KEY HIGHLIGHTS

Company Background

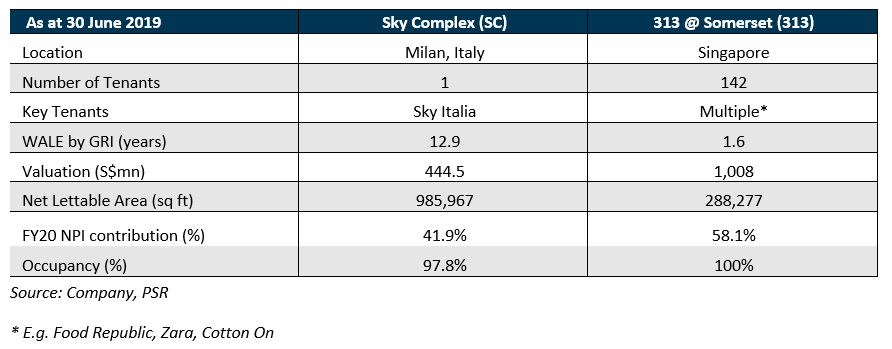

Lendlease Global Commercial REIT (LREIT) primarily invests in stabilised income-producing real-estate assets globally, for retail and/or office purposes. Its portfolio comprises a leasehold interest in 313@Somerset (313), a retail mall in the heart of Singapore, and a freehold interest in Sky Complex (SC), a Grade A office asset in Milan. Its portfolio has an appraised value of S$1.4bn. On 1 October 2020, LREIT acquired an effective 3.75% stake in Jem for S$45mn, a shopping mall in Jurong, Singapore.

Investment Highlights

We initiate coverage with an ACCUMULATE. Our DDM TP is S$0.78, implying 14.2% upside potential, inclusive of FY21e dividend yields of 6.1%.

THE REIT

LREIT was listed on 2 October 2019 on the main board of SGX at S$0.88 per share. Its Manager is Lendlease Global Commercial Trust Management Pte. Ltd., an indirect wholly-owned subsidiary of its sponsor. In May and June 2020, LREIT was included in the MSCI Singapore Index and GPR APREA Investable REIT 100 Index.

THE SPONSOR: LENDLEASE CORPORATION LIMITED

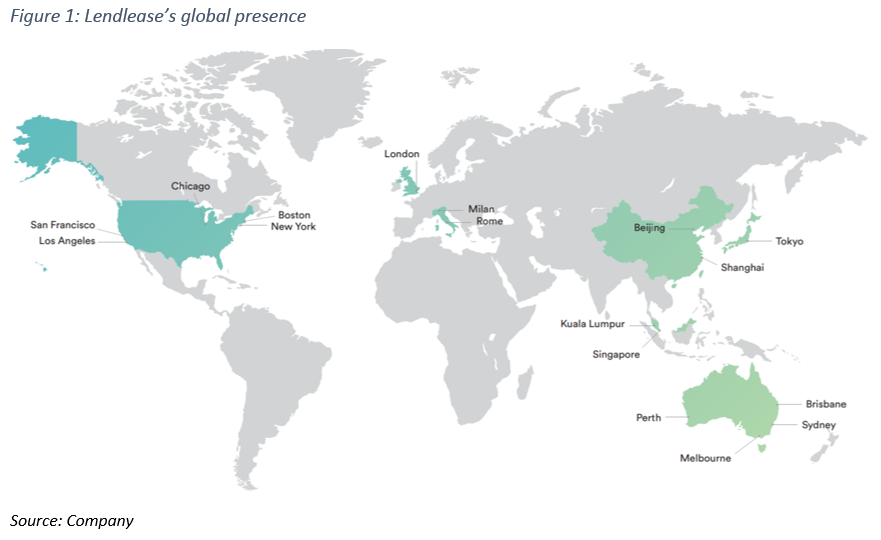

Lendlease Corporation Limited (LLC AU, Not Rated) is part of the Lendlease Group (LGroup), a leading international property and infrastructure group listed on the Australian Securities Exchange. Lendlease Group is one of the largest developers in the world, with a global development pipeline value approaching A$113bn. It operates in 17 gateway cities:

• Asia: Singapore, Sydney, Brisbane, Melbourne, Perth, Beijing, Shanghai, Tokyo and Kuala Lumpur

• Europe: London, Milan and Rome

• United States: New York, Boston, Chicago, San Francisco and Los Angeles

Lendlease Group (LGroup) has delivered projects globally for 60 years. To date, it has 21 urbanisation projects. These include Paya Lebar Quarter (Singapore), Melbourne Quarter (Melbourne, Australia, Fig. 2), The Exchange TRX (Kuala Lumpur, Malaysia) and Milano Santa Giulia (Milan, Italy). The Group’s core construction business had backlog revenue of A$14bn globally as at FY20. It also managed 14 wholesale funds with more than A$36bn for about 150 institutional investors.

THE ASSETS

LREIT holds two properties in its portfolio and an indirect 3.75% interest in Jem.

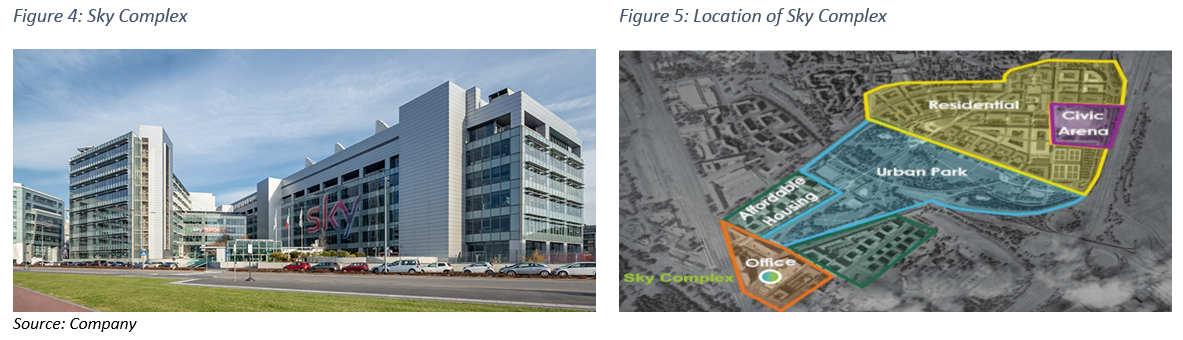

a. Sky Complex: stable income generator. Strategically located in one of Milan’s newest and most vibrant office precincts in the Milano Santa Giulia area, this property consists of three Grade-A office buildings wholly anchored by Sky Italia. Sky Italia is owned by ComCast Corporation, the world’s largest broadcasting company by revenue (Forbes, 2020). Milano Santa Giulia is a strategic area due to its connection to the historical centre of Milan and easy access to all transportation modes. The latter include the Tangenziale Est Milan Ring Road, a high-speed railway station, and Linate Airport. The strategic location and high-quality office buildings in Milan’s peripheral office submarket have led to its highest take-up rates in the Milan office market in the past three years.

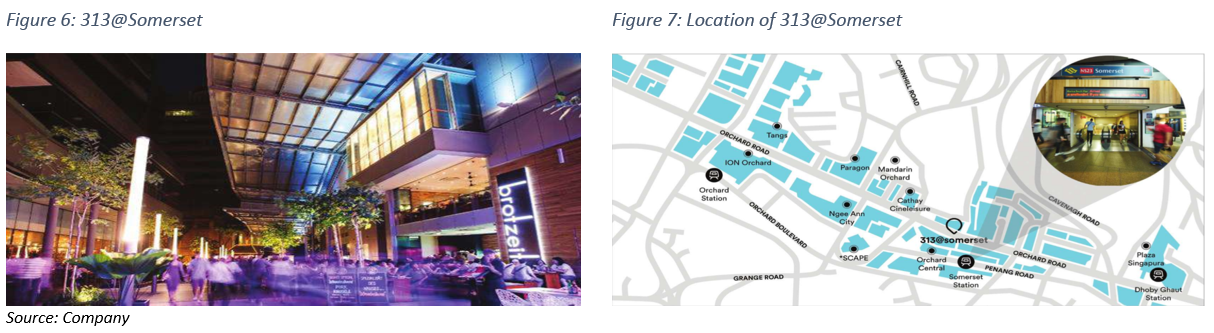

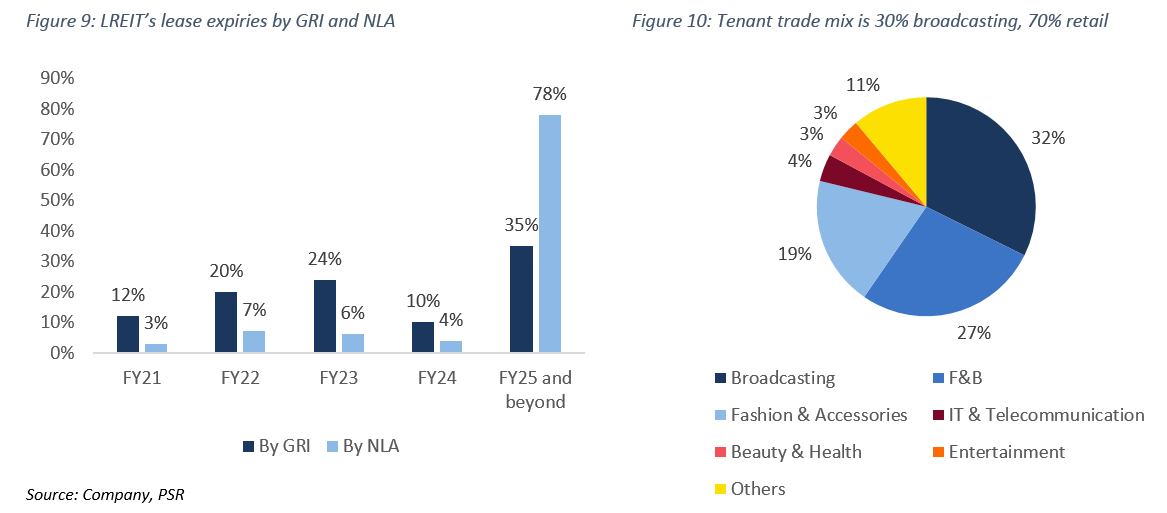

b. 313@Somerset: a differentiated lifestyle destination mall. 313@Somerset offers 288,277 sqft of prime retail NLA along the main Orchard Road belt, Singapore’s most famous shopping and tourist precinct. It is situated smack in the middle of Orchard Road with direct access to the Somerset MRT Station. 313’s tenants include leading global brands such as Zara, Forever 21 and Cotton On and dining establishments such as Hai Di Lao, Brotzeit and Marché. Over the past three years, annual footfalls averaged 45.5mn, about 8x Singapore’s population.

INVESTMENT MERITS

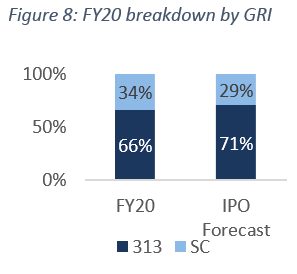

1. Highly stable portfolio built for growth. Portfolio committed occupancy is 99%. We see income stability for SC, which contributes 33.7% (Fig. 8) to FY20 gross rental income. This is because SC has been 100% leased to Sky Italia in a triple net lease structure. Its WALE is long at 12.1 years, with a lease break option only in 2026. It has an annual step-up feature which is based on 75% ISTAT consumer price index variation. The remaining 66.3% of the portfolio’s income comes from 313, with a WALE of 1.8 years by GRI. About 60% of 313’s leases are built with annual rental escalations of 2.7%.

SC has been resilient throughout Covid-19. To date, Sky Italia has paid up all its rents in a timely manner. Over at 313, struggling tenants with leases expiring in 1Q21 had been offered short-term extensions of 6-12 months or 3-year leases with lower base rents and higher turnover rents in the first year. As recovering tenant sales and footfalls are expected to return confidence to tenants, we expect upcoming leases to be renewed with a higher fixed rent component. Historically, gross turnover rent accounts for less than 5% of LREIT’s gross revenue. We are expecting fixed rents to contribute more than 90% to portfolio GRI in FY22.

Minimal drag on FY21 anticipated. As of date, most of 313 had reopened, except for one KTV which will reopen soon. Tenant sales and footfall had recovered to 70% and 60% of pre-Covid levels. Separately, LREIT has flushed out all the rental rebates to be given to tenants by the end of FY20 (30 June 2020). Hence, we are not expecting any residual abatements in FY21. Although six tenants had applied for rent deferral under Singapore’s Covid-19 temporary measures, none has exercised this. That said, we still expect FY21 revenue and NPI to underperform its IPO forecasts by 3% and 7.5% respectively, due to the short-term leases provided in 1Q21. We are expecting arrears to rise 20-30% as some tenants temporarily cancelled GIRO payments while waiting for government rebates.

313 to bottom out with the help of Phase 3. As Singapore moves towards Phase 3 reopening, more activities are expected to resume. An increase in the group size for gatherings and capacity as well as reopening of higher-risk bar, pub, karaoke and night-club outlets should bring back more get-togethers and consequently, consumption. As F&B tenants contribute 37.7% to 313’s GRI, we believe that further relaxation of Covid-19 measures will return footfalls to about 80% of pre-Covid levels. Tenant sales are expected to recover to 85% of pre-Covid levels. In addition, the air travel bubble announced by the Singapore and Hong Kong authorities in October, albeit delayed, could be a step towards the reopening of borders.

2. Organic growth for 313 with redevelopments

313’s lifestyle youth hub to appeal to New-Age tenants. 313 sits above the Somerset MRT station. This is an enviable location along Orchard Road, as it is smack in the heart of the shopping belt. With its proximity to public transportation, 313 is an optimal location for omnichannel players to locate their physical stores. Love, Bonito, Singapore’s largest local fashion brand, chose 313 as the venue for its first physical store in Singapore. Further bridging the online to offline trend, 313 also attracted Pomelo, which opened its first store in Singapore in 2019. In our view, 313 is a gem that remains attractive to new-to-market online brands due to its strategic location in a prime leisure spot and ability to provide myriad experiences and services to similar target audiences. We are fairly certain that this differentiation of 313 as a ‘lifestyle x new-age mall’ will be able to draw more footfall and sales. Not resting on this laurel, LREIT is exploring partnerships with brands and education providers to monetise its atrium space.

Rejuvenating Orchard Road via Grange Road carpark redevelopment. On 13 June 2020, LREIT won a joint tender to redevelop the 48,200 sqft carpark at Grange Road into a new multi-functional event space. This redevelopment is part of the STB-URA-NParks-LTA’s blueprint to rejuvenate Orchard Road. Somerset has been designated to continue providing lifestyle offerings to youths. Set to be operational in the first half of 2022, the concept offers a first-of-its-kind lifestyle experience along Orchard Road. It will have multiple dedicated event spaces, an independent cinema, hawker stalls serving local delights and a food and beverage attraction. LREIT is collaborating with Live Nation, the world’s leading live entertainment company, on this project. Other partners include The Projector and Museum of Food. With the inclusion of the Grange Road event space, 313’s net lettable area will expand by 14% to 330,000 sq ft.

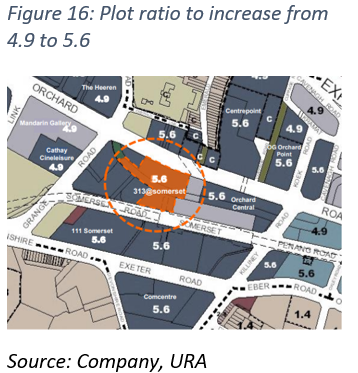

Development cost is S$10mn or less than 1% of LREIT’s deposited property value. This will be funded by LREIT’s working capital, spread throughout the development phase. We are expecting the development to be yield-accretive at a conservative return of investment of 10% p.a. (FY22 DPU accretion: 1%). There are future upside opportunities if we consider joint marketing and cost synergies with 313 (Fig. 16).

AEI to increase plot ratio for 313. The URA granted 313 an increase in plot ratio under its Master Plan 2019, from 4.9+ to 5.6, resulting in a potential increase of up to 1,008 sqm of space. LREIT has identified areas of expansion. However, in light of current economic conditions, major work has been temporarily shelved. We are looking at a possible delay till FY22 before the AEI contributes to valuation.

3. Inorganic growth opportunities; the only REIT under sponsor. Keeping its global and broad-based investment mandate, LREIT will be the only investment vehicle that the Lendlease Group will have. LREIT has ROFR agreements with Lendlease Trust and Lendlease Corporation which covers any proposed offer or private funds managed by Lendlease Group, if it is to dispose any interest in any stabilized assets globally, used for office and/or retail purposes.

For the asset to be considered stabilized, there are a few criteria: 1) the asset must be generating rentals at market rates; 2) it must be operating at a minimum occupancy of 80%; 3) there should be no major AEI planned for the next two years so that the property is readily generating income for investors. Within the A$36bn FUM of the sponsor, we are estimating up to c.A$32.4bn worth of stabilized assets that may present future acquisition opportunities for LREIT.

Assets in the pipeline closer to home include Paya Lebar Quarter (PLQ, 30% interest), Parkway Parade (PP, 10% interest) and Jem, where LREIT recently acquired a 3.75% stake in. PLQ recently opened in 3Q19, hence it may be too early to conclude that the property is generating a stable income stream. While PP has been operational since 2012, it is not ideal due to its near-term need for AEIs and the nearby construction of Marine Parade MRT due for completion in 2023.

LREIT’s near-term priority is to add to its stake in Jem. Jem is an integrated office and retail development in Jurong Gateway, the commercial hub of the Jurong Lake District. It is one of the largest suburban malls in Singapore with retail space on six levels. Anchor tenants like NTUC FairPrice and IKEA occupy 30% of the mall. It also comprises 12 levels of office space which have been 100% leased to the Ministry of National Development for the next 30 years. It is a stabilised asset with high fixed recurring income.

On 1 October 2020, LREIT acquired 5.0% of Lendlease Asian Retail Investment Fund 3 (ARIF3), which holds a 75.0% indirect interest in Jem. This brings LREIT’s effective stake in JEM to 3.75%. The S$45mn cost is fully debt-funded. Return of investment is c.2%. The Lendlease Group still holds a 15.1% stake in ARIF3. The 3.75% stake in Jem is expected to add to 2% to FY21’s DPU.

Other probable markets to be evaluated include Australia, where LREIT’s sponsor has a significant presence. LREIT is also open to looking at third-party transactions in Europe. With pro-forma gearing of 36.9% post-acquisition and low cost of debt of 0.86% p.a., we see room for LREIT to pursue more acquisition opportunities.

VALUATION

We initiate coverage with an ACCUMULATE rating and DDM-derived target price of S$0.78. With prospective dividend yields of 6.1%, total potential upside is 14.2%. Our target price is based on 4-year projections and assumes cost of equity of 8% and a terminal growth rate of 2%.

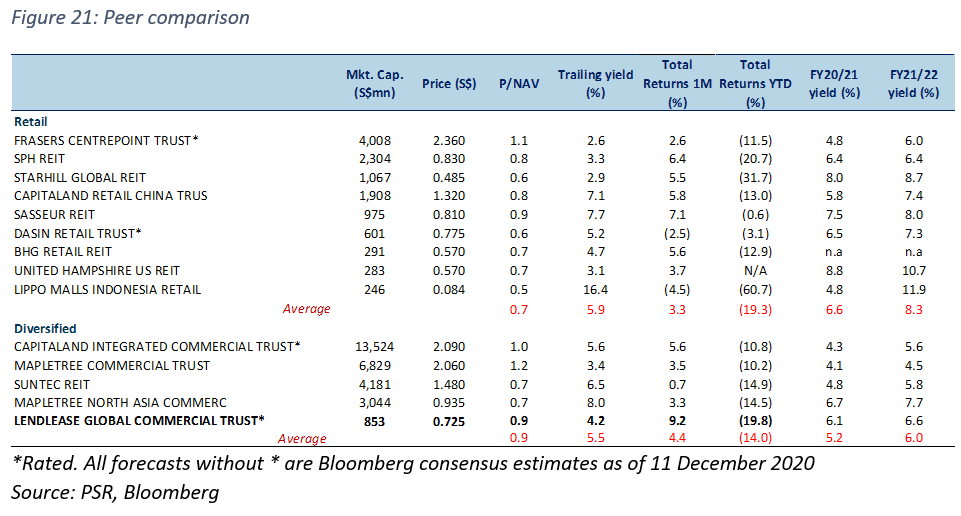

LREIT is trading at 0.86x P/B, which is above pure retail REITs’ 0.74x but below diversified retail REITs’ 0.90x. LREIT’s FY21e/FY22e dividend yields of 6.1%/6.6% also outperform the average forward yields of diversified retail REITs’ 5.2%/6.0%. We believe valuations are still attractive, with Phase 3 reopening and potential developments providing near-term catalysts.

RISK FACTORS

1. Small portfolio; subdued retail outlook. LREIT’s main portfolio comprise only two properties currently. About 58.1% of its FY20 NPI was reliant on Singapore’s prime retail market. Due to general economic weakness, retail leasing is expected to be subdued. Given that there are several malls in the Orchard Road belt (Ion Orchard, Orchard Central), 313 faces competition in retaining and attracting quality tenants. We conservatively estimate rental reversions of -10%/5%/10% for leases expiring in FY21e (25% of the GRI)/FY22e/FY23e. We assume that the 3% annual rent escalation remains constant for the next three years.

2. Limited growth prospects for SC in near term. Due to slower global economic growth, we are expecting limited growth in SC’s rental escalations. Its annual step-up feature is based on 75% ISTAT consumer price index variation. In our models, annual rental escalations estimated for the leases at SC in FY21e/FY22e/FY23e are 0%/0%/3%.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: