Positives

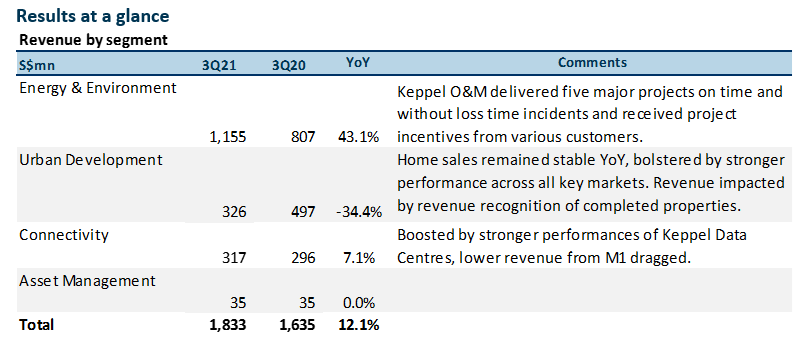

+ Significant improvement in 9M21 profit with revenue in-line. In its 9M21 voluntary business update, Keppel reported improvements in its profits driven by improved performance in all its segments. The net profit was not provided in this voluntary business update.

Energy & Environment: Keppel O&M was profitable for 9M21, reversing the net loss from last year. Keppel O&M also achieved overheads reduction of over S$90mn in YTD 2021 and will continue to streamline its operations. With the recent rise in oil prices, management is seeing signs of improvement in the jackup rig market. Utilisation rates are improving and Keppel O&M has been receiving more enquiries on bareboat charters for its rig assets, though the sale of rig assets may take longer to materialise. The O&M net orderbook was S$5.5bn, up 67% from S$3.3bn at end-2020.

Urban Development: Keppel Land’s total home sales was stable at 810 in 3Q21 vs. 800 for the same period last year. 3Q21 revenue was softer due mainly to the impact of revenue recognition of completed properties during the period.

Connectivity: 3Q21 revenue growth driven by strength in data centres. Despite the drag of lower roaming and prepaid revenue on M1’s top-line, earnings for the quarter was higher YoY from the growing enterprise business.

+ On track to hit higher bound of S$3-5bn divestment target. Keppel has announced monetisation of over S$2.3bn in assets from October 2020 to July 2021 (Figure 2), and have completed about half of the transaction. The transaction between M1 and Keppel DC REIT is subjected to approvals and are expected to be completed by end of 2021. M1 is not expected to recognise any gains from this transaction and we expect the capital to be used to help M1 invest in new capabilities and also fund other growth initiatives like the Bifrost Cable System.

We believe Keppel is expected to surpass S$3bn in asset monetisation well ahead of its three-year schedule. Keppel is likely to exceed the S$3-5bn target by the end of 2023 that is set in its Vision 2030 plans. We believe Keppel will use the capital unlocked to invest in organic and inorganic growth plans and distribute some of the proceeds to reward shareholders.

+ No provisions to be set aside for lawsuit from EIG Global Energy Partners. The lawsuit brought against Keppel O&M was first served in February 2018. EIG Global Energy Partners is a leading provider of institutional capital to the energy sector globally. The court has, in May 2020, amongst other orders, dismissed part of the plaintiffs’ claims in that lawsuit. The management is of the view that there are many disputed facts concerning the plaintiffs’ claim for aiding and abetting fraud. On that basis, Keppel O&M’s US counsel is of the opinion that overall, Keppel O&M has very good defences to the plaintiffs’ claim. As such, Keppel will not be setting aside any provisions for the lawsuit.

Negatives

– Rival offer for SPH from Temasek-backed consortium. With a new rival bid from a Temasek-backed consortium, Keppel may have to raise their offer bid for SPH. The consortium comprising Hotel Properties Ltd (HPL), businessman Ong Beng Seng, and two Temasek-linked entities, CLA and Mapletree, are proposing to acquire SPH at $2.10 per share in cash. The consortium vehicle, Cuscaden Peak, is 40% held by a HPL unit called Tiga Stars, 30% by Temasek unit CLA Real Estate Holdings and 30% by the Mapletree group. Property group Mapletree is also a Temasek-linked entity.

The offer price of $2.10 per share is slightly higher than what has been offered by Keppel. Recall that Keppel had in August offered to privatise SPH at S$2.099 per share. This offer comprises cash of $0.668 per share, 0.596 Keppel Reit unit (valued at $0.715) and 0.782 SPH Reit unit (valued at $0.716) per share.

Pursuant to the terms of the implementation agreement, Keppel has the opportunity, within ten business days, to improve their current proposal and we expect an announcement soon.

Possible scenarios

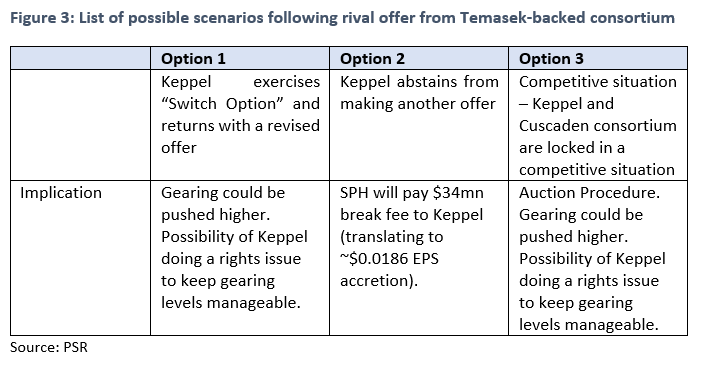

With a new rival offer for SPH, we list down the list of possible scenarios that Keppel may undertake in response to the new competitive bid.

Option 1: Keppel exercises “Switch Option” and returns with a revised offer. Under the Switch Option, Keppel will make the offer on the same or better terms as those which apply to the Scheme. We believe Keppel is well-positioned to enhance and unlock the value of SPH’s portfolio as the two companies are already partners in businesses such as M1, Prime US REIT (PRIME SP, TP: US$0.94) and the development of the data centre at Genting Lane in Singapore. We believe Keppel could return with another offer to reap the synergies from the acquisition.

In such a scenario, we believe the gearing could be pushed higher. Keppel had a net gearing of 0.76x as at end-Sept 21, we believe Keppel could propose another offer while keeping net gearing at ~1x. We see the possibility of Keppel doing a rights issue in order to keep gearing levels manageable.

Option 2: Keppel abstains from making another offer. It walks away from the deal and takes the $34mn break fee, which translates to about 1.86 Singapore cents earnings per share accretion.

Option 3: Competitive situation in the absence of any agreement between the parties as to any alternative procedure for resolving this competitive situation. The Auction Procedure, provided for by the Securities Industry Council will apply, in order to provide an orderly framework for its resolution.

Mechanism – In an Auction Procedure, either or both offerors may announce a revised offer on the Auction start date. An offeror shall then be able to announce a revised offer on the next day, provided that the offeror has announced a revised offer on the Auction start date. The only manner in which either offeror may revise its offer is by unconditionally increasing the cash consideration payable under its offer by a fixed amount of at least S$0.01. The process described above shall continue, on sequential days unless and until, on any given day, neither offeror announces a revised offer, in which case the Auction Procedure shall end at 6 pm on the day in question.

Outlook

Keppel previously announced they have received bids for its logistics business, which are currently being evaluated. We expect that a binding offer could take place before the end of the year.

Keppel O&M and Sembmarine (SMM SP, Non-rated) are in preliminary discussions on a potential combination. The timeline for the parties to reach an agreement has been extended to the 1Q22 from 4Q21. While nothing has been firmed up, we view the discussions positively as it provides better clarity on the fate of its O&M unit. With the overhang removed, along with the planned divestment of its logistics unit, we believe Keppel will be re-rated.

The proposed transactions are expected to be earnings-accretive for Keppel in the current financial year on a pro-forma basis, although there is no guarantee of completion by this year. The group’s net debt should fall as a result of the deconsolidation of Keppel O&M and receipt of part of the consideration from the merged entity. Distribution in specie of the merged entity will, however, reduce Keppel’s shareholders’ funds. Overall, net gearing is not expected to be much affected by the transactions.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Terence specialises in the consumer, conglomerate and industrials sector. He has over five years of experience as an analyst in the buy- and sell-side. As an institutional fund management analyst, he sat on the China-Hong Kong desk. Terence was ranked top 3 for Best Analyst under the small caps and energy category in the Asia Money poll 2018.

He graduated from the Singapore Management University with a major in Finance (Honours), and is the honoured recipient of the CFA scholarship.