The Positives

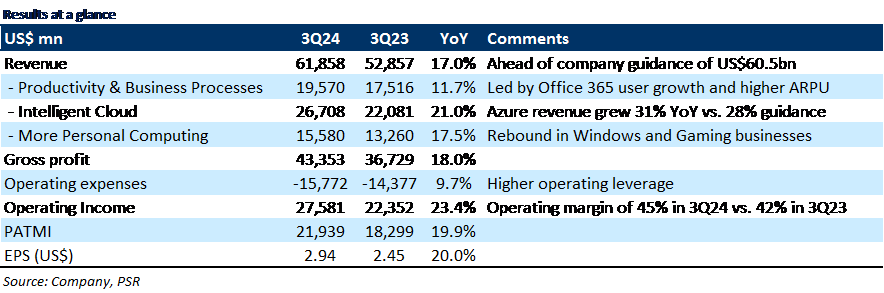

+ Azure revenue growth accelerates. In 3Q24, Intelligent Cloud segment revenue grew 21% YoY to US$26.7bn led by strength in cloud services. Azure revenue grew 31% YoY, beating the company’s guidance of 28% YoY growth. The significant growth was primarily driven by an increase in the size and duration of the deals as customers migrated workloads (e.g., SAP/Oracle) from on-premises to the cloud. Management noted accelerating demand for its Azure AI services, which contributed 7% points to Azure growth (vs. 6% in 2Q24). Azure AI services help enterprises create their own generative AI solutions, including the development of chatbots, summarization, and writing documents.

+ Windows and Gaming continued to rebound. In 3Q24, More Personal Computing segment revenue grew 18% YoY to US$15.6bn, 3% above the top end of company guidance. Notably, Windows OEM revenue grew by 11% YoY, beating the company’s guidance that it would be relatively flat. The growth was mainly driven by a recovery in the PC market and a shift to developed markets. Meanwhile, Gaming segment revenue grew by 51% YoY to US$5.5bn as the integration of Activision Blizzard titles like Call of Duty into Xbox Gamepass drove higher player engagement.

+ Improvement in margins. In 3Q24, the operating margin expanded by 300bps YoY to 45% despite elevated AI-related CAPEX, beating the company’s guidance of 43%. The margin improvement was mainly due to top-line upside, higher operating leverage from prudent headcount control (down 1% YoY), and lower sales-related costs. CAPEX jumped 66% YoY to US$11bn due to cloud and AI infrastructure build-out.

The Negatives

– Nil