The Positives

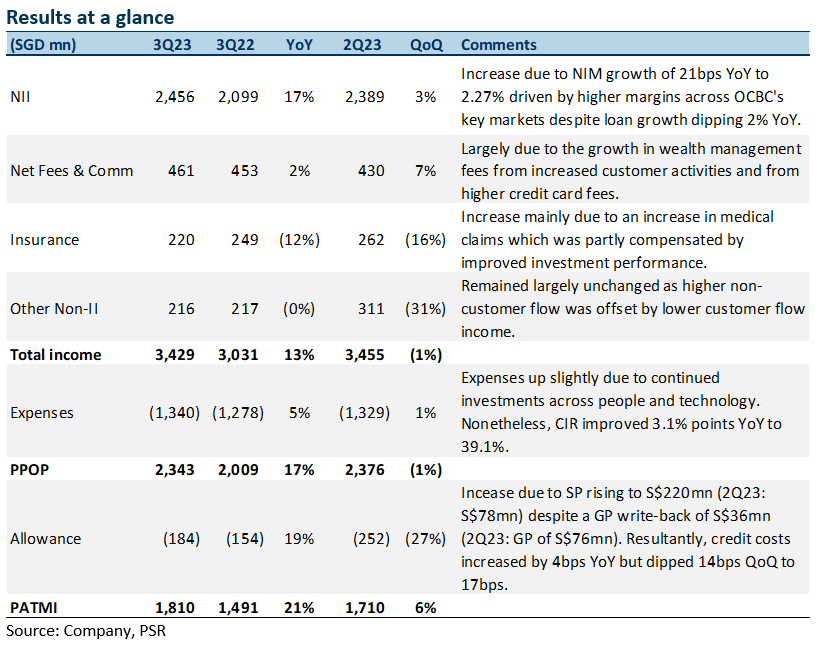

+ Net interest income grew 17% YoY. NII grew 17% YoY led by NIM improvement of 21bps YoY to 2.27% despite loan growth dipping 2% YoY. NIM expansion was mainly driven by higher margins across the Group’s key markets. However, NII only rose 3% QoQ as NIM rose 1bps QoQ as a rise in asset yields more than outpaced the increase in funding costs. Nonetheless, OCBC has increased its NIM guidance for FY23e from above 2.20% to around 2.25%.

+ Fee income grew to highest level in 4 quarters. Fee income rose 2% YoY to reach the highest level in 4 quarters. This was due to the growth in wealth management fees from increased customer activities, and from higher credit card fees. Furthermore, the Group’s wealth management income grew 16% YoY to S$1.12bn and contributed 33% to the Group’s total income in 3Q23. OCBC’s wealth management AUM was 8% higher YoY at S$270bn driven by continued net new money inflows.

The Negatives

– Insurance income down 12% YoY. Insurance income fell 12% YoY from an increase in medical claims, which was partly compensated for by improved investment performance. Nonetheless, total weighted new sales rose 5% YoY to S$419mn, driven by higher sales in Singapore, while new business embedded value (NBEV) was at S$184mn for the quarter.

– Allowances up 19% YoY, credit costs at 17bps. Total allowances rose 19% YoY to S$184mn as SPs grew to S$220mn (2Q23: S$78mn) partially offset by a GP write-back of S$36mn (2Q23: GP of S$76mn). The higher SP was from corporate accounts in various sectors and geographies all over ASEAN, and not to any specific account. OCBC said that it does not see any systemic risk. This drove credit costs up by 4bps YoY to 17bps. Total NPAs were down 16% YoY to S$3.1bn, and the NPL ratio improved by 20bps YoY to 1.0%. Notably, the rest of the world’s NPAs rose 46% YoY to S$585mn, mainly due to the downgrade of one network corporate account in ASEAN in the construction sector.

– CASA ratio continues to dip. The Current Account Savings Accounts (CASA) ratio fell 9.8% points YoY to 46.3% due to the high interest rate environment and a move towards fixed deposits (FD). Nonetheless, total customer deposits increased 5% YoY to S$369bn underpinned by strong growth in FDs. The Group’s funding composition remained stable with customer deposits comprising 80% of total funding.

Outlook

Loan growth: Loan growth declined YoY in 3Q23, falling below the bank’s guidance for FY23e. However, management said that it expects a slower pace of economic growth and has lowered its guidance from low to mid-single to low-single-digit loan growth for FY23e. Management also sees further lending opportunities in the wholesale segment and sustainable financing. Mortgage pipelines in Singapore and Hong Kong are also healthy, with more drawdowns expected in the rest of FY23.

Fee income: With the re-opening of China, OCBC is positive on the broader outlook and expects the re-opening to support China-Southeast Asia trade and investment flows. OCBC has recently launched a private banking unit in Malaysia and mainland China to strengthen its WM services while also hiring for the business. We could expect high single-digit fee income growth for FY23e.

Commercial real estate office sector: Commercial real estate office sector loans are mostly to network customers in key markets with a proven track record and financial strength. Overall LTVs are low at around 50% to 60% and are mostly secured. Overall, the commercial real estate office sector loans make up 13% of the total loan book, with two-thirds of loans to key markets of Singapore, Malaysia, Indonesia, and Greater China. Loans to developed markets including Australia, the United Kingdom, and the United States are largely to network customers with strong sponsors.

Glenn covers the Banking and Finance sector. He has had 3 years of experience as a Credit Analyst in a Bank, where he prepared credit proposals by conducting consistent critical analysis on the business, market, country and financial information. Glenn graduated with a Bachelor of Business Management from the University of Queensland with a double major in International Business and Human Resources.