead, the Fed went for 4.25%. This decimated global equity and bond markets. The Ukraine conflict exacerbated inflation with a surge in commodity prices. The inflation trade of 2022 was long US dollar and short equities and bonds. Our strategy for 2023 is the opposite. We expect inflation to fall sharply this year. Multiple indicators point to a steeper slowdown of inflation in the US. Goods inflation is sharply down (Figure 5), key services such as rents are turning around (Figure 6), freight rates are collapsing (Figure 7), and money supply is contracting (Figure 8). Core PCE (the Fed’s favourite inflation gauge) on an annualized basis is currently 2.6%, close to the Fed’s 2% target. A recession in the US is likely. The yield curve is significantly inverted (Figure 9) and other economic indicators are slowing down. However, we expect any recession to be modest. This is because of strong employment and the absence of deflation shocks reminiscent of the mortgage debt or banking crisis of 2008. A huge deleveraging has taken place but is isolated with the US$2tr collapse in cryptocurrencies. We guess there is a limit to how much of your own (crypto) money you can print to get rich. During inflationary recessions, similar to the 1970s, nominal GDP or operating cash flows did not contract (Figure 10). Over 1970-82, when the US faced four recessions, nominal GDP growth averaged 10% and earnings only fell 3%.

Recommendation: We expect another year of outperformance for Singapore. Sectors we favour are REITs, banks and consumer. The domestic economy is in great shape. Retail sales is trending at 16x pre-pandemic levels (Figure 21). Wage growth is at a 15-year high (Figure 23), job vacancies ample (Figure 24) and foreign direct investments steady at US$100bn plus p.a. (Figure 11). The year-end bonus was the re-opening of China’s borders and removal of COVID-19 restrictions. Tourism constituted 5 percentage points of Singapore’s GDP in 2019. We estimate three-quarters of the Singapore equity index will enjoy a tailwind from China’s recovery. All three local banks have loan and real estate exposure to China. China is the second-largest destination for telcos’ roaming revenue. Listed GLCs benefit from fund management, property development, mall and hospitality ownership in China. With interest rates peaking, we expect a recovery in REIT performance, particularly US REITs listed on the SGX. We believe many are trading at distressed valuations, at 40% discounts to NAV and dividend yields of 14%. As the cost of capital is repriced higher and rationed, companies with high ROEs or cash generators should be re-rated higher, such as HRnetGroup, ComfortDelgro, SGX and Del Monte Pacific.

2022 REVIEW

Singapore was a standout outperformer in 2022. In US dollar terms, Singapore equities were up 4.8% in 2022, (2021: +7.7%). A huge 24-25% points outperformance over US and Asia (Ex-Japan) equities (Figure 4). Banks’ performance was resilient as major beneficiaries of rising interest rates and healthy asset quality.

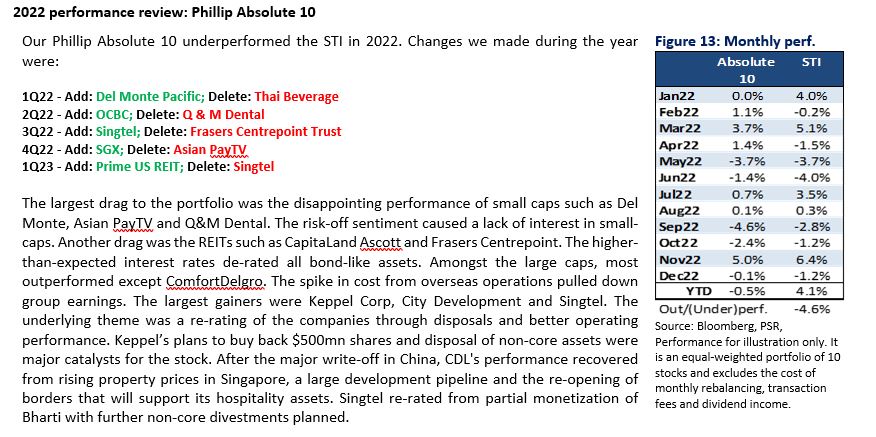

The sector outperformers this year were shipping with gains led by Yangzijiang Shipbuilding (+95%) and Sembcorp Marine (+68%). The upswing in oil and gas and container ship capital expenditure has driven up the order-books of shipyards. Conversely, 2022 was an awful year for REITs. Leading the decline were foreign asset base REITs Manulife US REIT (-55%), Prime US REIT (-51%) or data centres Digital Core (-53%), Keppel DC REIT (-28%).

OUTLOOK

The largest pressure point for all asset types in 2022 was larger-than-expected spike in interest rates. We started the year expecting only 0.75% rise by end-2022. Instead, the Fed went for 4.25%. This decimated global equity and bond markets. The Ukraine conflict exacerbated inflation with a surge in commodity prices. The inflation trade of 2022 was long US dollar and short equities and bonds. Our strategy for 2023 is the opposite. We expect inflation to fall sharply this year. Multiple indicators point to a steeper slowdown of inflation in the US. Goods inflation is sharply down (Figure 5), key services such as rents are turning around (Figure 6), freight rates are collapsing (Figure 7), and money supply is contracting (Figure 8). Core PCE (the Fed’s favourite inflation gauge) on an annualized basis is currently 2.6%, close to the Fed’s 2% target. A recession in the US is likely. The yield curve is significantly inverted (Figure 9) and other economic indicators are slowing down. However, we expect any recession to be modest. This is because of strong employment and the absence of deflation shocks reminiscent of the mortgage debt or banking crisis of 2008. A huge deleveraging has taken place but is isolated with the US$2tr collapse in cryptocurrencies. We guess there is a limit to how much of your own (crypto) money you can print to get rich. During inflationary recessions, similar to the 1970s, nominal GDP or operating cash flows did not contract (Figure 10). They still can grow faster than interest rates due to negative real rates. Over 1970-82, when the US faced four recessions, nominal GDP growth averaged 10%. During these recessions, US corporate earnings contracted around 3% compared to the 20% for the three most recent recessions (2001, 2008/09, 2020).

RECOMMENDATIONS FOR PHILLIP ABSOLUTE 10

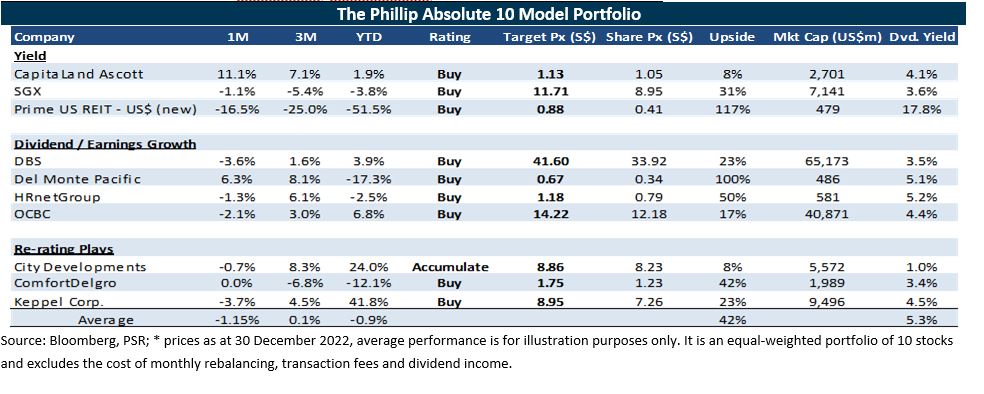

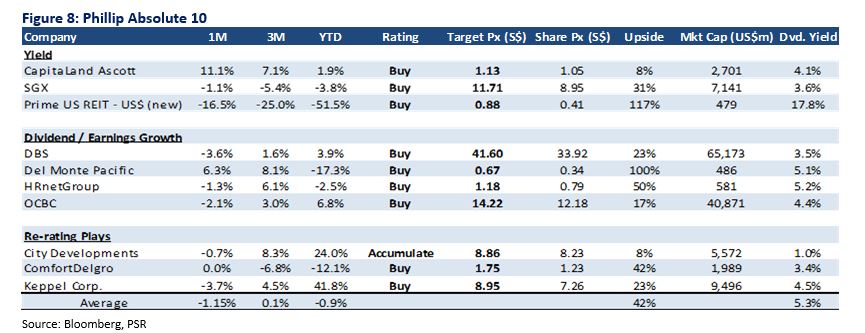

Our focus is on individual stock names to generate alpha in a balanced portfolio. Using 10 stocks for a portfolio is highly concentrated. To avoid excessive volatility in our model portfolio, we add lower beta yield names. In our 2023 model portfolio, which is reviewed every quarter, the top 10 picks – The Phillip Absolute 10 – by category are:

a) Dividend yields: CapitaLand Ascott Residence Trust dividend yield will be supported by the return of global travel, especially with the re-opening of China. Prime US REIT offers attractive valuations of 18% dividend yield and 50% discount to valuations. SGX is to hedge out huge swings in volatility. Its equity and derivatives business will thrive on volatility. Earnings will be supported by rising interest income from the S$14bn collateral it collects from customers.

b) Dividend/Earnings growth: We expect DBS and OCBC to raise dividends from record earnings and excess capital. Del Monte pays an attractive yield with healthy earnings growth. HRnetGroup has huge net cash of S$313mn and an annual operating cash flow of S$70mn to support its annual dividends of S$45mn (divided yield 5%).

c) Re-rating: CDL will ride on the recovery in its hospitality business and recognition of development profits in Singapore. ComfortDelgro’s has exited the pandemic with an even stronger balance sheet and now enjoying the volume recovery in rail and taxi ridership with price increases. Keppel Corp is enjoying a re-rating with more divestments and monetization of non-core assets, in particular the marine portfolio.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.