Positives

+ Keppel O&M will be restructured into three units (Op co, Rig Co and Dev Co), with two transient entities created to hold their legacy completed and uncompleted rigs valued at S$2.9bn. The path to the divestment of these transient entities (Rig Co and Dev Co) – the offshore rig building business has become clearer. Management expects cost savings of S$90mn in FY21e from the O&M restructuring through right-sizing of the workforce.

+ Keppel remain on track to unlock value from S$3 – 5bn of assets, and have already announced S$1.2bn of assets since October last year, they remain well on-track to reach their target. We expect this to come in at the upper bound of the range and have pencilled this in our FY21 – FY22e forecasts.

+ Strategic review of logistics business completed with Keppel T&T looking to fully divest or maintain a minority stake in their loss-making logistics unit. Despite benefiting from rising demand for e-commerce accelerated by COVID-19 pandemic, the Group has decided to exit the business to focus on other units.

Negatives

– We think the market will be disappointed by the absence of a clear and immediate exit plan from the O&M business while retaining their higher value added renewable energy division. We are cognisant however that an immediate exit might not be feasible given the challenging landscape, with the restructuring, we note that a merger/full divestment remains a possibility.

Outlook

We expect Keppel to speed up the divestment of non-core assets tracking the S$3 – 5bn target in three years. Keppel has identified S$17.5bn of assets to be monetised over time, specifically S$3 – 5bn within three years. They have already divested S$1.2bn of assets, realising an estimated gain of S$120mn. We see the successful divestment of Rigco as a potential catalyst for the Company.

Restructuring Keppel O&M

Keppel’s O&M unit will be restructured into three units (Op co, Rig co and Dev co). Operating company (“Op co”), less the legacy rig assets, will be transformed into an agile, asset-light Op co focused on developing and integrating offshore energy and infrastructure assets. It will focus on higher value-adding design, engineering and procurement, with fabrication subcontracted to third parties. Rig co is focused on putting completed rigs to work or selling them. Rig co will sell the rigs through a merger or spin-off. Development company (“Dev co”) is focused on completing rigs under construction, prioritising projects with firm contracts. Completed rigs will be delivered to customers or transferred to Rig co.

With the latest restructuring, Keppel’s Op co will be unencumbered by the historical legacy rig assets and can focus on opportunities in floating infrastructure and collaborate with other Keppel business units to provide solutions for sustainable urbanisation, such as data centre parks. The new Op co will be focused on higher value-adding work as developer and integrator. It is expected to be self-financing and profitable over time. Management has guided for cost savings of S$90mn in FY21e from the O&M restructuring.

Rig co, which will hold Keppel O&M’s completed rigs will be put to work or sold if the opportunities arise. The rigs expected to be injected into Rig co include the five jack-up rigs from Decon, TS Offshore, Clearwater and its Can-do drillship. The intention is to divest this over time, and the management expects this to require limited initial funding

Dev co will see the two semi-subs for Sete Brasil and Awilco and five jack-up rigs for Borr Drilling injected into Dev co. This structure will be dissolved once the rigs have been completed and delivered to customers or transferred to Rig co. Both Rig co and Dev co are collectively expected to require about S$500mn in net funding, mainly for Dev co to complete the rigs.

Keppel has started reclassifying its businesses under Energy & Environment, Urban Development, Connectivity and Asset Management. It has started reporting its financials under these new segments.

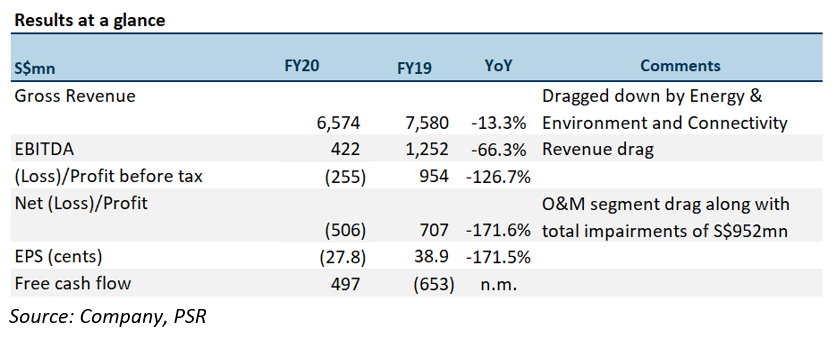

Results summary

For 2H20, revenue declined 20% to S$3.4bn compared to the same period last year. The drag came from lower revenue in the Energy & Environment and Connectivity segment partly offset by higher revenues from Urban Development and Asset Management. For FY20, Group revenue declined by 13% y-y to S$6.6bn, coming ahead of our estimates by S$435mn helped by better than expected results from the Urban Development segment. All key business units were also profitable except for their O&M unit. Excluding impairments in both years, FY20 net profit was S$446mn vs. S$828mn in FY19.

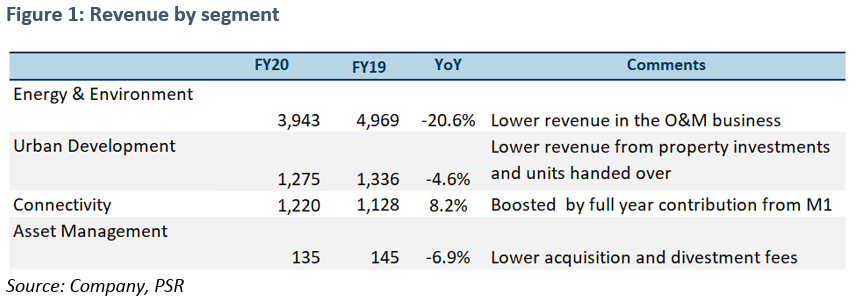

Energy & Environment: Revenue from this segment declined by 32% in 2H20 due to significantly lower revenue in the offshore & marine business as a result of slower progress from certain on-going projects due to COVID-19 related disruptions, suspension of revenue recognition from Awilco contracts, and deferment of some projects. For FY20, revenue in this segment declined an overall 20.6%.

Urban Development: Revenue increased 8% in 2H20 vs. the same period last year mainly due to higher contribution from property trading projects led by a higher number of units handed over for Waterfront Residences in Wuxi, Seasons Residences in Wuxi, Sheshan Riviera in Shanghai and Seasons Residences in Shanghai, which were partly offset by fewer units handed over in Riviera Point in Ho Chi Minh city, Park Avenue Heights in Wuxi, 8 Park Avenue in Shanghai, as well as lower contribution from the Reflections & Corals at Keppel Bay in Singapore. For FY20, this segment saw a 4.6% decline in revenue compared to last year.

Connectivity: Revenue saw a 5% drop in 2H20 vs the same period last year due to lower roaming service revenue as a result of COVID-19 and lower handset and equipment sales in M1, as well as lower contribution from their logistics business following the divestment of certain China logistics assets in November 2019. For FY20, revenue from this segment increased 8.2% vs. the same period last year, boosted by full year contribution from M1.

Asset Management: Revenue increased 3% in 2H20 vs. the same period last year largely due to higher asset management fees, partly offset by lower acquisition fees. For FY20, this segment saw a 7% decline in revenue due to lower acquisition and divestment fees.

For 2H20, the Group reported a net profit of S$31mn, as compared to S$351mn for the same period last year. Profits from Urban Development, Asset Management and Connectivity were partly offset by losses at Energy & Environment. For FY20, net loss was S$506mn vs. net profit of S$707mn for FY2019, excluding impairments, mainly from the O&M business, net profit would have been S$446mn. Net gearing was 0.91x as at end-Dec 2020, had the Keppel Tower transaction been completed in Dec 2020 however, net gearing would have moved to 0.81x on a pro-forma basis.

Maintain BUY with unchanged target price of S$6.12

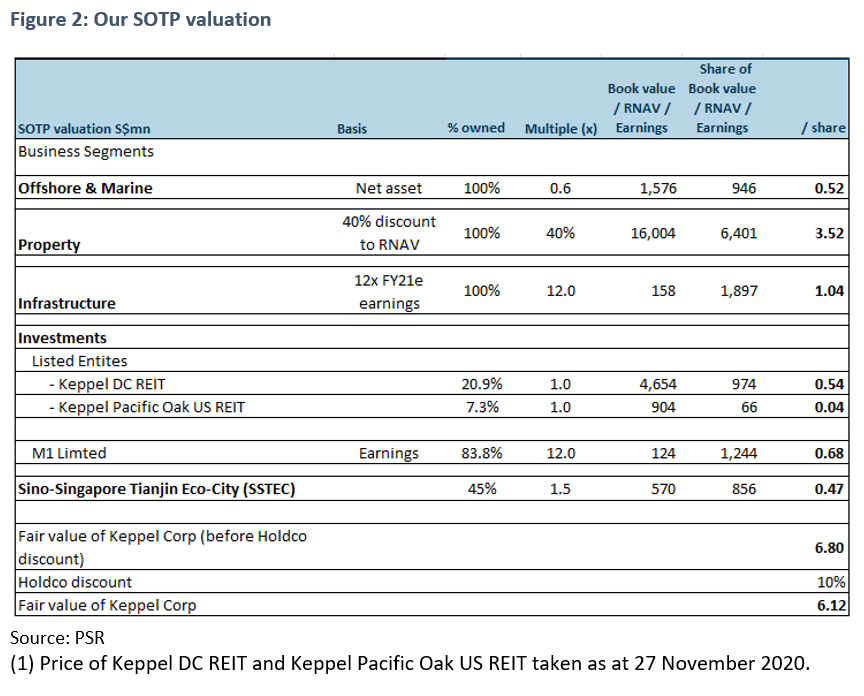

We maintain our SOTP valuations at S$6.12 based on FY21e segments and maintain our BUY recommendation. Our TP is based on sum-of-the-parts (SOTP) valuation with a 10% holding-company discount. We value its Offshore & Marine division at 0.6x book value, about a 16% discount to peers (Figure 2). We value its Property segment at a 40% discount to RNAV and Infrastructure division at 12x FY21e earnings, in-line with peers. We also value M1 at 12x FY21e earnings, a slight discount to listed peers’ average of 13x. We value Keppel’s stake in Sino-Singapore Tianjin Eco-city at 1.5x book value.

Risks to our view include 1) a prolonged resolution for Rig co, 2) a further weakening of oil prices and 3) a worsenin of economic uncertainties.

We estimate the book value of Keppel for FY20e and FY21e at S$10.7bn and S$11.2bn respectively or S$5.90 and S$6.14 per share. Our TP of S$6.12 translates to about ~1.0x FY21e book value (a slight discount to their 5-year average of 1.05x).

Keppel has been promoting intra-company collaboration for some time. To this end, it has introduced OneKeppel. Collaboration initiatives may include but are not limited to large-scale urban developments or floating data-centre parks. The development of these projects will involve different capabilities within the Group. But as we think OneKeppel will take time to materialise, we have ascribed a 10% hold-company discount to arrive at our target price of S$6.12. Over time, as management continues to break down the silos, we see the potential for this discount to narrow, leading to higher valuations.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Terence specialises in the consumer, conglomerate and industrials sector. He has over five years of experience as an analyst in the buy- and sell-side. As an institutional fund management analyst, he sat on the China-Hong Kong desk. Terence was ranked top 3 for Best Analyst under the small caps and energy category in the Asia Money poll 2018.

He graduated from the Singapore Management University with a major in Finance (Honours), and is the honoured recipient of the CFA scholarship.