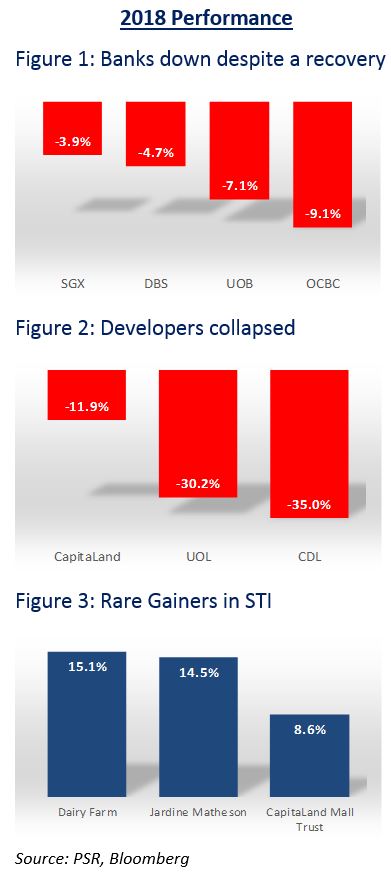

Review: 2018 was a turbulent year for the STI, which lost 9.8%. From a peak of 3641 in May, it corrected by 19% over six months to a low of around 3000. Only 6 of 30 STI component stock registered any gains. We had been bullish for 2018. There was momentum in the economy and rising interest rates was positive for our heavily-financial-weighted STI. However, as the year progressed, we ran into a wall of issues. Firstly, a new tail risk surfaced when the U.S. President began a series of tariffs on Chinese goods, sparking tensions between the U.S. and China. Secondly, strength in the US dollar plus rising interest rates triggered a violent retreat of liquidity from emerging markets. Thirdly, China’s deleveraging resulted in slower-than-expected growth in its economy. In Singapore, property-cooling measures smothered whatever momentum left in the economy. Singapore’s GDP halved from plus 4.6% YoY in 1Q18 to 2.2% in 3Q18. Our initial 3,900 target for the STI bit the dust.

Outlook: The Singapore market is cheap on a historical basis. On a forward PE of 12x or PB of 1x, STI is trading at 1 SD of its 10-year historical valuations. The driver to returns will be a reversal of portfolio outflows back to Asia and Singapore: 1) We are expecting a rolling over of U.S. data. U.S. growth has been boosted by the steepest fiscal stimulus since the GFC; 2) We anticipate more turmoil in U.S. politics. With the Democrats taking over majority in the Lower House, we expect them to launch multiple investigations, with the Mueller probe leading the troupe; 3) Slower economic conditions have tempered the Fed’s rate-hike enthusiasm. Commentary is now tilted towards raising rates to that neutral level rather than exceed it. This is a range of 2.5%-3.5%; 4) Final puzzle will be trade negotiations between China and the U.S. We expect a negotiated truce. We are assuming Trump is not dogmatic but deal-driven. He has reversed many hard stances before, from Iran sanctions to war with North Korea. As we approach 2020 U.S. elections, the last thing needed is a disruption to the economy or financial markets, either from a further implosion of global trade or higher consumer product prices.

STI Target: We cut our STI target twice this year, to 3,400 in October. We maintain this target for 2019. This pegs the market at 13.5x (or around its 10-year average valuation).

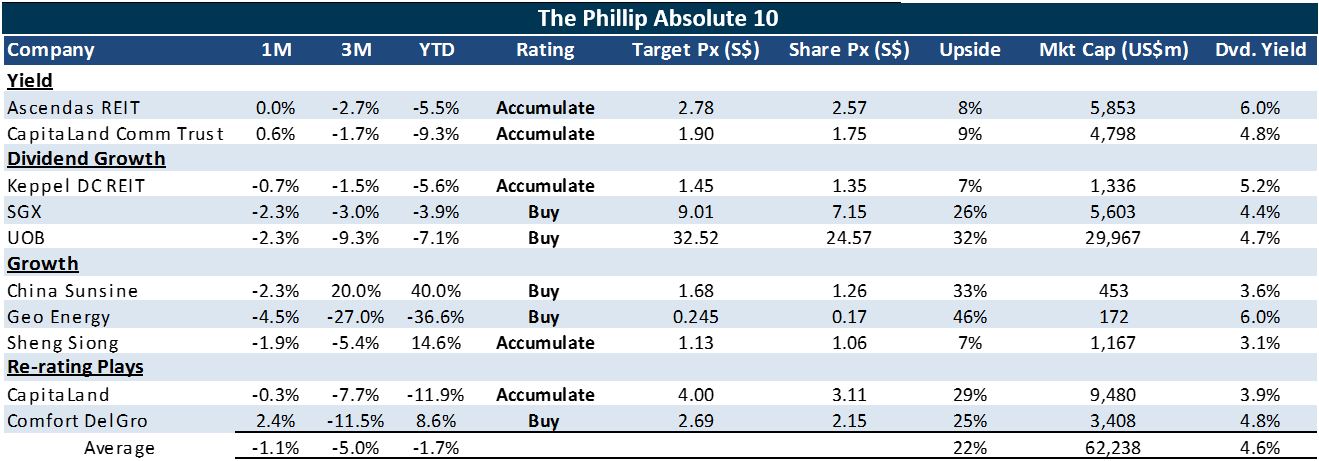

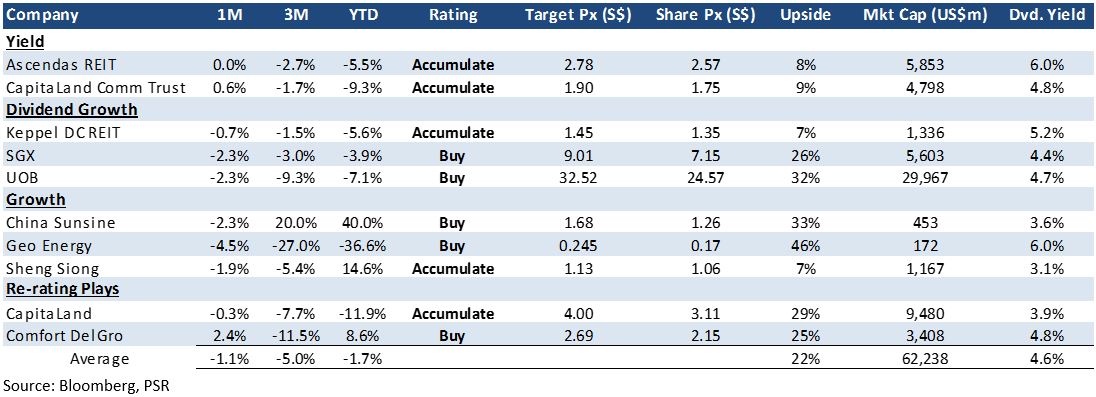

Recommendation: We advocate a lower-beta equity portfolio for 2019. Our emphasis is on dividend-paying stocks. In our Phillip Absolute 10 for 2019, our top picks are: a) UOB for its attractive dividends, well supported by the bank’s excess capital; b) SGX, whose derivatives business is growing as much as 20%; c) On REITs, we opt for Ascendas for its stable dividends, CCT for the attractive demand-supply dynamics for office market and Keppel DC for the structural growth of data centres; d) Growth stock are Geo Energy, as coal production recovers in 2019. Sheng Siong is gaining market share and rolling out record new stores. China Sunsine will maintain healthy earnings growth as supply is constrained by China’s strict environmental regulations; e) Re-rating picks are ComfortDelGro and CapitaLand.

2018 REVIEW

The year began with worries over rising US Treasuries. But the STI still managed to climb higher as the Singapore economy grew 4.6% in 1Q18. A new uncertainty emerged when President Trump declared that trade wars were good and could be won. His commentary and policies started to rock equity markets. Relative strength of the US economy and dollar began to rattle emerging markets. Argentina and Turkey had to raise interest rates by as much as 68% and 24% respectively to contain their currency devaluation. Despite the above, the STI managed to touch a high of 3641 in early May, propelled by strong banking performances.

As we entered the second half of 2018, the market started to relent to growing signs that global economic growth had peaked. There were also clearer signs that the trade skirmish between the U.S. and China was turning into an all-out trade war. While the immediate economic impact was manageable, with direct global GDP affected at most by 0.5% point, the uncertainty and accompanying caution in spending was more pervasive and damaging. It also did not help our equity market when a new round of cooling measures were slapped on Singapore’s residential property market. This sucked out whatever economic momentum was left in the domestic economy

OUTLOOK

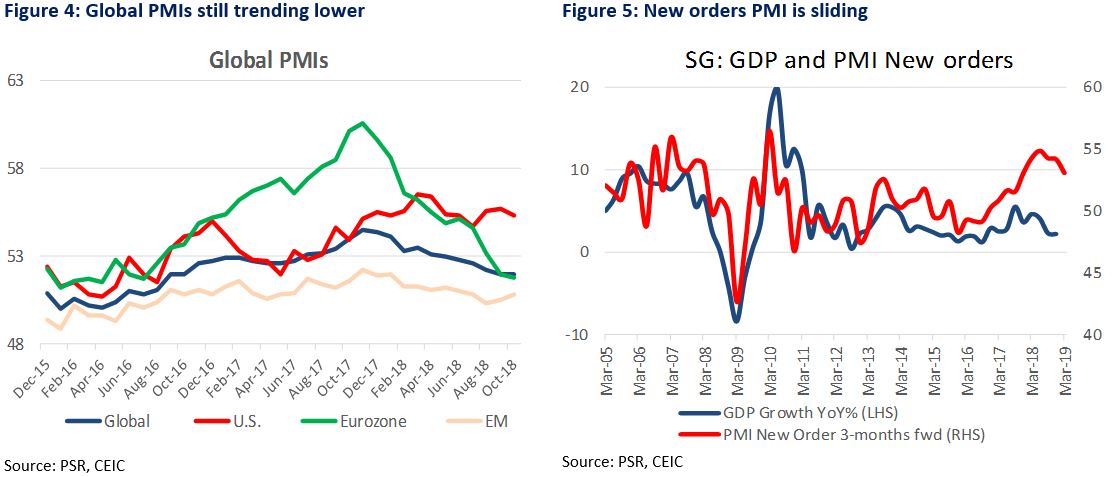

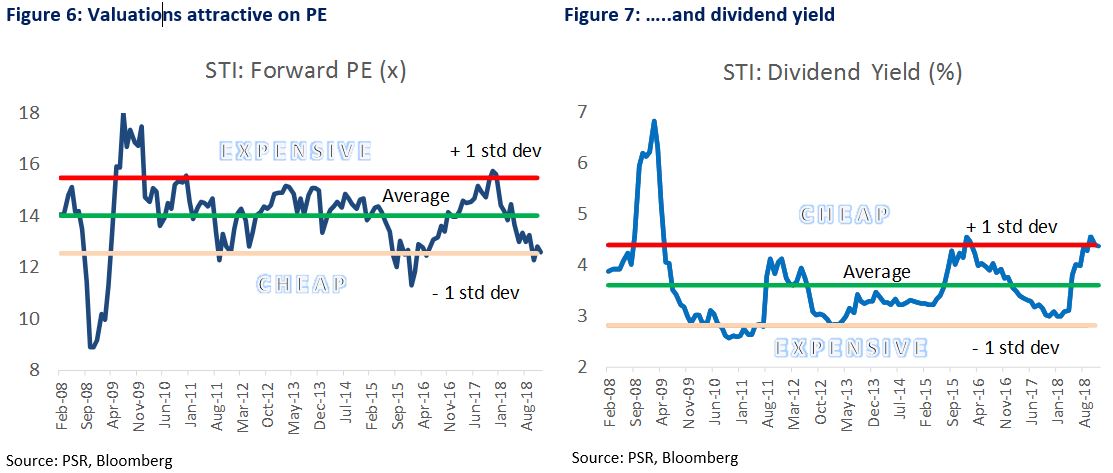

Despite the slowing momentum (Figure 4), we still expect positive returns for the Singapore market in 2019. Valuations are attractive. The STI is trading at 12x forward PE or 1 standard deviation its 10-year average (Figure 6). Dividend yields of 4.5% are around the highest after GFC (Figure 7). But attractive valuations alone are not a sufficient trigger for positive returns. We believe a major catalyst in 2019 will be a reversal of funds back into Singapore and Asia.

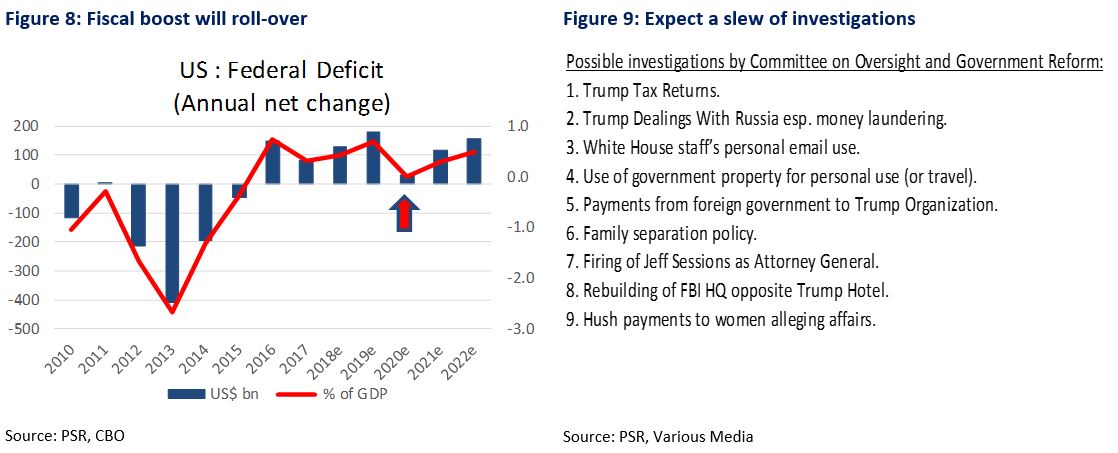

Firstly, we are expecting U.S. data to roll over. U.S. growth has been boosted above trend, courtesy of a 1.1%-point fiscal stimulus from the Trump tax cut (Figure 8). This is the steepest fiscal boost since GFC.

Secondly, we anticipate more turmoil in U.S. politics. With the Democrats taking over a majority in the Lower House, we expect them to launch multiple investigations, likely with the Robert Mueller probe leading the troupe. The new Lower House Committee on Oversight and Government Reform controlled by the Democrats will “Make Subpoenas Great Again” (Figure 9).

Thirdly, slower economic conditions have tempered the Fed’s rate-hike enthusiasm. Commentary is now tilted towards raising rates to its neutral range of 2.5%-3.5% rather than exceeding it. Market expectations are for two hikes in 2019. In the December FOMC meeting, expectations for 2019 inflation and median dot plots have fallen to 1.9% (from 2%) and 2.875% (from 3.1%). The pressure to raise rates has eased. Worry is now on the Fed reducing its balance sheet by US$50bn per month from its initial US$10bn per month target in October 2017. The market is concerned about the effects of this unprecedented quantitative tightening. We are more sanguine. Excess liquidity parked at the Fed by US banks totalling US$1.7tn can potentially absorb the Fed’s sale of Treasuries. We doubt the balance-sheet contraction will meaningfully hurt loans growth or money supply in the U.S. More critical is the demand for rather than supply of credit in the U.S.

Finally, we expect a negotiated truce between China and the U.S. We are assuming President Trump is not dogmatic but deal-driven. He has reversed many of his hard stances before, from Iran sanctions to war with North Korea. Recall that in August 2017, President Trump declared that any provocation of the U.S. by North Korea would be met with “Fire and Fury”. Ten months later, both leaders were shaking hands on TV. Elsewhere, Trump threatened Iran with “consequences…few throughout history have ever suffered before”. Less than four months later, the US waived its sanctions for 180 days for major Iranian oil buyers such as China and India. And a month later, it will withdraw troops from Syria. Another reason we expect some trade truce is the approaching 2020 U.S. presidential elections. We think the last thing Trump wants is a disruption to the economy or financial markets, either from the trade war or higher consumer product prices. Trump has repeatedly linked the rally in the U.S. stock market to his Presidency. Another interested party to resolve the dispute with China will be the largest donor to the Republican party and Trump 2016 campaign. He has casinos in Macau.

RECOMMENDATION

We advocate a lower-beta equity portfolio for 2019. Until economic data starts to stabilise, our emphasis is on dividend-paying stocks. For our 2019 absolute return portfolio, our top 10 picks – The Phillip Absolute 10 – are:

a) Dividend Yield: Ascendas REIT for yield stability anchored by more than 100 properties. A large part of its portfolio is in resilient business parks or office space and high-tech factories. CapitaLand Commercial Trust is expected to book positive rental reversions from improving demand-supply of office space.

b) Dividend Growth: UOB’s attractive dividends should be well supported by its excess capital. Its business is also less exposed to any deceleration in the Chinese economy. SGX’s derivatives business is growing by as fast as 20%. Derivatives now account for almost 50% of its revenue, up from 22% in FY11 (Figure 44). Keppel DC is fast expanding its data-centre business through M&As. It can arbitrage the difference in private market yields and its own lower cost of capital.

c) Growth: Geo Energy’s coal production should recover in 2019. Sheng Siong is gaining market share and opening a record number of new stores. China Sunsine’s healthy earnings growth should be supported by tight supply from China’s strict enforcement of environmental regulations.

d) Re-rating: ComfortDelGro’s prospects will improve from lower taxi competition and more bus contracts overseas. CapitaLand continuously builds up more recurrent and quality earnings from investment properties and other property asset cum funds under management.

STI target. We cut our STI target twice this year, to 3,400 in October. We maintain this target for 2019. This pegs the market at 13.5x (or around its 10-year average valuation).

Figure 10: The Phillip Absolute 10

2018 Performance Review – Phillip Absolute 10

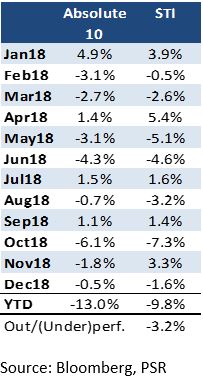

Our inaugural Phillip Absolute 10 underperformed the STI. The initial drag came from disappointing results and dividends from Asian PayTV. We exited this stock in August. We took profit on DBS and replaced it with OCBC in March. Other stocks in our portfolio that severely underperformed were: (i) Geo Energy – despite healthy coal prices, production and costs were below our expectations; (ii) Micro-Mechanics – the semiconductor down cycle hurt it more severely than expected; (iii) Chip Eng Seng – performed well operationally but cooling measures precipitated a massive de-rating of all property stocks.

Gainers in our portfolio were: (i) ComfortDelGro as competition in taxi industry abate following the exit of Uber; (ii) Banyan Tree, which gained traction from collaboration with new partners Accor and China Vanke.

Figure 11: Monthly moves

My Sector Narratives

1. Commodities – Coal: 2018 was a disappointment. Production was affected by weather and cost was higher than expected. We exited 2018 with some overstocking at China ports in anticipation of winter demand and avoid a similar shortage of supply last year. For 2019, we expect production to rebound and selling prices resilient as China is still controlling domestic production.

2. Conglomerate/Utilities: Demand for power in China was better than expected. India still facing spot prices that are too low to incentivise state electricity boards to sign up longer-term PPA. The weak balance sheet of these state boards remains a structural issue. Singapore still faced with excess power and punitive take-or-pay gas supply contracts.

3. Consumer: Despite a recovery in employment for Singapore, consumer spending is still sluggish. Only market share gains and staples registered better-operating performance.

4. Finance: Banks reported strong results and performed well in 1H18. The sector was over-owned and most affected by liquidity flows leaving Asian markets especially after cooling measures for Singapore. As the year progressed, there were fewer catalyst. Weak capital markets slowed wealth management income and loans growth have started to decelerate. Entering 2019, banks are clinging on interest margin expansion as key source of growth. But banks are now paying attractive dividends.

5. Healthcare: No change in the weak fundamentals stemming from loss of share in medical tourism to Malaysia and Thailand plus loss of share to public hospitals.

6. Industrial: Electronic stocks hurt by contraction in volume and lower prices from Apple. 4Q18 will be challenging because the whole supply chain virtually froze or de-risked ahead of Trump-Xi talks in G20 summit. If trade war subsides, we could expect demand to return to the supply chain and the current attract valuations for the sector make them an attractive bet for 2019.

7. Property: Even when take-up rates for new projects were healthy, the share prices for developers were sluggish. 2019 will see a rush for the exits by developers so sell as fast and as much as possible before your neighbour launches.

8. REITs: Sector performance has been resilient in 2018 despite the constant worries of rising interest rates. Ability of many REITs to hedge the interest rates have provided some comfort to investors. 2019 should be a better year as this rate headwind ease off.

9. Shipping – Yard: Just a sector to trade on oil direction. We are still cautious over the fundamentals of this sector. Yard capacity still look excessive and any new jobs aggressively bid up.

10. Telecommunications: The arrival of 4th mobile operator into Singapore telco has been well flagged and incumbents have already responded by lowering prices and sacrificing margins. The MVNOs has already carved out whatever price sensitive profit pool in the market.

11. Transportation: Competition has structurally lessened with departure of Uber and stricter licensing has reduced the supply of drivers of ride-hailing operators. Downtown Line should start to breakeven, as ridership gains traction.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: