The Positives

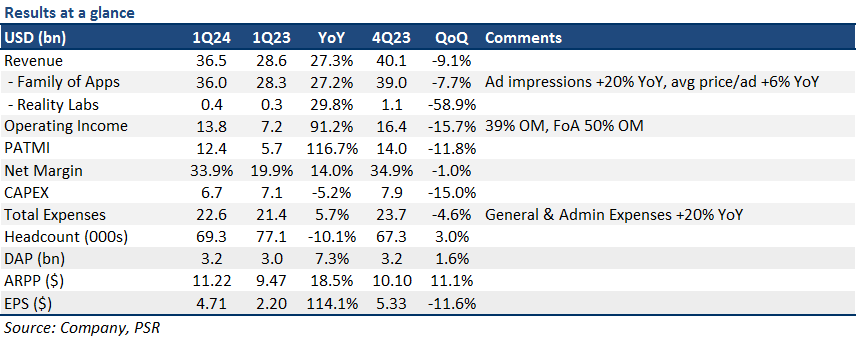

+ AI content driving greater engagement, leading to higher ad revenue. META continues to leverage its AI capabilities to improve engagement on its apps, indirectly leading to higher ad revenue (+27% YoY). META’s AI recommendation system now contributes roughly half of all content users see on Instagram, driving more value for advertisers. The demand-supply dynamics of digital ads are also improving, with META seeing healthy 20+% YoY growth in impressions and a 2nd consecutive quarter of YoY advertising price increases. E-commerce companies remained the largest contributor to advertising revenue growth.

+ Positive momentum for Video/Reels. Video engagement continues to be a bright spot for META, contributing to >60% of viewing time on both FB and IG. Reels remain the key driver for this growth, with its strong ramp throughout FY23. Reels monetisation is also improving with META leveraging AI for more optimised ad loads and placements.

The Negatives

– Higher CAPEX spending moving forward. META is doubling down on scaling its AI capabilities to develop more advanced and compute-intensive models while also scaling its training and inferencing needs (custom silicon). As a result, FY24e CAPEX guidance was raised by ~US$4bn to a range of US$35bn-US$40bn. It expects this investment cycle to take at least 2 years to complete.

– Decelerating revenue growth for 2Q24e. META guided to 2Q24e revenue growth of ~18% YoY, implying a deceleration in growth as it: 1) laps a period of tougher comparisons due to China recovery from early-FY23, 2) slower increase in Reels’ advertising load after an initial aggressive ramp, 3) ~1% YoY impact from a strengthening USD.

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.