Company Background

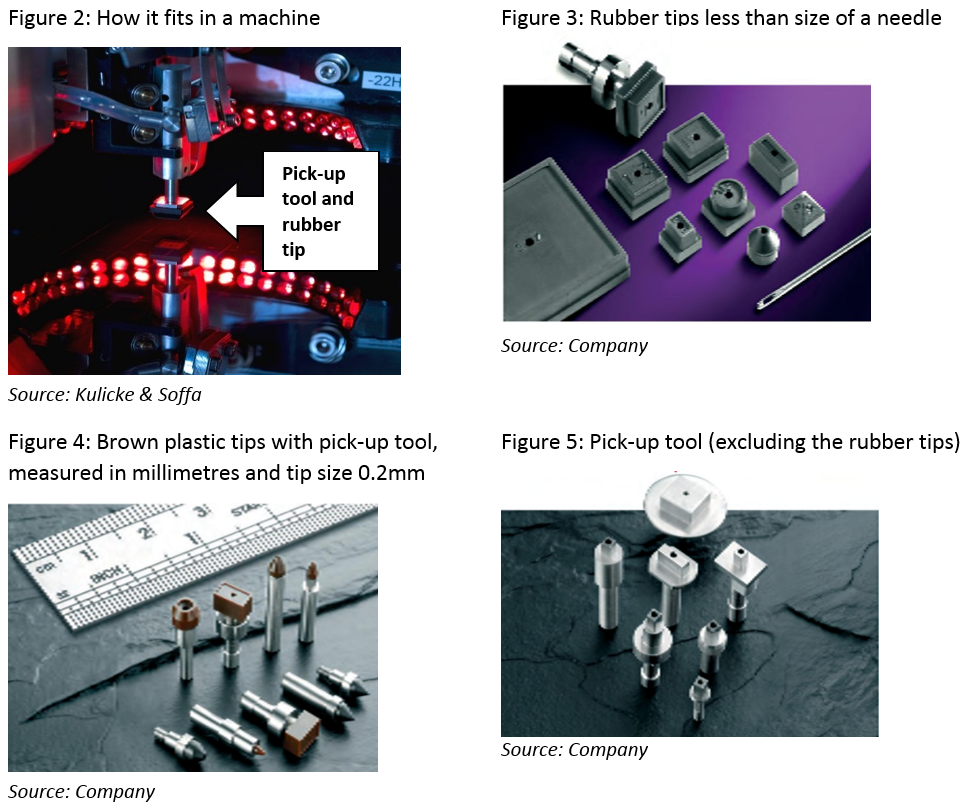

Micro-Mechanics (MMH) produces consumable tools and parts used in the back-end semiconductor process, in particular, die attach and wire bonding. These include rubber tips that pick up tiny bare semiconductors (called dies) that have been cut from a wafer and then placed onto a metal pad (called leadframe that connects to outside world or circuit board). This die will then be encapsulated into the ubiquitous semiconductor chips we see everywhere. Another major product are tools used in the wire-bonding process. An example is a clamp to hold the lead frame during the wire-bonding process of the die. It is also building up capabilities to serve the front-end of the semiconductor industry through its US operations. We do not expect this to contribute materially to earnings in the near term. MMH has a dividend policy of not less than 40% of earnings. Dividend yield is presently at 5.2%

Investment Merits

We initiate MMH with a BUY and a target price of S$2.00, 35% upside including dividends. Our target price pegs MMH at 15x PE FY/18e, which is in-line with peers in the back-end semiconductor supply chain. We believe this is conservative given its superior margins, ROE and dividend yield.

Background

Micro-Mechanics (MMH) was founded by Mr Christopher Borch in 1983. It was listed in June 2003. In its 14 years since listing, revenues have more than tripled and earnings have increased five-fold. During this time, the company has also returned more than S$70m in dividends.

MMH manufactures precision tools and consumable products for the semiconductor industry. Core products manufactured are used in the die attach and wire bond process of the assembly and testing stage. It is also building up capabilities to serve the front-end of the semiconductor industry through its US operations. MMH has five manufacturing facilities in Singapore (1983), Malaysia (1989), Philippines (1998), China (2004) and USA (2008). Also worth mentioning MMH is ranked 19th out of 606 companies on SGX in terms of Singapore Governance and Transparency Index.

*in parenthesis is the year the factories were established.

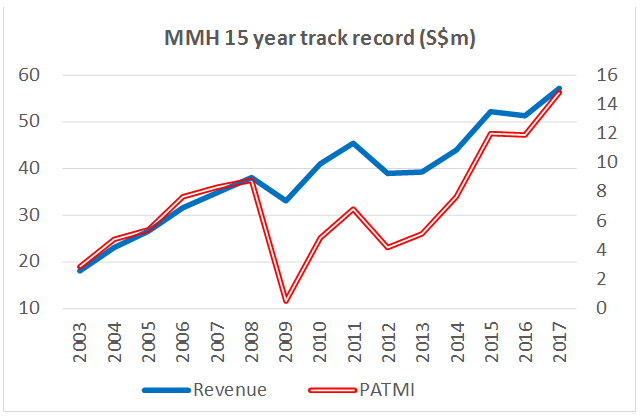

Figure 1: Since GFC impact in 2009, MMH growth has been stellar

Source: Company, PSR

What Micro-Mechanics manufactures?

MMH produces consumable tools and parts used in two steps of the back-end semiconductor process, in particular, die attach and wire bonding (refer to Appendix 1). In addition, MMH has made the strategic step to produce tools and parts for the wafer-fabrication equipment industry from its US factory.

a) Die attach tools (~60% of revenue)*

Refer to Appendix 2 for more details of the die attach process.

b) Wire bonding tools (~25% of revenue)

Refer to Appendix 3 for more details.

c) Precision parts and tools in wafer-fabrication (~15% of revenue)

US operations have been loss-making, but in FY17 the losses have narrowed considerably. MMH embarked on the strategy to penetrate front-end semiconductor industry (and laser, medical, aerospace) following the acquisition of Advanced Machine Programming in May 2008 for S$2.5mn. Since FY09, US operations have been suffering accumulated losses totalling S$12mn. In FY16, MMH redefined its business strategy to focus on manufacturing process-critical parts and tools for the front-end semiconductor industry.

Figure 6: Precision part for front-end equipment

Source: Company

*MMH does not disclose the revenue breakdown by product type. This is based on revenue breakdown last disclosed in FY2006. Similarly, MMH does not disclose the quantity of products sold. Last disclosure was in prospectus FY2002 which was approximately 200k PUTs, 6000 rubber tips, 180k die ejector needles and 9600 wire bond tools.

Competitive advantages

To enjoy manufacturing gross margins of 60% and 40% EBITDA margins, we believe it is due to the tremendous complexity and technology required in producing these tiny little parts which the limit competition. Below are some of the competitive advantages which we believe MMH enjoys:

1. Increased miniaturization: With miniaturization of electronic products and semiconductors, we have seen a dramatic shrinkage of die sizes. Dies sizes are now as small as 1mm2 to 10mm2 depending on the application. Not only is the size of the die shrinking but the thickness of the die is collapsing from 60 microns to less than 20 microns (i.e. 0.02mm).

2. Complex material engineering: The material used in producing the rubber tips require a significant amount of R&D. Materials must avoid electrostatic discharge (ESG) that can burn the semiconductor chip. These materials used must be purified to avoid chemical or organic contamination. The material composition of these tools is proprietary developed by MMH.

3. Need for customization: An interesting “quirk” about MMH tools and consumables is the level of customization. Every customer will require some level of customization for their tools despite some using the same die attach or wire bonding machine. Customers look for fast turnaround times for the tools they require. This customization we believe creates an additional barrier and even exclusivity. Such customization is highly complex due to the quick turnaround time (as short as 6 days). It also means customers prefer to work with a single source or supplier to save cost, in our opinion.

4. High quality and reliability: The quality of the tools requires high precision and consistency due to:

* Micrometre or micron (μm): Width of a single strand of human hair range from 10 to 200 microns.

What we find most attractive about MMH?

1. Huge Margins

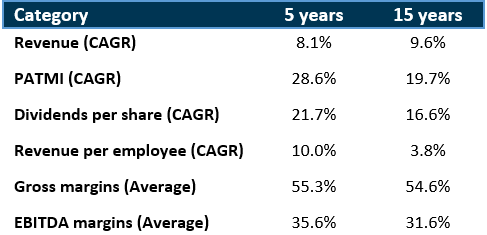

MMH gross margins have averaged 55% over the past five years. The most recent quarter margin expanded to almost 60%. As Figure 8 suggests, MMH has consistently enjoyed high gross margins. Only in the 2009 global financial crises, gross margins suffered and even then, margins bottomed out at 40%.

When we compare MMH margins, against other parts of the back-end eco-system, MMH margins stand as the highest (Figure 13) and is easily double of the industry average. As mentioned earlier, the high margins are a result of the complexity in manufacturing the product, high efficiency (24/7 automated machining), extensive customization and quick turnaround time demanded by customers (as short as 6 days).

2. Long track record of compounding earnings and dividends

When we look at MMH 15-year history, the track record is impressive. Over the past 15 years, revenue has compounded almost 10% per year. Profits have performed even better, compounding at 20%. It seems that MMH’s growth is accelerating. The 5-year track record for earnings is now 28% CAGR. MMH has a dividend policy of not less than 40% of earnings.

Figure 8: Enviable track record of earnings and dividends

Source: Company, PSR

3. Healthy Balance Sheet

MMH has no leverage on its balance sheet. The company is in a net cash position of $22m. In its 15 years track record, MMH has always been in net cash position due to the positive cash-flow generated every year. Despite its large cash holdings, MMH posted unlevered ROE of 28% in FY17.

4. Consumable nature of produt

Another strength of MMH products is the consumable feature of the tools. In general, some of the tools, in particular higher-end semiconductors, need to be replaced every 8-hour shift by the customer. This is to contain contamination and ensure precision of the process. This means the demand for the product is more recurrent and depend on the output of semiconductor rather than on lumpy capital expenditure cycles.

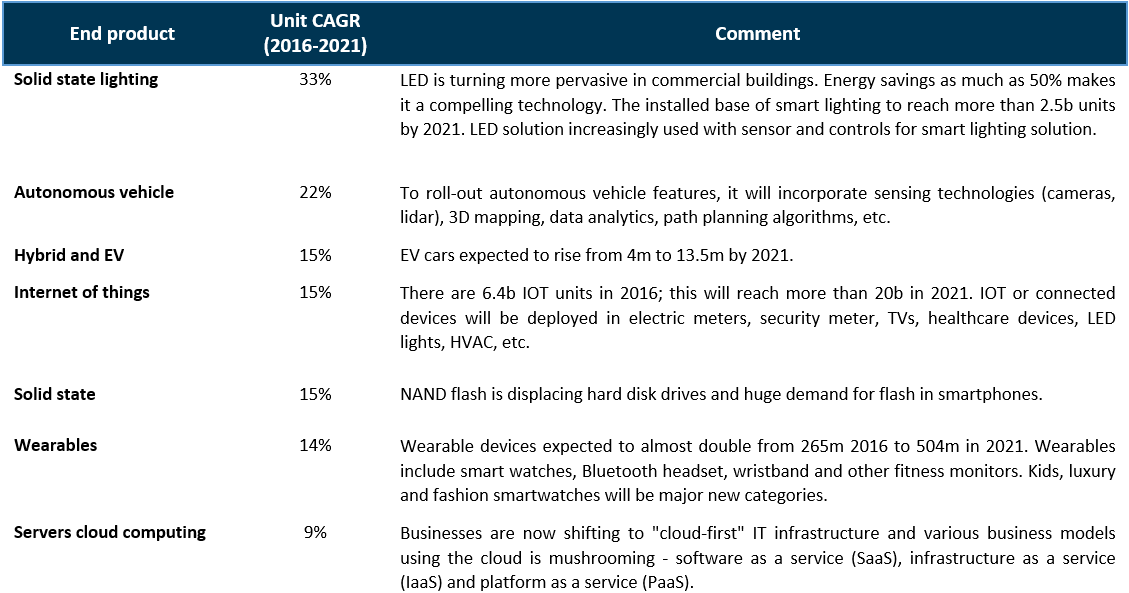

5. Huge growth opportunity ahead

The key driver for MMH growth will be increased sophistication of packages and unit growth of semiconductors. It is hard to compute the exact impact of advanced chip packages on demand. But we can use semiconductor unit growth to have a good gauge for demand, especially due to the consumable nature of MMH products. Demand for semiconductors is expected to grow 9% per year on a per unit basis from 2016 till 2021, according to Gartner. The various drivers to unit growth are represented in Figure 9.

Figure 9: Multiple drivers of semiconductor unit growth

Source: Kulicke & Soffa, Gartner, PSR

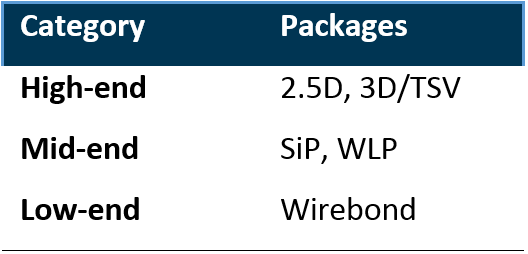

6. Advanced packages still require die attach process

As semiconductor packages evolve, the requirement for the pick and placing of dies becomes ever more critical.

Figure 10: Simple summary of packaging categories

Source: PSR, media

7. Wide customer base and low concentration risk

MMH has more than 600 active clients. Customers are basically from three broad categories:

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.