I guess QE did work. With interest rates at near zero, Act 1 of QE was to shift investor preference up the liquidity curve into higher yielding and riskier assets. We did get asset reflation in equities, bonds and real estate. The problem was, the wealthy have a lower inclination to spend and would rather store their gains. Corporates preferred the liquidity for share buybacks. And households were de-leveraging post-GFC and in no mood to consume. So despite the surge in liquidity, the use (or velocity) of money globally was at record lows. It took the real economy several years to heal through wealth effect and lower cost of capital.

Act 2 has finally arrived. It is the transmission of this liquidity to stimulate aggregate demand. Global economies are back to a growth mode not seen in five years, according to IMF. To keep this recovery on a self-sustaining path, we need a positive feedback loop of higher sales that spur further employment and capital investment. This then feeds into higher aggregate demand and sales. As corporate profits recover, peppered with the usual dash of executive optimism, we have finally seen a revival in investments. Employment has recovered to multi-year highs but lacking has been wage growth. It has been creeping up but not robust. Higher wages is critical. Money can then be placed in the hands of those with a higher propensity to spend and more liquidity will flow into the real economy. In summary, we expect the rally in global growth to continue in 2018. Wage growth will be the final cog to sustain an above-trend growth, even in the face of rising interest rate.

Strategy: Under such a macro scenario that we construct our playbook for 2018. The sector we favour the most is banks. Banks will be surfing the wave of rising interest rates, recovery in asset quality and higher loan volumes. The concoction could not get any better. Property stocks we believe can perform until at least the 1H18. We still view them as a trade because of high vacancy rates, stretched affordability and fluid demand. We fear these could be roadblocks to any secular story. Our other Overweight is consumer. With wage growth improving (personal wish too), consumers in Singapore should open up their wallets again. This is our laggard Overweight as data has not revealed itself yet.

STI Target: We raise our STI target from 3450 to 3900. This a bottoms-up target, based on a culmination consensus and our target prices. At 3900, PE for STI will be around 17x.

Recommendation: In our absolute return portfolio for 2018, our top 10 picks are: a) Asian PayTV and Ascendas REIT, for those with an appetite for only dividend yield; b) Chip Eng Seng, Dairy Farm, DBS Group, Geo Energy and Micro-Mechanics, for earnings growth; c) ComfortDelGro, Banyan Tree and CapitaLand are our re-rating plays.

The Phillip Absolute 10

2017 REVIEW

2017 kicked off with exuberance over the Trump reflation trade, matched by angst over the EU’s with looming elections and the populist wave. The Trump reflation trade was a head fake. US Treasury yields and US dollar reversed their ascent, and any planned infrastructure stimulus fizzled out. Macron’s overwhelming parliament majority in France ended the debate on EU disintegration. Instead, it rekindled hopes of some fiscal union in the future.

Over in Singapore, the outlook was tepid, at best. Consensus expectations for GDP in 2017 was a sombre 1% – 2%. This was warranted as most indicators were languishing. Loans growth were only growing at 1%, consistent with industrial production paltry 1% climb. And exports moving sideways.

However, as the year progress, it became more evident an economic recovery underway, trending far better than expected. Global economic growth breached several years’ high, accompanied by low inflation. Such conditions ignited the performance of cyclicals, in particular electronics. Another notable event in Singapore was the relaxation of property measures in March. Initial market response was lukewarm, but as the months ploughed on, pent-up demand started to fuel primary and secondary private residential sales. Sales surged to four-year highs and averaging 2300 units per month, up 36% from a year ago.

OUTLOOK

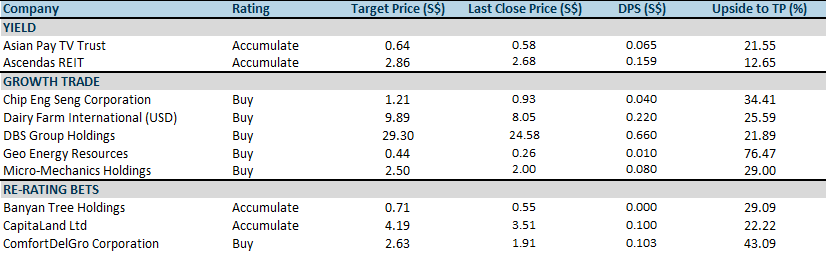

The cyclical uplift for Singapore is well and underway. We are enjoying the best growth rates in five years. For investors, the crucial question is the longevity of this expansion. We used several indicators to give us a peek into the near-term. Singapore new orders PMI suggest economic vibrancy at least till 1Q18 (Figure 1). Another gauge, IFO business expectations, similarly points to sustainable strength in 1Q18 (Figure 2).

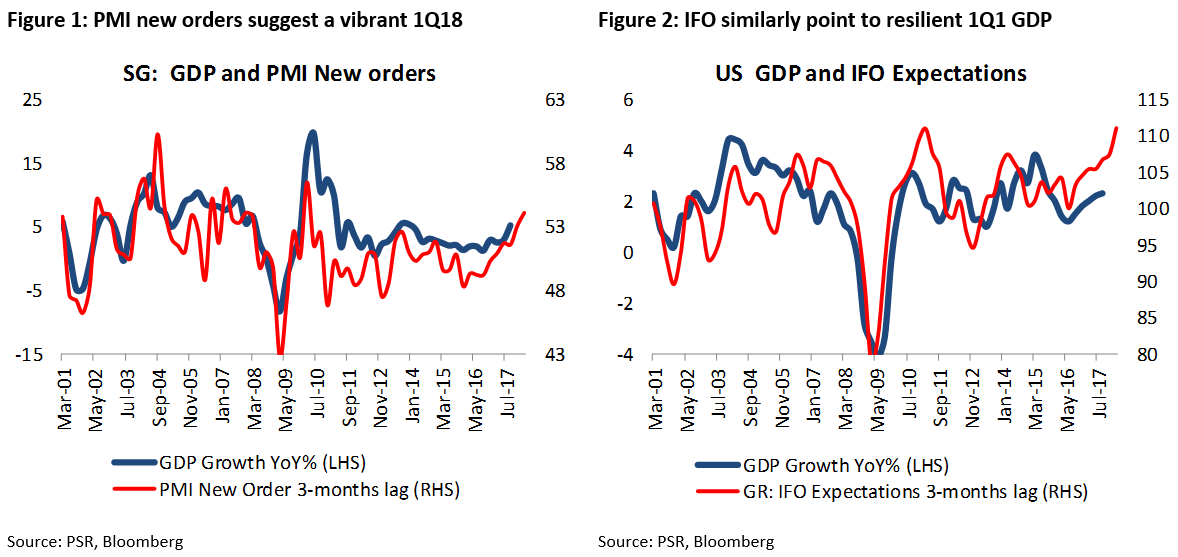

Sustainability, we think, would require a positive feedback loop. Rising sales need to be followed up with employment or wage growth and further capital investment. This will keep an economy on a self-sustaining path. Therefore, two sources of demand need to be trending upwards in 2018, namely wages and capital spending. Capital investment has started its recovery. Employment is at a multi-year high. Only wage growth has been below trend.

Capital Investment: Going by the US proxy, global investment cycle recovered early this year, after drifting for almost three years. We see this in both nominal private fixed investments (Figure 3) and spending on durable goods (Figure 4).

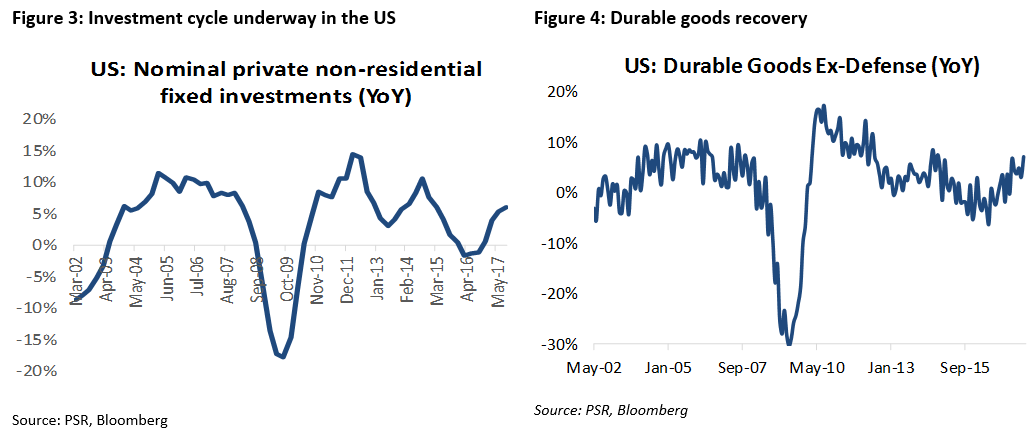

Wages: Wage growth has been sanguine in most parts of the world. As Figure 5 illustrates, US wage growth after GFC has been stuck in a 2% to 2.9% range the past eight years. Singapore’s has averaged 3% p.a. for the past three years. It historically lags GDP by three quarters (Figure 6). We are upbeat, holding the view that wage growth will recover, albeit after a longer lag. We feel there are two secular reasons for the longer lag in wages, notably (i) the build-up of automation in both manufacturing and services sector; (ii) expansion of the global pool of labour with the opening of several developing countries to globalization.

In summary, we expect a continuation of the global growth in 2018. Forward indicators point to at least a healthy 1Q18. For growth to be sustainable, we would need investments and wage improvements. So far, only capital investment has recovered. We believe wage growth will return after a lag. This can bolster growth, even in the face of rising interest rates.

RECOMMENDATION

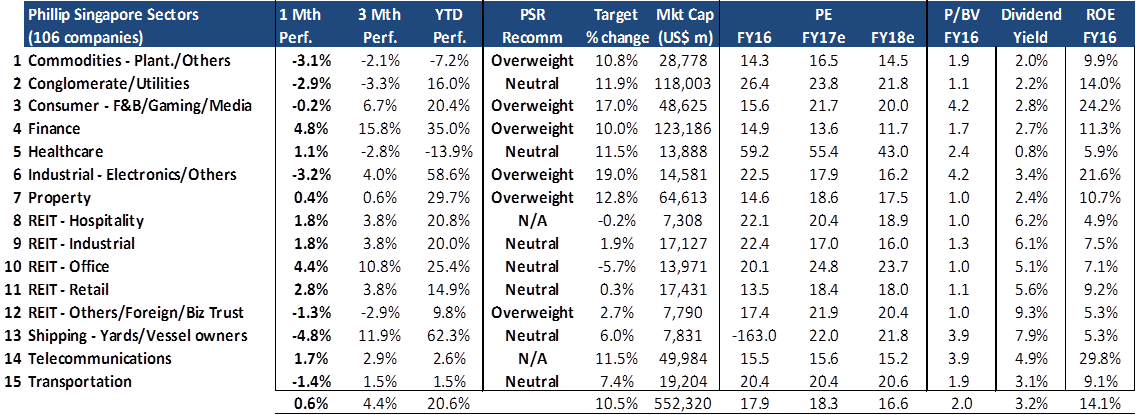

In Singapore, our Overweights are in Commodities (Coal), Consumer, Finance, Industrial (Electronics) and Property. All these sectors are riding on a healthy sales moment. Only consumer is less apparent as any improvement will be lagging.

For 2018 absolute return portfolio, our top 10 picks (The Phillip Absolute 10) are:

Figure 8: Phillip Sector Universe

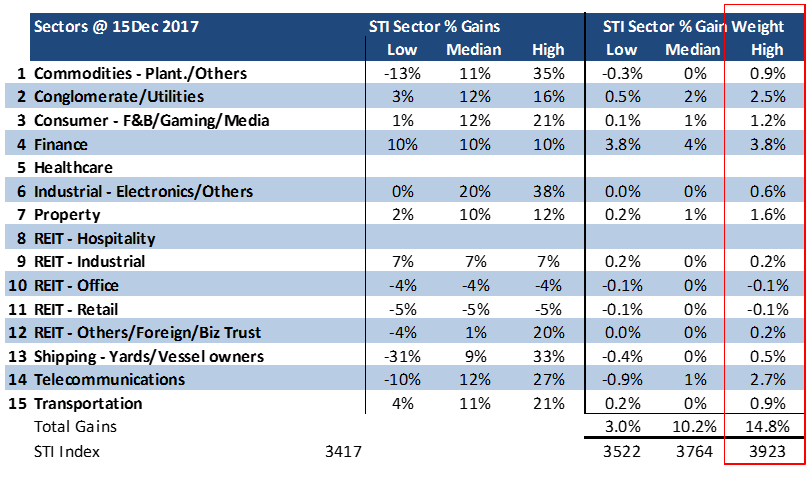

STI target. Our STI target for end 2018 is 3900, an upside of 14%. This a bottoms-up target, based on consensus and our target prices. At 3900, PE for STI will be around 17x. As Figure 9 illustrates, the largest index contributors to STI in 2018 will be finance, telecommunications, conglomerates, and property. In terms of percentage upside, the largest comes from industrial (+38%), commodities (+35%) and shipping (+33%). REITs’ performance is expected to be mixed.

Figure 9: STI range is 3500 to 3900

My Sector Narratives

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.