|

Review: YTD19, the STI is up 4%. We fell short against the benchmark MSCI Asia Ex-Japan (MAXJ)’s rise of 11% (SGD terms). The STI has underperformed MAXJ in four out of the past five years. We lack the earnings growth and re-rating theme. This has resulted in STI valuations being stuck in a tight range. A new source of fund-flow could be a re-rating trigger. When reviewing sector performance, REITs stood out as the best performer in 2019. We entered 2019 with expectations of two rate hikes. Instead, we faced the “Powell pivot” and experienced three rate cuts in 2019.

Outlook: In 2020, we think the Singapore economy could surprise on the upside. Firstly, the economic backdrop globally is expected to recuperate after two years of deceleration led by the manufacturing sector. Secondly, several key sectors of our economy are starting to recover. Property transaction volumes have rebounded after the malaise post-July 2018 cooling measures. Sales from new launches are up 13% in 2019. The improvement in the property sector supports retail spend and mortgage loans. The construction sector is on the mend with contracts awarded at four-year highs. Thirdly, the macro setting is turning positive. Foreign direct investments in Singapore are at record levels of US$108bn. Employment growth is the fastest in almost five years. There will be several political events to eyeball in 2020. Of course, we have our own Singapore elections. Past elections have not seen any meaningful impact on the stock market. Another notable event will be the Democratic Primaries. If Elizabeth Warren secures the presidential nomination, we can expect a knee jerk sell down in U.S. equities. On the dreaded trade war, our base case is a truce via the Phase 1 deal. We believe the deal has a better chance in this period because i) Trump is heading into Presidential election, of which he will not wish to risk further deceleration in the US economy; ii) Headlining Phase 1 deal to provide both sides with the legroom to claim victory that more concessions and assertion should be attained in Phase 2, and iii) A desire to avoid 15 December punitive tariffs on the U.S. consumer.

STI Target: We are raising our STI target from 3400 to 3700. The improvement in growth and re-rating potential could surprise on the upside. This pegs the market at 15x PE FY20e.

|

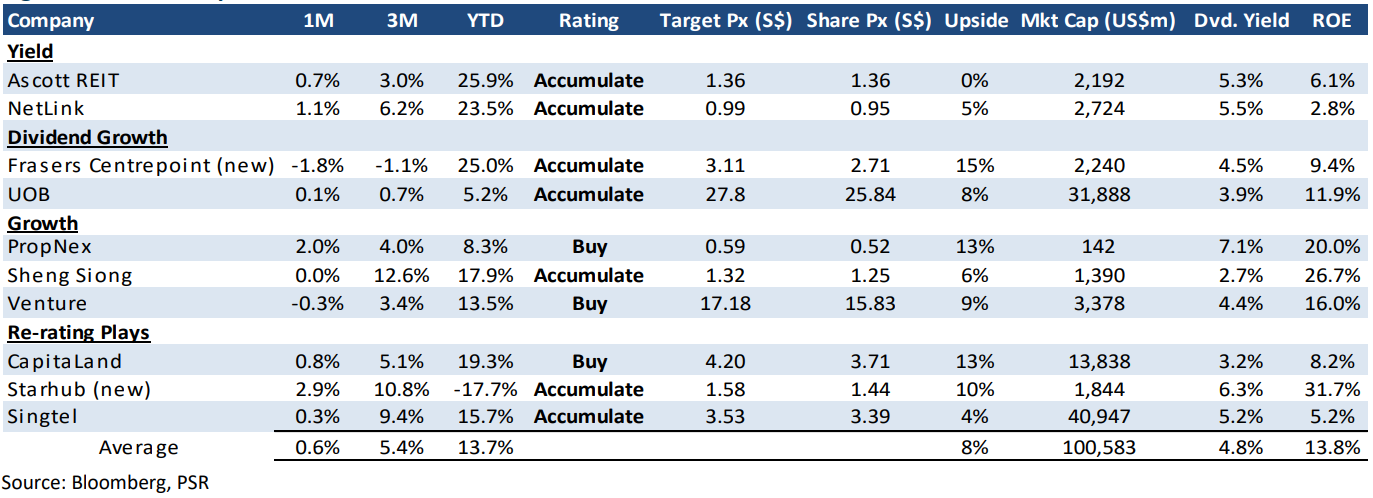

Recommendation: Our model portfolio – Phillip Absolute 10 – outperformed the STI in 2019. Our best performers include SGX, Capitaland, Sheng Siong and Ascott REIT. We are removing SGX due to the share price performance and expectations of reduced (Trump driven) market volatility. We replaced SGX with StarHub. StarHub is on a path to recovery. The problematic pay-TV business should improve with more variable content contracts and a steadier subscriber base. As for mobile, we believe it is past the peak of the competitive intensity. We are replacing DBS with Frasers Centrepoint. 1H20 will be challenging for banks as net interest margins roll-over and loans growth stay tepid. Sheng Siong will deliver consistent earnings growth from new stores and a recuperating retail sector will be helpful. CapitaLand’s journey to building more recurrent earnings continues. Venture is our exposure to a rebound in the electronics sector driven by 5G and supply chain de-risking from China to Southeast Asia. We like PropNex’s huge market share, attractive yield and recovery in property transaction volumes.

|

2019 REVIEW YTD19, the STI is up 4%. We fell short against the benchmark MSCI Asia Ex-Japan (MAXJ)’s rise of 11% (SGD terms). The STI has underperformed MAXJ in four out of the past five years. We lack the earnings growth and re-rating theme. This has resulted in STI valuations being stuck in a tight range. When reviewing sector performance, REITs stood out as the best performer in 2019. We entered 2019 with expectations of two rate hikes. Instead, we faced the “Powell pivot” and experienced three rate cuts in 2019. As the year progressed, the slowdown in the global economy, led by manufacturing-stoked fears of a looming recession swayed by the inverted yield curve and escalation of tariffs between the U.S. and China. Stocks that performed the best were driven more by bottoms-up company-specific drivers rather than a broad macro driver.

OUTLOOK In 2020, we think the domestic Singapore economy could surprise on the upside. Firstly, the economic backdrop globally is expected to recuperate after two years of deceleration led by the manufacturing sector. Secondly, several key sectors of our economy are starting to recover. Property transaction volumes have rebounded after the malaise post-July 2018 cooling measures. Property sales from new launches are up 13% in 2019 and accelerating. The improvement in the property sector supports retail spend and mortgage loans. The construction sector is on the mend with contracts awarded at four-year highs (Figure 8). Even the moribund retail sector is registering some stability (Figure 9). Thirdly, the macro setting is turning positive. Foreign direct investments in Singapore are at record levels of US$108bn (Figure 10). After two consecutive years of decade-low population growth, Singapore manage to eke out an improvement in our population growth (Figure 11). |

There will be several political events to eyeball in 2020. Of course, we have our own Singapore elections. Past elections have not seen any meaningful impact on the stock market. Another notable event will be the Democratic Primaries. If Elizabeth Warren secures the presidential nomination, we can expect a knee jerk sell down in U.S. equity markets. Then there are the November Presidential elections. Maybe, only Michael Bloomberg can save the following four years. On the dreaded trade war, our base case is a truce via the Phase 1 deal. We believe the deal has a better chance in this period because i) Trump is heading into Presidential election which he will not wish to risk further deceleration in the US economy; ii) The headline Phase 1, can provide both sides with the legroom to claim victory that more concessions and assertion could be attained in Phase 2; and iii) A desire to avoid 15 December punitive tariffs on the U.S. consumer.

|

RECOMMENDATION There is no single underlying theme in our portfolio. Our selection is purely a bottom-up balanced portfolio of stock picks which we hope to generate alpha. We look for balance returns in our model portfolio. For our 2019 absolute return portfolio, our top 10 picks – The Phillip Absolute 10 by categories are:

a) Dividend Yield: Ascott REIT and Netlink Trust are the yield anchors to our portfolio. Around 40% of Ascott revenues are income protected (master lease and income guarantees) and the balance is diversified across nine geographies. Netlink is your residential fibre provider monopoly enjoying regulated returns. Incremental to earnings growth will be connections for 5G deployment and penetration in commercial fibre business. b) Dividend Growth: We expect UOB to grow their dividends in view of their 7% earnings growth in FY19e. Frasers Centrepoint is a new addition. Growth will come from the rise in captive HDB population for their malls and likely inorganic growth from a pipeline six suburban mall assets in PGIM fund held by its sponsor. c) Growth: The recovery in HDB transactions and a large number of new property launches will be supportive of PropNex earnings growth in FY20. We expect another year of growth for Sheng Siong as they grow the stores, market share and margins. Venture will ride on the shift in global electronics supply chain into Southeast Asia and an improvement in electronics demand from improving Sino-US trade relationship. d) Re-rating: CapitaLand is scaling up its lodging and asset management fee income. We view this as a higher quality income and will re-rate the valuation of the company. We are expecting Starhub pay-TV operations to improve as customers are locked in two years and the content cost is gradually restructured. We think mobile competition has peaked and intensity will subside. We expect Singtel’s associate Airtel to improve group earnings, after a brutal price war, the wireless market in India is currently going through a series of price hikes.

STI target. We are raising our STI target from 3400 to 3700. The improvement in growth and re-rating potential could surprise on the upside. This pegs the market at 15x PE FY20e. |

|

2019 Performance Review – Phillip Absolute 10 |

|

Our Phillip Absolute 10 outperformed the STI in 2019. Below were some of the changes we made during the quarters.

1Q19 Add: SGX, Keppel DC REIT, China Sunsine; Remove: Chip Eng Seng, Micro-Mechanics, Banyan Tree 2Q19 Add: NetLink Trust, Ascott REIT, Singtel; Remove: Ascendas REIT, CCT, Geo Energy 3Q19 Add: DBS, APAC Realty; Remove: China Sunsine, Keppel DC REIT 4Q19 Add: Venture Corp, PropNex; Remove: ComfortDelGro, APAC Realty

|

The portfolio was dragged down in 1H19 by some of our growth stocks such as China Sunsine and Geo Energy. Earnings severely disappointed with both stocks. Keppel DC REIT was a hindsight miss, as we took profits too early as we felt valuations were stretched. We switched our income-generating stocks in 2Q19 with NetLink and Ascott REIT. In the 3Q19, we included our first mid-cap stock – real estate agency APAC Realty. We exited ComfortDelGro as taxi industry continues to lose market share to private hire vehicles and rail business was hit by several charges. In 4Q19, we added Venture as a beneficiary of recovery in electronics industry plus swapped APAC Realty with PropNex due to the latter’s better execution.

|

Sector Narratives 1. Consumer: Consistent with our domestic recovery theme, we expect consumer spending to improve in 2020. Wage and job growth will support spending and even an improvement in property sales. 2. Finance: We still view banks as dividend growth stocks due to their single-digit earnings growth profile and well-capitalised balance sheets. Nevertheless, we expect 1H20 to be weak for the banks namely from lower interest margins and tepid loans growth. 2H20 should see better performance as the recovery in macro conditions becomes less ominous. 3. Healthcare: The hospital admission data has surprisingly turned positive and even medical tourism has been better. However, high valuations and higher risk profile (as the sector ventures overseas) will cap any upside in share prices. 4. Property: We have been surprised by the share price performance of property stock especially with the huge uncompleted supply yet to be launched. With 40 to 50 launches a year, take-up rates have understandably been low at 20%. We prefer the real estate agents over developers. Agencies have concentrated market shares, will benefit from improvement in volumes and not underwrite the potential losses from unsold inventory (or the punitive stamp duties). 5. REITs: It was a windfall year for REITs. We moved from expecting two rate hikes to receiving three rate cuts in 2019. This five cut swing in expectations will not occur in 2020. My expectations are flat price performance and to just collect your dividends as returns. 6. Technology: Pretty bullish on this sector – 3 reasons: (a) recovery in overall global manufacturing; (b) roll-out of new structural technologies like 5G and continued penetration of electronics into mainstream automobiles (infotainment, LEDs, seating, etc) and hybrid vehicles (due to emission standards especially in Europe); and (c) supply chain migration to Southeast Asia – including Malaysia. 7. Telecommunications: Not too worried about the fourth mobile operator. If there was a profit opportunity, the service would have already been rolled out and not just an unlimited free trial at present. MVNOs have closed any profit pools left for TPG. 8. Transportation: It has been challenging for the taxi industry in Singapore. The number of private hire vehicles is growing at a rate that is equivalent to the current fleet of taxis every 18 months. |

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: