FY16 was a weaker year for Nam Lee Pressed Metal Industries (Nam Lee), with 21% lower revenue and consequently 29% lower PATMI. Despite the weaker year, gross profit margin was defended at 21.6% (FY15: 22.7%), – which we believe to be due to product mix being maintained. Revenue contribution from the highest margin Aluminium segment was maintained at 83% (FY15: 86%). We note that the twenty largest shareholders now hold 76.71% of the outstanding shares – the highest in the most recent three financial years (FY15: 76.42%; FY14: 76.69%; FY13: 76.75%) – with new institutional interest among them.

What is the news?

We attended Nam Lee’s FY16 Annual General Meeting (AGM) that was held on 26 January 2017. We left with a better understanding of the capital budgeting and capital structure decisions and business plan.

Management shared that the expected capital expenditure (capex) for FY17 is S$15 million to S$20 million. The bulk of the capex is towards setting up its sixth factory in Malaysia, to support HDB projects for steel and aluminium products and a new product line. The use of FY17 capex is for land and construction cost for the new factory in Malaysia (S$10 million) and for new and replacement machinery across the Group (S$5 million to S$7 million).

Management was asked on plans to consolidate the operations in Malaysia, and cited reasons such as country, political and labour concentration risk for not doing so. In addition, certain customers require redundancy in Nam Lee’s production supply chain to ensure uninterrupted delivery of products.

Management shared that the rationale behind the cash hoard (just under half of market capitalisation), is due to the major customer requiring them to have a strong balance sheet, as a condition to contracting Nam Lee.

Shareholders gave two suggestions on returning cash to shareholders – by actively buying back shares and by paying an interim dividend. In theory, the intended outcome of a share buyback programme is to give shareholders an opportunity to exit from their investment, while at the same time increasing the earnings per share (EPS) of the company by reducing the number of outstanding shares. We believe that an aggressive share buyback programme might not be in the best interest of the remaining shareholders in the case of Nam Lee, as it would exacerbate the already low trading liquidity of the stock. A share buyback programme would probably be more effective on a stock with a larger number of outstanding shares and a healthy trading liquidity. We believe that the introduction of an interim dividend would be a shareholder-friendly change, which could lead to better investor interest in the stock.

Management shared on revenue recognition for the year: (1) demand from major customer of speciality aluminium product to be maintained, (2) the Group will be recognising 80% of revenue for a public infrastructure façade project and (3) other ongoing smaller HDB projects will continue to contribute to the Group.

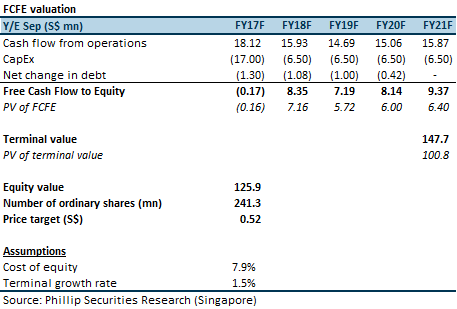

Maintain “Buy” rating with lower DCF-backed target price of S$0.52 (previous: S$0.60)

We have changed our valuation method since our last report and the assumptions are explained overleaf. The current price of S$0.37 gives an implied FY17F dividend yield of 5.4% and our target price gives an FY17F forward P/E multiple of 12.4x and an implied FY17F P/B multiple of 0.93x. Current-asset value per share (current assets minus total liabilities) of S$0.358 should be a floor to the downside, while dividend yield is attractive.

Company Valuation

We are changing our cash flow model from a dividend discount model (DDM) to discounted free cash flow to equity (FCFE) model.

We had previously valued Nam Lee using a DDM, on the assumption that a large proportion of cash on the balance sheet would be paid out as dividends. However, management has stated that the cash would not be paid out excessively, as a strong balance sheet is required in order to be awarded the contract from its major customer.

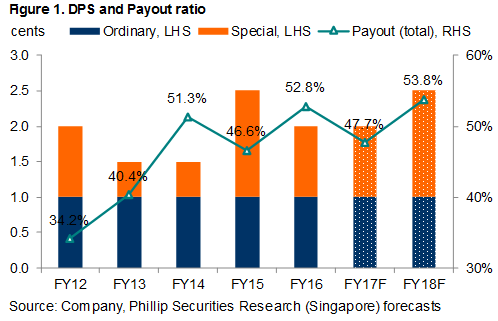

Management stated that its aim is to pay a stable dividend. Nam Lee’s dividend policy is a payout ratio of a third of earnings (inclusive of special dividends). We have adjusted our dividend assumptions downwards, maintaining a payout ratio of about 50% going forward, which is in line with the last three FYs.

Following the downward adjustment to our dividend assumptions, a DDM is no longer suitable to value Nam Lee, as it would not assign any value to the cash that is being retained on the balance sheet. A FCFE valuation would account for all cash that is available to equity holders – both cash that is paid out as dividends and cash that is retained on the balance sheet. We have adjusted our FY17F capex assumption higher to S$17 million (from S$5.5 million previously), following guidance given at the AGM. Our capex assumption from FY18F onwards has been raised to S$6.5 million. We have also added a small-firm premium to our previous cost of equity.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.