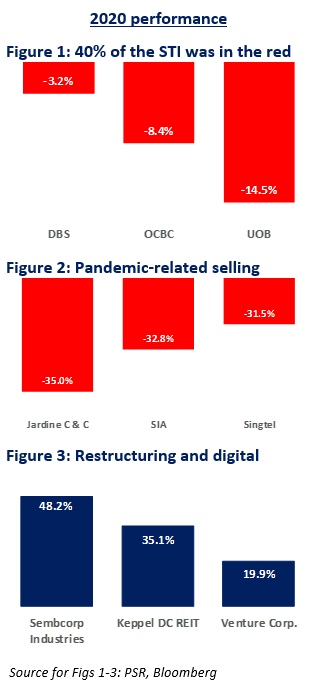

Review: The STI was down 11.8% in 2020. It was the worst performer in Asia, coinciding with Singapore’s worst GDP contraction on record of -6% to -6.5% in 2020. The pandemic triggered consensus earnings to be slashed around 27% this year. The worst-hit sectors were the pandemic epicentres of transportation (-30%) and hospitality REITs (-20%). Sectors that managed to clock gains were industrials (+9%), industrial REITs (+10%) and healthcare (+30%).

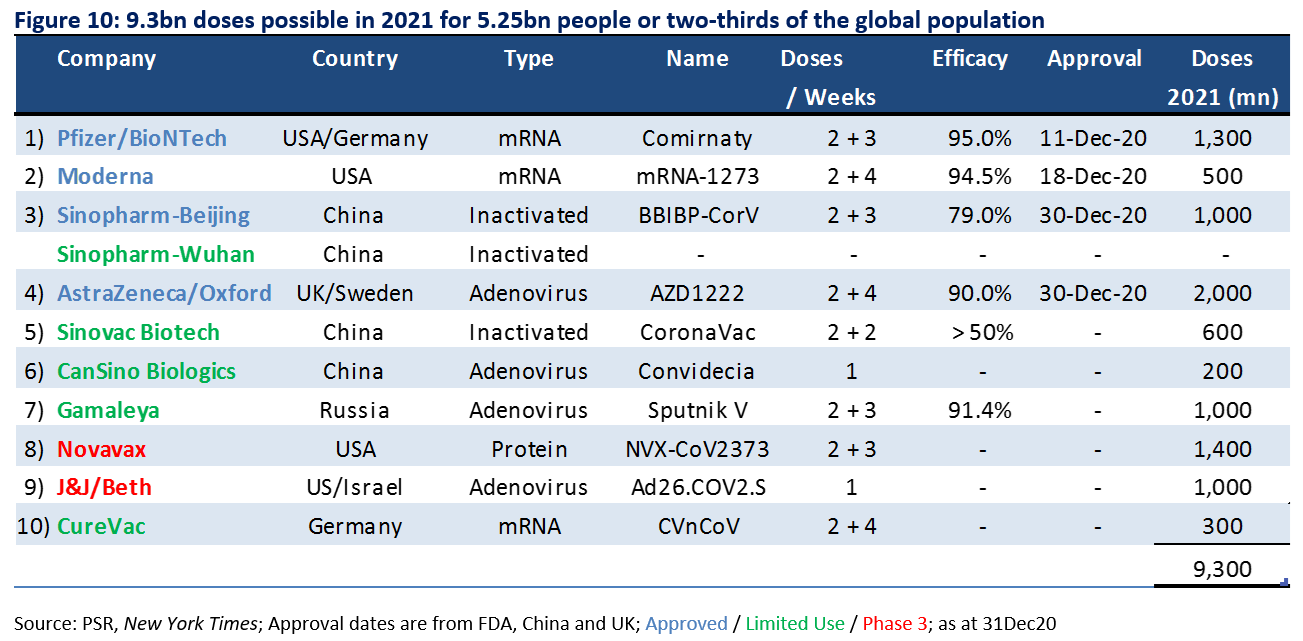

Outlook: We believe Singapore’s equity market is in a sweet spot. Our containment of the pandemic will lead to an earlier and more pronounced economic rebound than many countries, where the pandemic is still raging on. Globally, new COVID-19 cases average 561k per day. In Singapore, community cases averaged one per day over the past week. Phase 3 reopening should add to the economic momentum as bigger group activities resume. Other conditions conducive for an equity rally include low interest rates, undemanding valuations and attractive dividend yields. Vaccines and populist fiscal stimulus offer downside protection to global growth, in our view. Approval of Moderna’s and Pfizer’s vaccines can support 1.8bn doses for 900mn people in 2021. If all the 10 leading vaccines are approved, there is capacity for 9.3bn dosses in 2021, enough to cover two-thirds of the global population and most of the developed markets. Vaccines can bend the infection curve in 2021. Yes, risks remain. The most obvious are vaccine failures to tame mutations of the virus, their side effects or even inefficacy. Other factors that could unsettle markets are monetary-policy misjudgements by the Fed or foreign-policy faux pas by the new U.S. administration. But we think the likelihood of such pitfalls is low.

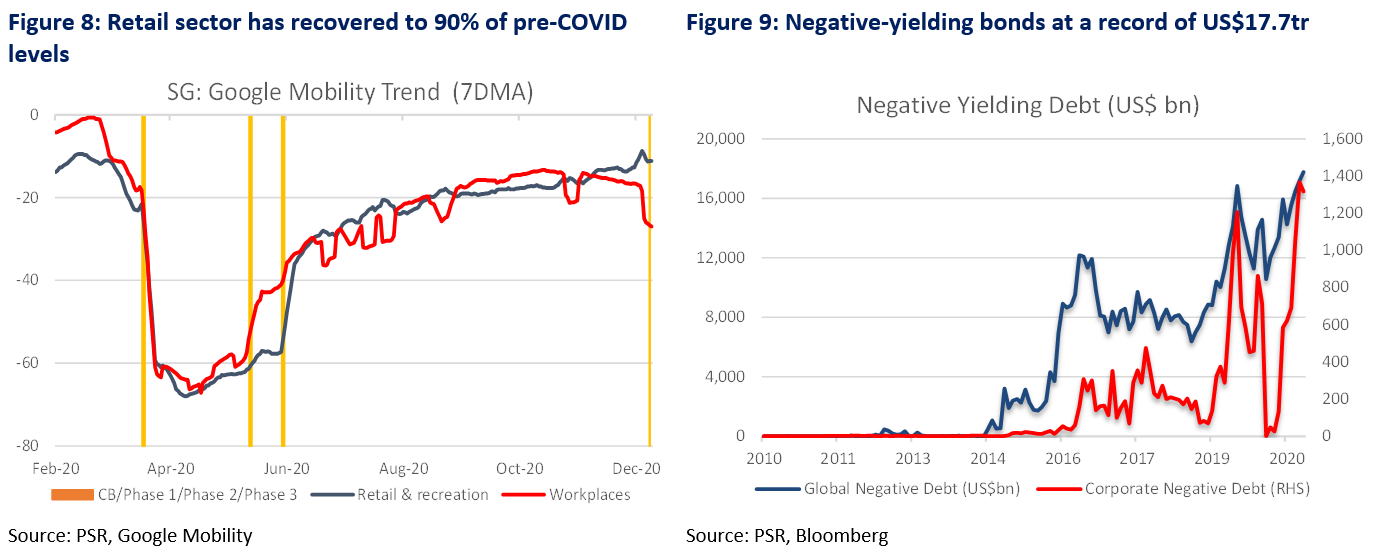

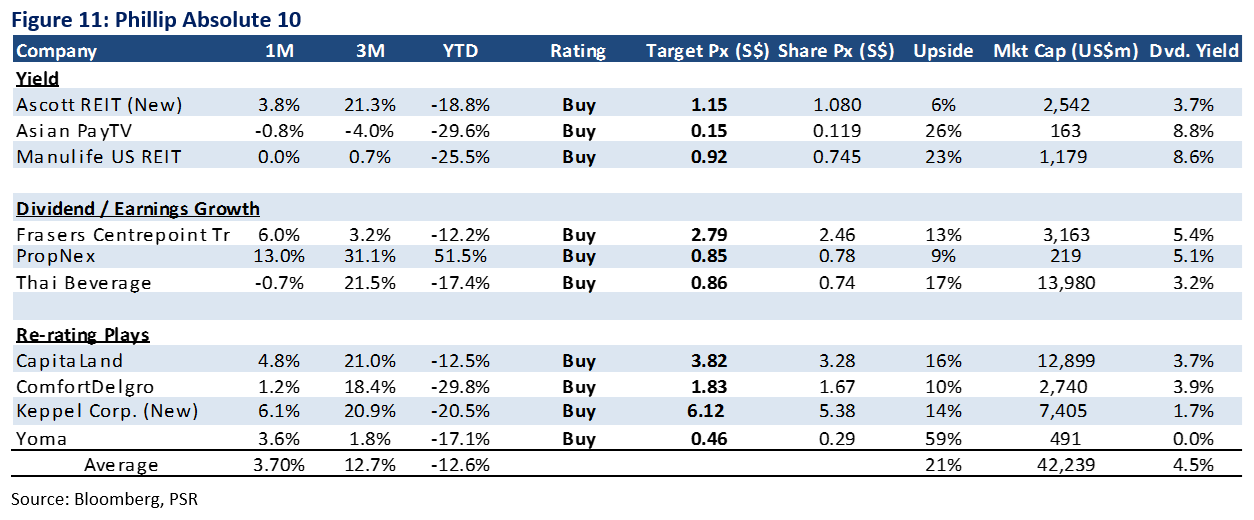

Recommendation: Sectors we favour in 2021 are hospitality, banks and REITs. We are taking a longer-term stance on hospitality. Pent-up demand for travel is likely to result in a prolonged upcycle for the hospitality industry. Airline stocks may be tantalising after their steep drops amid expectations of a return of travel but we have our concerns. Firstly, competition in the industry has not abated due to support from governments. Secondly, airlines are now even more leveraged than before the crisis. In the banking sector, we expect multiple headwinds to change direction. As our economy comes out of lockdown and loan moratorium ends, we expect the aggressive pre-emptive provisioning to reverse. The next positive could be the MAS’ removal of dividend caps. This has already come to pass in some jurisdictions. A corollary tailwind will be better loans growth as economic uncertainties recede. Where REITs are concerned, the pandemic has introduced unwonted volatility for risk-averse yield investors. Both asset values and dividend payments suffered in 2020. With global negative bonds at a record US$17.7tr, the search for yield remains integral to our equity strategy. Our preference is U.S. REITs for their attractive 9% yields. While work-from-home trends had already taken root in the U.S. before the pandemic, average leases of five years should anchor near-term yields, even if some tenants shift more aggressively and permanently to home-based work arrangements.

2020 REVIEW

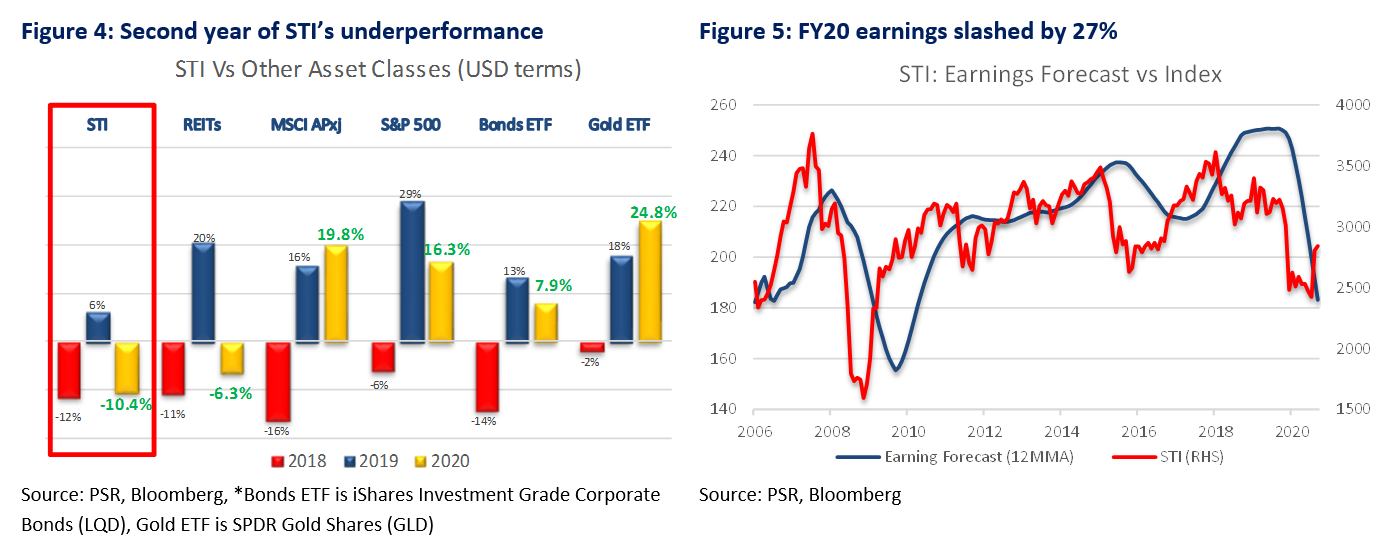

The STI was down 11.8% in 2020. It was the worst performer in Asia, coinciding with Singapore’s worst GDP contraction on record of -6% to -6.5% in 2020. When we compare the STI to other major asset classes such as corporate bonds, gold and U.S. markets, 2020 was its second (or even third) consecutive year of underperformance, in USD terms (Figure 4).

The pandemic triggered a slash in consensus earnings by around 27% for 2020, primarily due to banks, telcos and aviation (Figure 5). The worst-hit sectors were the pandemic epicentres of transportation (-30%) and hospitality REITs (-20%). Other sectors similarly affected by the pandemic were even worst hit. They included telecommunications (-27%) and ship/marine yards (-37%). Sectors that managed to clock gains were industrials (+9%), industrial REITs (+10%) and healthcare (+30%).

OUTLOOK

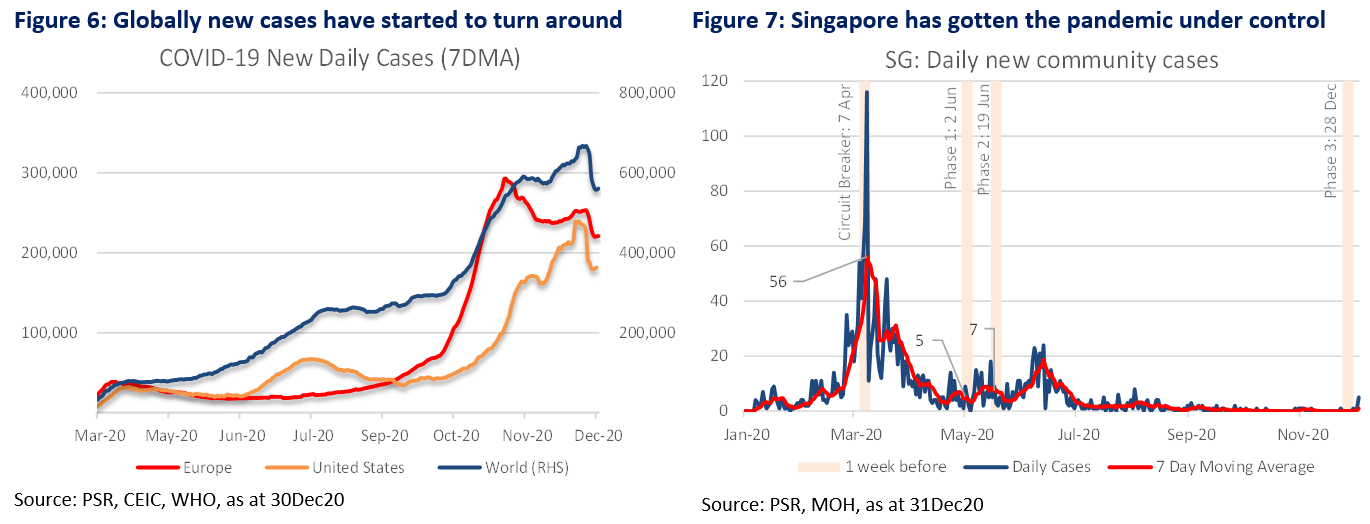

We believe the Singapore equity market is in a sweet spot. Containment of the pandemic has led to an earlier and more pronounced economic rebound than many countries, where the pandemic is still raging on. Globally, new COVID-19 cases average 561k per day (Figure 6). A positive is the infection curve is bending albeit at very elevated levels. In Singapore, community cases averaged one per day over the past week due to a recent surge (Figure 7). Phase 3 reopening in Singapore should accelerate the economic momentum as restrictions on group activities are further relaxed (Figure 8). Other conditions conducive for an equity rally include low interest rates (Figure 9), undemanding valuations and attractive dividend yields. Vaccines and fiscal stimulus offer downside protection to global growth, in our view. Approval of Moderna’s and Pfizer’s vaccines can support 1.8bn doses for 900mn people in 2021. If all the 10 leading vaccines are approved, there is capacity for 9.3bn dosses, enough to cover two-thirds of the global population in 2021 (Figure 10). Vaccines can bend the infection curve in 2021.

With vaccines dominating all the headlines and an economic boom in 2021 forecast by just about every economist and government, the question is, has everything been priced in? We think No, looking at the large underperformance of our equity market. Yes, risks remain. The most obvious are vaccine failures to tame mutations of the virus, their side effects or even inefficacy. Other factors that could unsettle markets are monetary-policy misjudgements by the Fed or foreign-policy faux pas by the new U.S. administration. But we think the likelihood of such pitfalls is low.

5 themes for 2021

✓ A boom in global growth

✓ Vaccines to bend the infection curve

✓ Interest rates remain conducive

✓ Prolonged growth in tourism

5 themes we had for 2020

✓ Trade ceasefire

× Recovery in the domestic economy

✓ Buoyant electronics sector

✓ Binary political events

× Less momentum from interest rates

RECOMMENDATIONS FOR PHILLIP ABSOLUTE 10

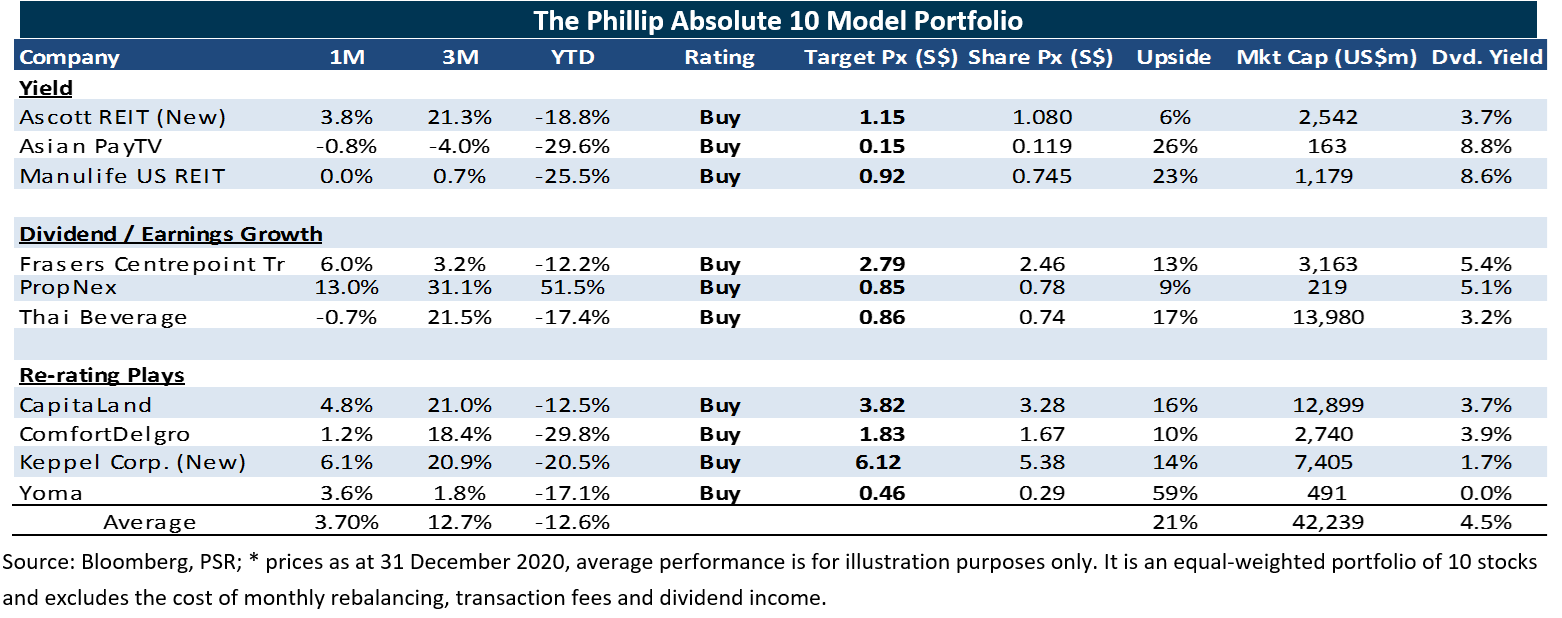

The STI’s relative performance has been poor. Therefore, it is challenging to simply buy beta to find returns. Our focus is on individual names to generate alpha. With our 10 stocks, we look for balanced returns to avoid excessive volatility in our model portfolio. For our 2021 absolute return portfolio, our top 10 picks – The Phillip Absolute 10 – by category are:

STI target. Our target for the STI is 3,200. This is based on 14x PE, its 10-year PE ratio average and earnings rebounding 25%, still 10% below pre-COVID levels. The index is trading at 15x PE on depressed earnings.

2020 performance review: Phillip Absolute 10

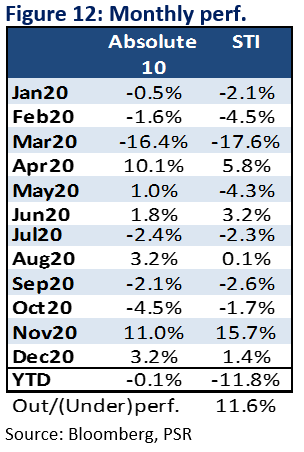

Our Phillip Absolute 10 outperformed the STI in 2020. Changes we made during the year were:

1Q20 – Added: Fraser Centrepoint, StarHub; Deleted: SGX, DBS

2Q20 – Added: Thai Beverage; Deleted: Singtel

3Q20 – Added: Yoma Strategic, Asian PayTV, DBS; Deleted: StarHub, Sheng Siong, UOB

4Q20 – Added: ComfortDelGro, Manulife US REIT, SGX; Deleted: Ascott REIT, DBS, Venture Corp.

1Q21 – Add: Ascott REIT, Keppel Corp.; Deleted: NetLink Trust, SGX

Our portfolio suffered tremendously when COVID-19 struck in 1Q20. It took us the next three quarters to recover all the losses. We bore the brunt of the selling from our exposure to Ascott REIT, DBS, Singtel and FCT. Major winners for us were Sheng Siong, Venture Corp, PropNex and Thai Beverage. Sheng Siong was supercharged by a spike in grocery sales during the lockdown. Venture recovered from disruptions in its Malaysian operations with increased dividends and resilient earnings. PropNex gained market share as property sales performed better than expected. Thai Beverage endured an alcohol ban in Thailand and increased regulatory oversight of alcohol consumption in Vietnam to report resilient earnings. The company took aggressive steps to contain cost.

Sector Narratives

Download the full report to the in-depth sector and technical views, here.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.