Company Background

Keppel Corp is an investment holding and management company with operations in Offshore & Marine, Infrastructure, Property and Investments.

Investment Merits

Outlook

Its strategic reviews and Vision 2030 are expected to put the Group firmly on the road to its ROE target of 15%. This is expected to lead to a strong re-rating of its shares.

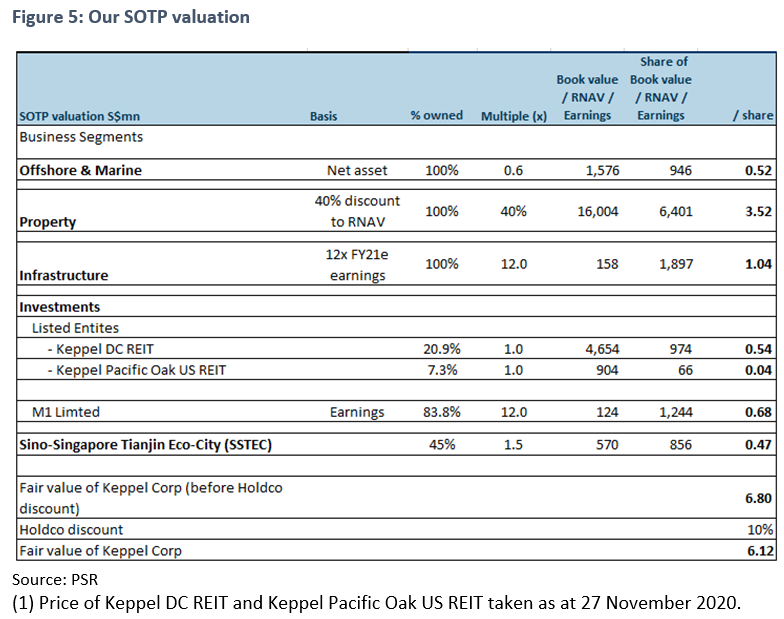

Initiating coverage with BUY rating and TP of S$6.12

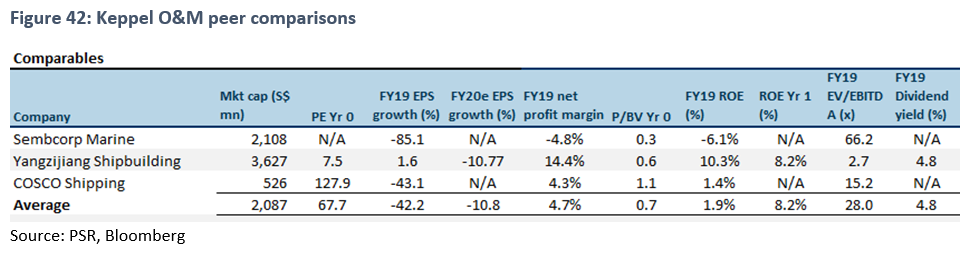

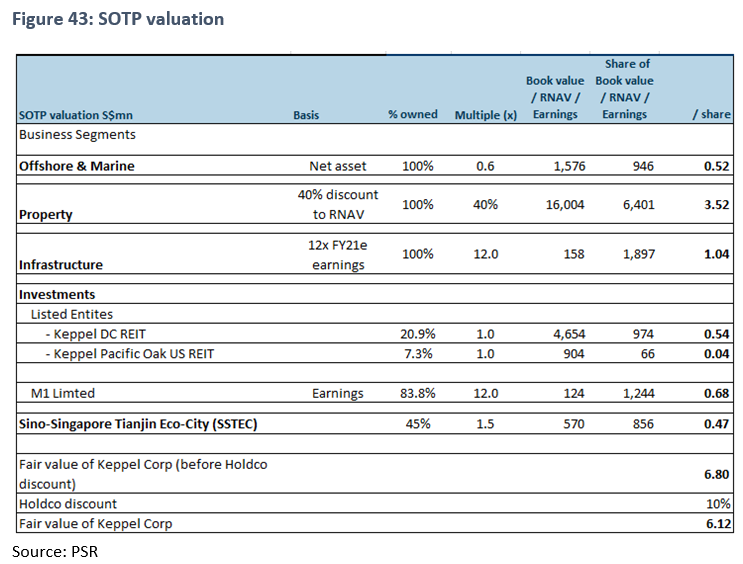

We initiate coverage with a BUY recommendation and target price of S$6.12. Our TP is based on sum-of-the-parts (SOTP) valuation with a 10% holding-company discount. We value its Offshore & Marine division at 0.6x book value, about a 16% discount to peers (Figure 42). We value its Property segment at a 40% discount to RNAV and Infrastructure division at 12x FY21e earnings, in-line with peers. We also value M1 at 12x FY21e earnings, a slight discount to the sector average of 13x. We value Keppel’s stake in Sino-Singapore Tianjin Eco-city at 1.5x book value.

Background

Keppel Corp is an investment holding and management company for offshore and marine engineering and construction services. It also has interests in Infrastructure, Property and Investments.

Six years after the O&M downturn, Keppel has announced a strategic review of its O&M division, with a decision expected in January 2021.

It has rolled out OneKeppel as part of its Vision 2030 strategy, to harness synergies within the Group and pave the way for greater scalability.

Business segments

Offshore & Marine includes offshore rig design, construction, repair and upgrading, ship conversions, repair and specialised shipbuilding.

Property covers property development, investment and fund management. Keppel Land, with a pipeline of about 45,000 homes in Singapore and overseas, is diversified in Asia, with Singapore, China and Vietnam as its key markets.

Infrastructure focuses on environmental engineering, power generation, logistics and data centres, where the Group owns and operates competitive energy and infrastructure solutions and services.

Investments consist mainly of interests in investment holding companies. These include Keppel Capital, the Group’s asset-management arm with AUM of S$33bn as at end-2019, and M1 Limited, a leading telco in Singapore with more than 2mn customers.

Keppel has started reclassifying its businesses under Energy & Environment, Urban Development, Connectivity and Asset Management. It has started reporting its financials under these new segments.

Business model

Recycling capital is a core part of the Group’s strategy. It has set up different REITS and trusts to recycle capital: Keppel DC REIT (Neutral, TP: 2.91), Keppel REIT (NR) and Keppel Infrastructure Trust (NR) to list a few.

From the time an asset is created till its injection into a Keppel-managed trust or fund, their business model generates multiple income streams which enables the Group to create and capture value across its businesses. To accelerate growth, the Group is also expanding its capital base. It has been bringing on board like-minded co-investors through its private funds to seize opportunities for asset creation without straining its balance sheet. This turns its assets efficiently and unlocks value.

Investment Merits

Initiating coverage with BUY and target price of S$6.12

We initiate coverage with a BUY recommendation and target price of S$6.12. Our TP is based on sum-of-the-parts (SOTP) valuation with a 10% holding-company discount. We value its Offshore & Marine division at 0.6x book value, about a 16% discount to peers (Figure 42). We value its Property segment at a 40% discount to RNAV and Infrastructure division at 12x FY21e earnings, in-line with peers. We also value M1 at 12x FY21e earnings, a slight discount to the sector average of 13x. We value Keppel’s stake in Sino-Singapore Tianjin Eco-city at 1.5x book value.

Risks to our view include 1) lack of clear resolution to strategic review of O&M unit, 2) a further weakening of oil prices and 3) uncertain economic outlook.

Investment merits

We estimate the book value of Keppel for FY20e and FY21e at S$10.7bn and S$11.2bn respectively or S$5.90 and S$6.14 per share. Our TP of S$6.12 translates to about ~1.0x FY21e book value (a slight discount to their 5-year average of 1.05x).

Keppel has been promoting intra-company collaboration for some time. To this end, it has introduced OneKeppel. Collaboration initiatives may include but are not limited to large-scale urban developments or floating data-centre parks. The development of these projects will involve different capabilities within the Group. But as we think OneKeppel will take time to materialise, we have ascribed a 10% hold-company discount to arrive at our target price of S$6.15. Over time, as management continues to break down the silos, we see the potential for this discount to narrow, leading to higher valuations.

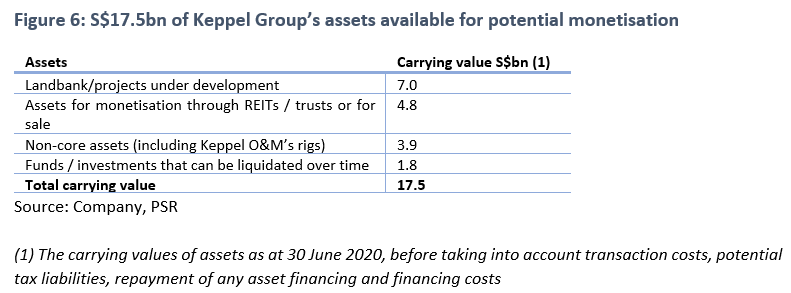

Vision 2030: to monetise assets worth S$17.5bn

Reaffirmation of capital recycling. Keppel has identified S$17.5bn of assets that can be monetised. While there has always been value in Keppel for unlocking, the question was always “when”. The latest details provide colour on the assets available for monetisation as well as a timeline. This provides greater clarity of the Group’s outlook.

In total, Keppel intends to monetise S$7.0bn of its landbank (Figure 6), which is held at historical cost. It also intends to monetise S$4.8bn of investment properties and assets being developed/stabilised for monetisation through Keppel-managed or third-party platforms. Non-core assets, including Keppel O&M oil rigs amounting to S$3.9bn, have also been identified for divestments. Various funds and investments amounting to S$1.8bn are also expected to be liquidated over time.

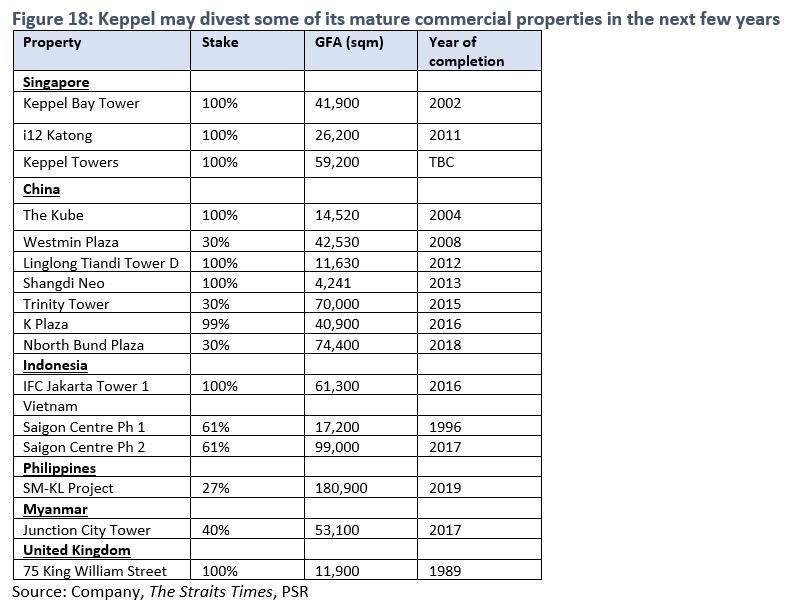

While asset recycling has been a key part of the Group’s strategy, we think setting a clear target of monetising S$3-5bn of assets over the next three years provides greater clarity to investors. We believe Keppel could be looking for buyers for its stranded rig-building contracts, which include five jack-up rigs and one Cando Drillship. We estimate their market value at US$700-900mn or S$1.3-1.4bn. Keppel could also divest commercial buildings in its portfolio like Keppel Bay, Keppel GE Tower or i12 Katong to REITs.

We believe Keppel will reinvest the proceeds in new, vibrant areas of growth such as renewable energy solutions, integrated urban development and data centres. At the heart of its Vision 2030 is its goal to provide solutions in sustainable urbanisation, clean energy and smart nation.

To help it get there, Keppel has established a Vision 2030 transformation office, including a 100-day programme. The office was set up at the end of September, which implies the Group could provide more details as early as January. This is expected to lead to a stock re-rating.

Strategic review of Keppel Offshore & Marine timely

Commenced strategic review. Keppel is reviewing its O&M operations amid the sector’s downturn. It will explore both organic and M&A options. Organic options include reviewing the strategy and business model of Keppel O&M, assessing its current capacity and global network of yards and restructuring to seek opportunities as a developer of renewable energy assets. M&A options range from strategic mergers to disposals. Keppel declined to provide details as the review in in a preliminary stage, but has stressed that all options are on the table.

The review comes hot on the heels of a pullout by Temasek’s wholly-owned subsidiary, Kyanite Investment Holdings, from its S$4.1bn partial offer for Keppel in August this year. This was after Keppel reported 2Q20 losses of S$697.6mn. The walkaway breached a precondition for the partial buyout. Kyanite Investment defended its move by invoking a material adverse change clause, which states that Keppel’s profit after tax must not fall by more than 20% over the cumulative four quarters from the third quarter ended September 2019. Even though Temasek has pulled out of the deal, we believe Keppel will still undertake its O&M review in consultation with Temasek. Recall that Kyanite initially announced it would make a comprehensive strategic review of Keppel with the objective of creating sustainable value for all shareholders after the deal.

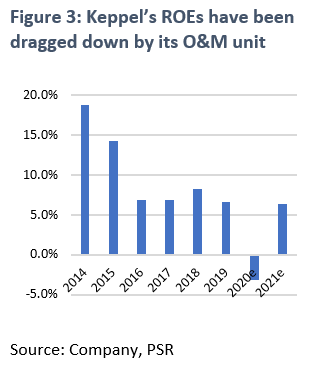

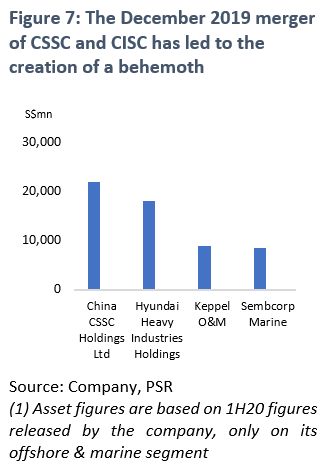

We believe that ultimately, Keppel O&M will be deconsolidated. Three reasons for this: 1) even though Keppel had assets of S$9.5bn in FY19, O&M EBIT was only about S$145m. This means that Keppel generated only 1.5% in returns from its offshore & marine assets, which is a drag on its performance; 2) globally, there is still overcapacity in shipbuilding. Competition is expected to stiffen from consolidated or consolidating Chinese and South Korean shipyards. Just last December, China State Shipbuilding Industry Co (CSSC) merged with China Shipbuilding Industry Co (CSIC) [SHA: 600150, Not Rated]; and 3) oil prices remain volatile. Upstream capex this year was cut by about 22% after the oil-price slump. For 2021, the outlook has improved in the last few months, but is still expected to remain subdued.

In our view, the case for merging Keppel O&M and SMM is compelling, given the challenging outlook for the sector. A merger of the two Singapore yards is expected to produce savings from eliminating overlapping functions. The merged entity would enjoy greater bargaining power in procuring raw materials and equipment. Merger could also free up idle or less productive yards for other forms of development.

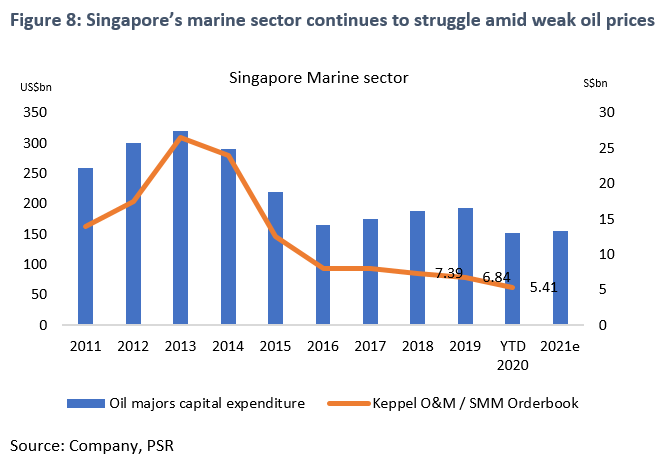

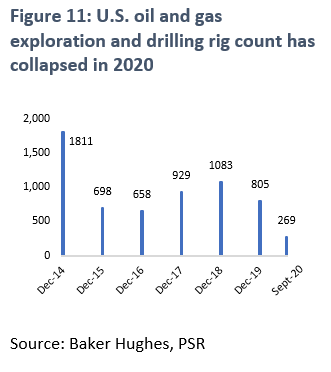

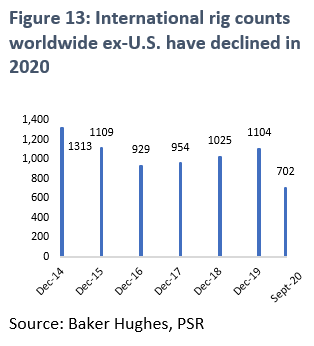

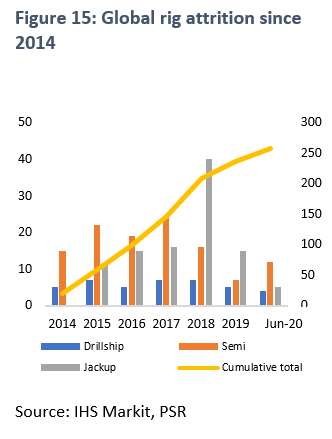

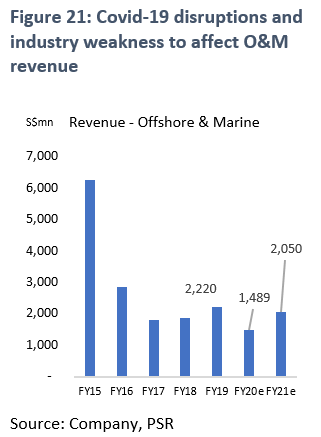

We expect the segment to remain weak in FY20e and FY21e as new orders remain slow. According to Baker Hughes, U.S. oil and gas exploration and drilling rig count has fallen sharply in 2020 (Figure 11), from 805 in December 2019 to 269 as at end-Sep 2020. International rig counts worldwide, excluding the U.S., have also declined (Figure 13), from 1,104 in December 2019 to 702 at end-Sep 2020. Data from IHS Markit suggest that 43 rig contracts have been terminated globally since the beginning of March this year. Few regions have been immune to terminations. Canada, the Gulf of Mexico, Latin America, the Mediterranean, Middle East and India all had their fair share of cancellations.

These cancellations give an indication of how activity could shape up in the near future. 2020 was set to be better with many dormant regions resuming exploration and the commencement of long-awaited development drilling programmes. The global pandemic, however, up-ended this. As operators slashed budgets, semis and jack-ups found themselves the hardest hit.

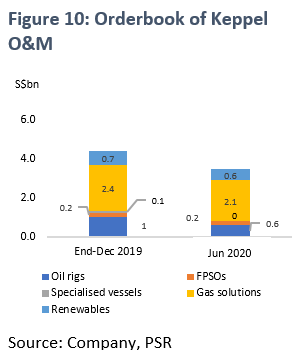

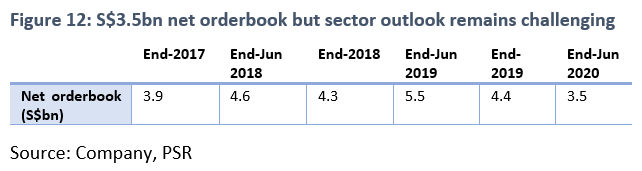

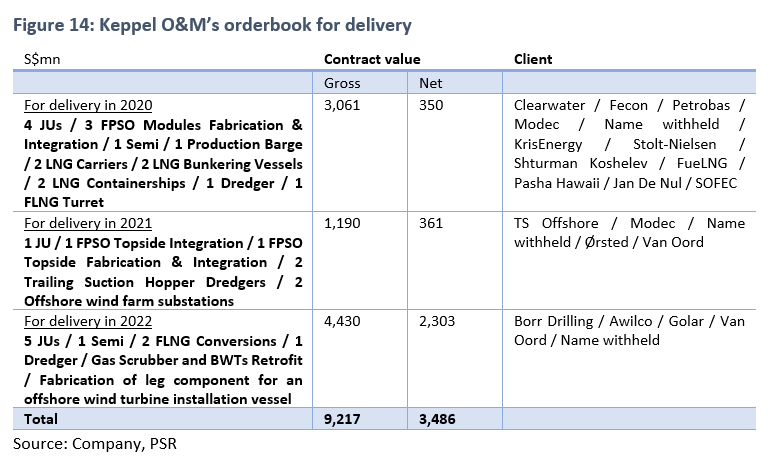

Keppel’s net orderbook from this segment stood at S$3.5bn in 1H20 (Figure 14). It recently secured a S$600mn contract from an energy company for the engineering, procurement and construction (EPC) of a vessel for the offshore renewable energy industry. New order wins have brought its YTD orders to S$1.0bn, a 3-year high.

Vision 2030: continuing the transformation

Vision 2030 commits Keppel to pivoting its focus to renewable energy solutions. We view their recent contract win of S$600mn in renewable energy is another step in this direction.

Current projects include building converter stations and substations to support the offshore wind energy industry in the German sector of the North Sea. Keppel’s share of its latest contract is about S$560mn. Keppel is also working on two offshore wind farm substations for OOO, a Danish renewable energy company, worth more than S$150mn. The contract comprises detailed EPC, testing and commissioning for two offshore wind farm 600MW substations.

We see Keppel O&M’s capabilities in offshore rig design, construction and repair and specialised shipbuilding as highly synergistic with its core business. In 2019, the Group established a new business unit, Keppel Renewable Energy, to pursue opportunities as a developer, owner and operator of renewable energy infrastructure.

Keppel O&M first entered the offshore wind market in 2010, when it secured a contract to build an electrical transformer and maintenance platform for a German offshore wind farm. This was followed by the commercialisation of its proprietary KFELS MPSEP, a multi-purpose self-elevating platform concept, in Keppel’s first offshore wind turbine installation vessel. It previously delivered Blue Tern, one of the world’s largest and most advanced multipurpose offshore wind turbine installers, for the UK North Sea. It has a stake in Blue Tern.

We see Keppel O&M tapping its expertise in offshore energy infrastructure to develop integrated solutions across the value chain of offshore wind farms. These would include offshore substations, foundations, installation and support vessels and accommodation platform solutions. We think its early mover advantage will give Keppel a critical competitive advantage against their Chinese and Korean competitors.

Vision 2030: property has the biggest monetisation potential

Under Vision 2030, Keppel’s property segment has the biggest monetisation potential. While the company did not spell out projects or landbank, we think Keppel will accelerate sales of its existing landbank in Tianjin Eco-City and its remaining plots in Keppel Bay. It could also divest commercial buildings like Keppel Bay, Keppel GE Tower or i12 Katong to REITs.

Land prices in many Asian cities have risen significantly over the years. As Keppel’s landbank and residential properties are carried at cost, there could be further upside for the Group if these are monetised at current market values. A significant portion – S$7.0bn or 40% of its S$17.5bn target for divestment – is carried at cost, representing potential meaningful upside.

We expect Keppel to accelerate land sales in its 45%-owned Tianjin Eco-City. This property already turned profitable in 2017, contributing S$50mn profits to Keppel in the last 2-3 three years. With residential property prices and demand in Tianjin remaining healthy (Figure 17), we expect the development to continue contributing S$55-60mn profits in the next few years. We expect the development to be fully sold by 2028

The Group is expected to seek out bigger land parcels for development in countries where it has strong domain knowledge. These include China, Vietnam and India. We think Keppel will look for land parcels with an average size of 700K sqm GFA or more. This size is similar to its Tianjin Eco-City (625k sqm GFA) and Saigon Sports City (781K sqm GFA). Plots of this size offer greater value-add in terms of opportunities for soft infrastructure than smaller land parcels.

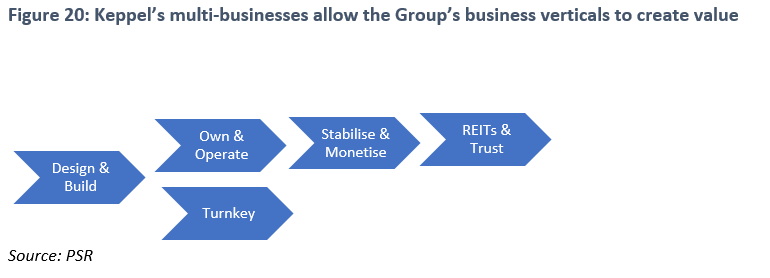

Business model: asset recycling

Asset recycling is a key strategy of the Group. It has set up different REITS and trusts to recycle capital: Keppel DC REIT (Neutral, TP: 2.91), Keppel REIT (NR) and Keppel Infrastructure Trust (NR) to list a few.

From the time an asset is created till its injection into a Keppel-managed trust or fund, the business model generates multiple income streams which enables the Group to create and capture value across its businesses. To accelerate growth, the Group is also expanding its capital base. It has been bringing on board like-minded co-investors through its private funds to seize opportunities for asset creation without straining its balance sheet. This turns its assets efficiently and unlocks value.

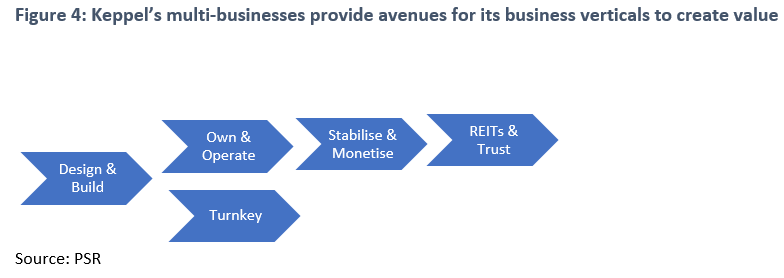

The Group has a strong track record of designing and developing high-quality real assets. These include rigs and ships, residential and commercial properties, data centres and power plants. Depending on the nature of its projects, Keppel either owns and operates the assets or sells products and provides turnkey solutions to customers. An example of this is jack-up rigs, Cantarell I, II and III, built to Keppel’s proprietary KFELS B Class design for Grupo R.

Turnkey: the Group sells products and provides turnkey solutions to customers. Examples are rigs and homes, which are handed over to customers when they are completed. In this phase of asset creation, business units earn development margins from the sale of solutions. An example is Keppel’s Property division, which develops quality homes, offices, commercial and integrated developments to create highly livable, vibrant and digitally-connected communities for sustainable urbanisation.

Own & operate: Keppel owns and operates many of the assets it creates. These are retained as investments for long-term, recurring income. Business units earn fees from leasing out and operating such assets. They can also earn from rendering project and asset management services to the private funds created by Keppel. Keppel Infrastructure, for instance, has a track record of developing, owning and operating power plants in Brazil, China, the Philippines and Nicaragua. In Singapore, it operates a 1,300-megawatt gas-fired combined cycle power plant on Jurong Island.

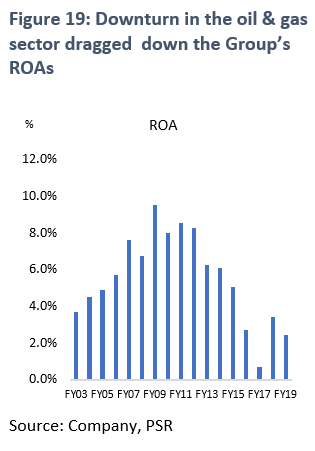

The heavy assets held as investments by Keppel and its private funds are revalued annually. They contribute revaluation gains to the Group each year. As these assets mature and are de-risked and stabilised, the Group can monetise them through divestments to its REITS and trusts as well as third parties. Turning the assets can enable the Group to achieve the best risk-adjusted returns from its investments, although the downturn in the oil & gas sector in the last few years has caused a drag on the Group’s earnings and ROAs.

The Group sponsors and manages real-estate and infrastructure trusts across its business lines, which it leverages to recycle capital from assets. Mature assets are well suited for divestment to REITs and trusts, for stable, recurring income. The injection of assets to these REITs and trusts helps the Group increase the portfolio of assets managed by the Group.

Revenue

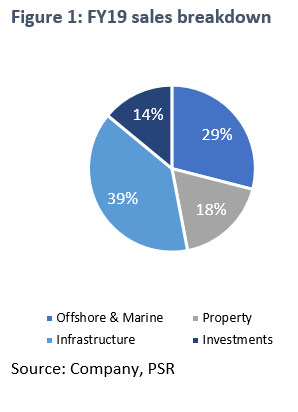

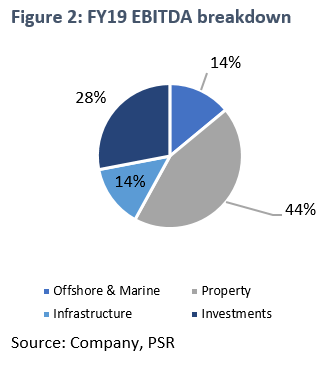

O&M comprised 29% of FY19 revenue. Despite product diversification in tandem with the changing global energy mix (offshore wind and LNG projects make up 72% of its S$900mn YTD new contracts), we expect continued industry oversupply to weigh on O&M

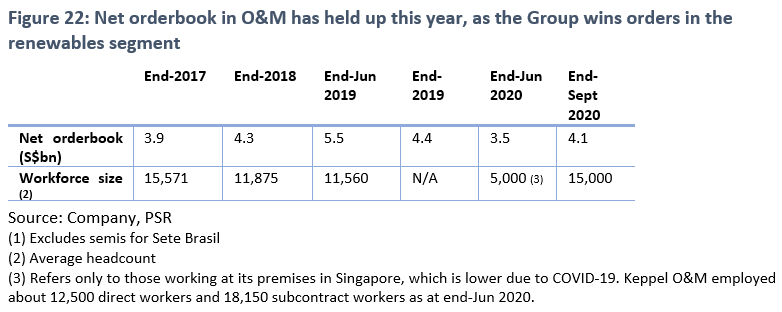

As at end-Sep 2020, net orderbook in this segment was S$4.1bn. This was roughly in line with the last three years. The orders would be recognised over two years. More recently, Keppel O&M secured a S$600mn contract in the offshore renewable energy industry. This boosted its orderbook further.

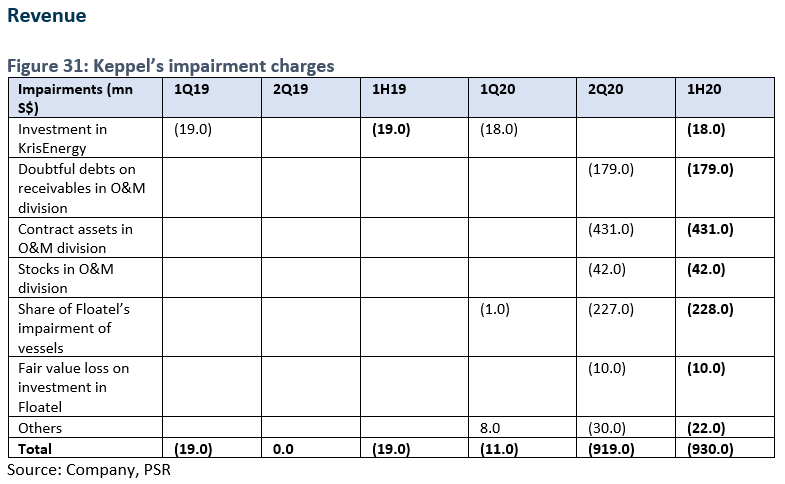

For FY20e, we expect Keppel O&M to report revenue of S$1.5bn (-33% yoy) due to Covid-19 disruptions and industry weakness. We expect a loss of S$521mn for FY20e mainly due to reduced topline and impairment charges of S$930mn in 2Q20 for stranded assets, receivables, stocks and share of provisions at Floatel. Excluding impairments, net profit would have been S$393mn for 1H20 (+5% yoy). Work at its shipyards has resumed, with 15,000 back at work as at end-Sep 2020 vs. 5,000 as at end-June (Figure 22). For FY21e, we expect revenue of S$2.1bn (+38% yoy), underpinned by its orderbook of S$4.1bn and work resumption at its yards.

In order to compete in this space, Keppel O&M is developing rigs of the future. It is leveraging digitalisation and analytics to enhance the efficiency and versatility of its rigs. It is also building yards of the future by incorporating robotics and artificial intelligence in its manufacturing processes to ensure it remains at the forefront of the industry.

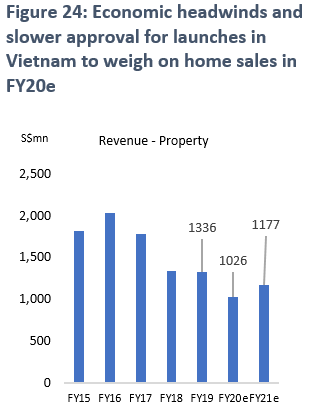

Property comprised 18% of FY19 revenue. Property has been Keppel’s most important source of profits in the last five years. Keppel Land continues to benefit from urbanisation in Asia, which drives demand for quality urban-living conditions. In 2019, Keppel Land sold 5,150 homes, up 16% from the 4,440 sold in 2018. The value of these sales was about S$3.2bn. Home sales in both China and Singapore have been healthy, growing by more than 50% yoy. Contributions from Vietnam have also been growing steadily.

Revenue

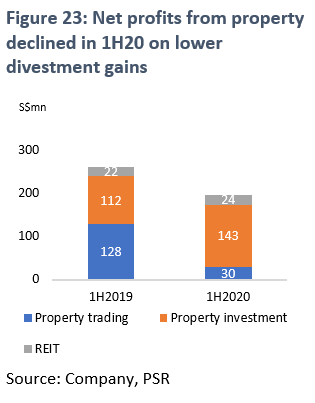

In its recent 9M20 operational update, home sales declined to S$1.5bn from S$2.1bn in the same period last year. The Group moved fewer units – 2,030 vs. 3,520 – this year due to economic headwinds in China and slower approval for new launches in Vietnam. China and Vietnam are the main sources of growth for Keppel Land. 1H20 property revenue and net profit declined due to lower divestment gains from Dong Nai Waterfront City in Vietnam and slower home sales in China, Vietnam, Singapore, Indonesia and India. The Group is expected to recognise the sale of 8,750 overseas units worth about S$4.2bn over 2H20-2024.

We expect Keppel to accelerate land sales in its 45%-owned Tianjin Eco-City. Tianjin Eco-City started turning profitable in 2017, contributing S$50mn profits to Keppel in the last 2-3 years. In October, the Group divested another plot, Plot 18b, which has a GFA of 79,684sqm, in Tianjin Eco-City. It realised a gain of S$18mn from the sale. With residential property prices and demand in Tianjin remaining healthy (Figure 17), we expect the development to continue contributing S$55-60mn profits in the next few years.

That said, we will be watching for potential headwinds in China after policymakers drafted “three red lines” in October this year. These are metrics on debt that developers will have to meet if they want to borrow more. Limits on developers’ borrowings might cause them to slash prices more aggressively to clear inventories. Along with the economic slowdown in China, this could affect Keppel’s sales in China.

In Singapore, we expect to see healthy demand for the Group’s new launches: The Garden Residences (74% sold as at end-Sep 2020) and 19 Nassim. We also expect the Group to unlock value in Keppel Bay Plot 4 through the launch of The Reef at King’s Dock in the first half of next year. This forms about 3% of Keppel Group’s RNAV.

For FY20e, we expect property revenue of S$1.0bn vs. S$1.3bn in FY19 (-23% yoy) as global home sales dropped. In FY21e, we expect the Group to speed up the divestment of land plots, in keeping with its Vision 2030 transformation plan.

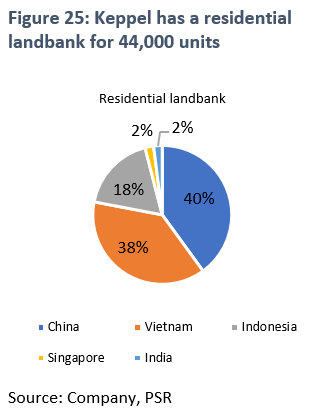

The Group had a residential landbank for about 44,000 homes as at end-Sep 2020 (45,000 at end-2019). More than 17,000 homes in key Asian cities will be launched from 2020 to 2022. In its commercial portfolio, Keppel Land has about 1.7mn sqm of GFA (1.6mn at end-2019). About half is under development and we expect the properties to be launched from 2022.

We also expect the Group to speed up the development of its current landbank and opportunistically replenish this landbank. We expect it to add bigger plots (780K sqm GFA), as bigger plots will allow the Group to contribute its expertise in soft infrastructure. Through Keppel Urban Solutions, a new unit established in 2017 to capitalise on the mega-trends of rapid urbanisation and the increasing global focus on sustainability, the Group is expected to play to its strengths in urban living. We think it will further leverage its strengths as an end-to-end integrated master developer of smart, sustainable precincts in the Asia-Pacific.

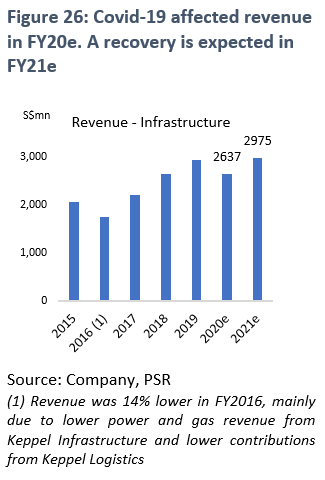

Infrastructure comprised 39% of FY19 revenue. Infrastructure has been growing steadily, delivering stable revenue (Figure 26) and net profit growth over the years. Its main businesses are energy infrastructure, environmental infrastructure, infrastructure services, data centres and logistics.

Revenue

YTD, Keppel Infrastructure has secured S$2.1bn worth of waste-to-energy and district cooling contracts in Singapore, India and Thailand. These include its latest S$300mn contract from JTC Corporation to build, own and operate a new district cooling system plant for 30 years. Expected to be completed in 2022, the plant will have a cooling capacity to serve up to 14,000 refrigeration tonnes.

For FY20e, we expect Infrastructure net profit to increase 90% yoy on the back of marked-to-market gains of S$131mn. The gains accrue from a reclassification of the Group’s interest in Keppel Infrastructure Trust from an associate to an investment, as well as gains from the sale of Keppel DC REIT units. Revenue, though, should decline by about 17% mainly due to lower power and gas sales and a slowdown in the progress of the Keppel Marina East Desalination Plant and Hong Kong Integrated Waste Management Facility as a result of Covid-19.

On the other hand, we expect logistics to be an indirect beneficiary of Covid-19, from higher demand for logistics solutions. Channel marketing sales at UrbanFox have also grown strongly, with more customers shopping online. Logistics revenue is expected to be higher this year despite lower contributions from some China logistics assets following their divestment in November last year.

Going forward, we expect Keppel to focus on growth areas such as data centres. In July 2020, the Group announced its first greenfield data-centre development in China, through the Alpha Data Centre Fund. We expect the Group to build up a portfolio of quality data centres gradually. We also think it will expand its omnichannel solutions to customers in Southeast Asia through Keppel Logistics as the Group taps growing demand for e-commerce in the region.

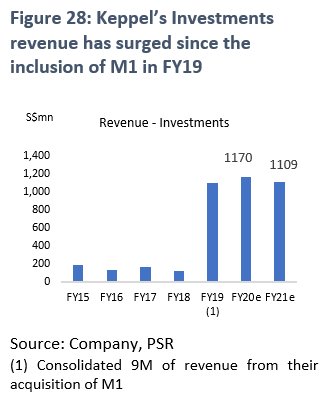

Investment comprised 14% of FY19 revenue. Revenue from this segment jumped to S$1.1bn in 2019 from S$121mn in 2018. This was mainly due to the consolidation of M1 and higher revenue from its asset-management business.

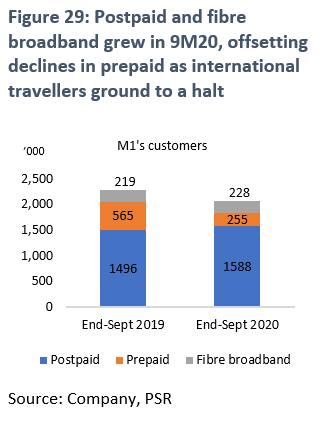

M1’s 9M20 EBITDA was resilient at S$202mn vs. S$211mn in 9M2019. The Group recently announced the divestment of Plot 18B in Tianjin Eco-City in October 2020. GFA for the site is 79,684 sqm, with Keppel recognising an S$18mn gain.

Keppel Capital – managed funds received total commitments of over US$2bn from investors, up from US$1.5bn in 1H20. Total commitments till date have come from pension and sovereign wealth funds. They recently announced a strategic cooperation with the National Pension Service of Korea to explore opportunities for infrastructure in Asia. For FY20e, we expect Keppel Capital to report total assets under management (AUM) of US$36bn, up from US$33bn in FY19.

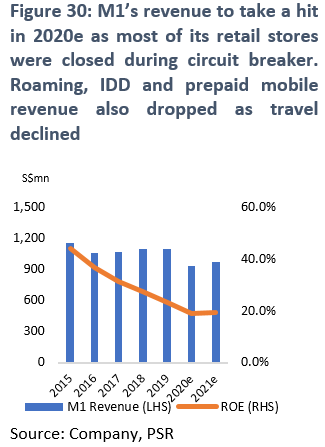

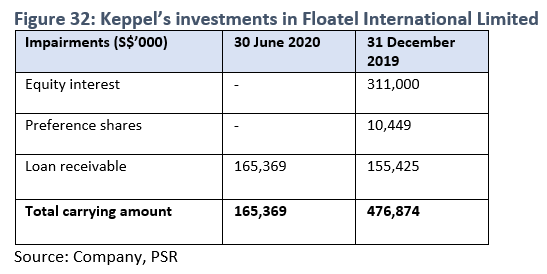

For FY20e, we expect revenue to increase to S$1.2bn from S$1.1bn in FY19 as Keppel consolidates full-year earnings from M1. M1 has been contributing net profits of S$25mn every quarter since its acquisition. Based on this, we expect S$23mn in FY20e and FY21e. M1’s revenue, however, is expected to drop 7.7% yoy from lower service revenue and equipment sales. We also expect this segment to report a loss of S$22mn in FY20e as it recognised an S$18mn impairment charge for KrisEnergy and impairment for Floatel in 2Q20 (Figure 32). Keppel had impaired all its equity investment in KrisEnergy in 1Q20.

The Group reported a net loss of S$698mn in 2Q20, hit by massive impairment charges totalling S$919mn. These were largely from the O&M segment. Excluding impairments, Keppel would have booked a net profit of S$393mn in 1H20. Management has guided for further potential impairments on Floatel as Floatel has announced an extension of its Forbearance Agreement with its bondholders to 15 November 2020. Keppel’s investment in Floatel International had a carrying value of S$165.4mn as at 30 June 2020 (Figure 32).

We conservatively write off the full S$165.4mn from Keppel’s equity value for FY20e as we await a resolution of Floatel. This pushes up our FY20e net gearing to 1.02x vs. 0.98x in 3Q20.

Keppel had also impaired all its equity investment in KrisEnergy in 1Q20 and ceased recognition of KrisEnergy in its P&L since.

Balance sheet

Group net debt was S$10.8bn in 1H20, for a net gearing of about 100%. About a quarter of this was in project finance loans. The increase in net gearing was largely caused by an increase in Group net debt and a reduction in total equity from the impairment of its O&M division. Group net debt had surged in FY19 following its acquisition of M1, consolidation of M1’s net debt of S$0.3bn, acquisition of the remaining interest in Keppel T&T and the recognition of lease liabilities arising from the adoption of SFRS (I) 16 Leases of S$0.6bn.

Group net gearing is expected to increase to 102% this year from 84% last year, as we have conservatively written off the full S$165.4mn value of Keppel’s investment in Floatel. For FY21e, we expect net gearing to be lower at 96%. This is because debt requirements would drop by about S$853mn as it speeds up the divestment of assets with a carrying value of S$17.5bn.

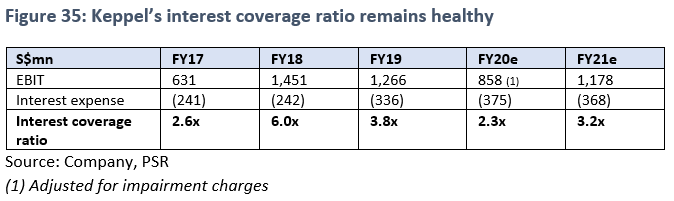

We think the Group remains well positioned to manage its interest in FY20e and FY21e. We have adjusted Group FY20e EBIT for impairments recognised by the Group in 1H20. This gives an interest cover of 2.3x for FY20e. We expect interest cover to improve to 3.2x in FY21e on the back of improved operations and increased divestments.

Keppel had S$2.4bn of cash and S$12.7bn of debt in 1H20. It has S$3.0bn of loans and committed bank facilities. This should put it in good stead to ride out the crisis. That said, we do not expect the Group to increase borrowings in the next few years as it turns to divesting S$17.5bn of assets over the next few years.

Notwithstanding the economic outlook, we believe the Group’s gearing will remain elevated in the next two years as it continues to spend on acquisitions (e.g. investment properties) and build new logistics and data-centre facilities. In the mid-term, we expect the monetisation of assets to drive down its net gearing to its long-term average of 65-75%.

Cash flow

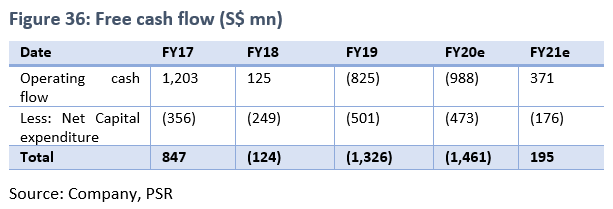

We expect continued negative FCF in FY20e as lockdowns in 1H20 and slower property sales, weighed on its cash flows. Without the massive impairments of the O&M segment, core net profit would have been S$222m (+45% yoy). As such, we forecast S$638mn profits for FY21e and S$195mn FCF as operations resume.

We believe Keppel has a number of options for shoring up its cash flow. One is to lighten assets in its O&M and Property segments as they make up the largest chunks of its balance sheet. We believe Keppel could be looking for buyers for its stranded rig-building contracts, which include five jack-up rigs and one Cando Drillship. We estimate the market value of these rigs at US$700-900mn or S$1.3-1.4bn. Keppel could also divest some commercial buildings like Keppel Bay, Keppel GE Tower or i12 Katong to REITs.

In addition, Keppel could pare down stakes in some of the listed REITs it owns. We think a comfortable ownership range is 15-20% for the REITs. We think it could potentially pare down its stake in Keppel REIT from 49% and Keppel DC REIT from 23%. These could translate to revaluation gains for the Group, shoring up its cash flow. Keppel recently recognised a marked-to-market gain of S$131mn from reclassifying Keppel Infrastructure as an investment from associate in 1Q20.

While Keppel has no fixed dividend policy, it paid out 20-30 Singapore cents in FY15-FY19. This represented 40-50% payouts. Even though we expect the Group to report a loss in FY20e, we believe it will still propose a final dividend. The Group reported a half-year loss of S$537mn but paid out an interim DPS of 3 Singapore cents in 1H20. We think it will declare 6 Singapore cents, down from 12 Singapore cents last year, as its final dividend for FY20e. The total DPS of 9 Singapore cents would represent a payout of about 45% of the Group’s profit, excluding impairments.

Prospects

Keppel has unveiled a 10-year roadmap that will transform its business to meet its 15% ROE target. Under Vision 2030, Keppel has redefined its businesses as energy and environment, urban development, connectivity and asset management. It has started reporting earnings based on these new segments. In our financial analysis, however, we have kept to its previous reporting segments for ease of comparison.

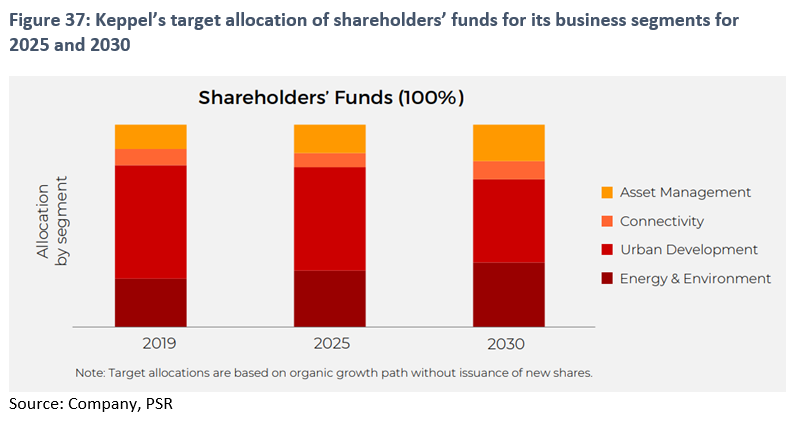

The Group intends to achieve its ROE target by focusing on new growth areas, divesting non-core assets, increasing funds allocated to asset management and recycling capital through its landbank. The Group will reinvest funds in gas value-chain renewables and environmental solutions (Figure 37), integrated projects, data centres, senior living and 5G services.

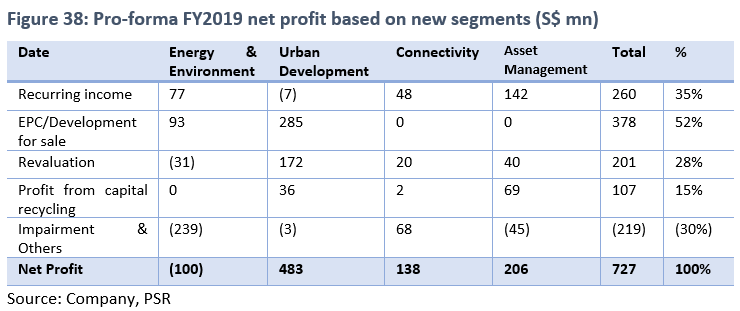

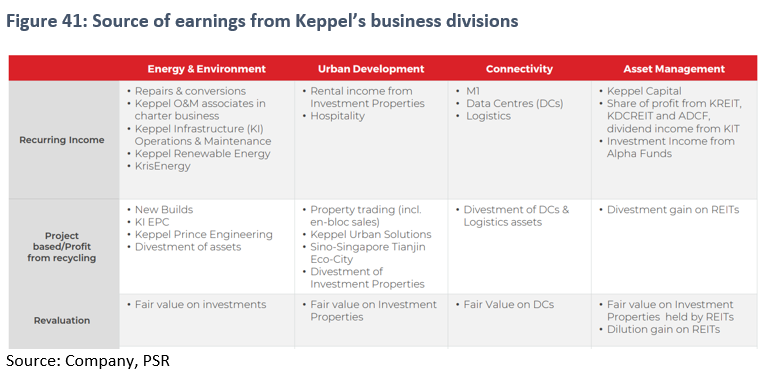

Keppel also intends to reduce its reliance on lumpy project-based earnings and increase recurring income. Based on its proforma FY2019 earnings (Figure 38), 35% of its earnings is recurring in nature. We believe Keppel will increase this to 50% in the mid-term and 60% over the long term by targeting asset management, connectivity and energy & environment. A breakdown of the sources of its earnings is provided in Figure 41.

Keppel 2030

A big part of Vision 2030 is to break down the silos within the Group to allow it to extract the most group synergies and create quality solutions for customers. We think the challenge here is execution. We are cautiously optimistic that management will be able to pull this off as Keppel has already combined its urban-development capabilities with its logistics, data-centre and connectivity businesses to deliver smart solutions for sustainable urbanisation in the Asia Pacific. We expect the Group to deepen the collaboration between its different business units to harness greater synergies.

Besides organic growth, it is expected to pursue strategic M&As to accelerate growth.

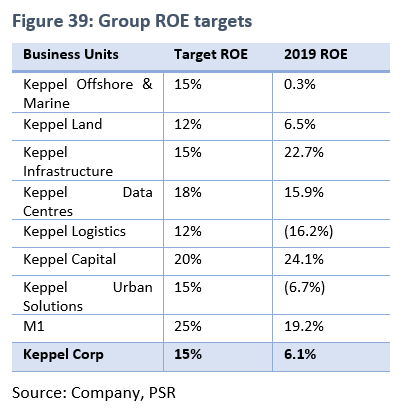

Keppel has established ROE targets for its individual business units to help it achieve (Figure 39) a 15% Group ROE. While the targets for Keppel O&M and Keppel Logistics may be on the high side, we expect the current strategic review of both divisions to provide greater clarity.

Even though Temasek has pulled out of its partial offer, we believe Keppel O&M’s strategic review will still involve Temasek, given Temasek’s stakes in both Sembcorp Marine and Keppel. Had the Temasek offer gone through, we believe Keppel O&M would have been merged with Sembcorp Marine because of the current challenges in the offshore & marine sector.

Keppel Logistics is also being reviewed. This business has been an indirect beneficiary of Covid-19, with higher demand for its logistics solutions. We believe the Group could announce a further streamlining of the business along the lines of its facilities in Foshan and Hong Kong.

We expect an announcement of its review outcomes by mid-January, which would be 100 days from the establishment of its 100-day transformation office.

To achieve its 15% ROE target, the Group will likely pivot to renewables, environmental solutions, nearshore floating infrastructure, connectivity solutions including green data centres, and integrated smart district development.

Redefining Keppel’s divisions

As part of Vision 2030, Keppel plans to become an integrated business, providing end-to-end solutions for sustainable urbanisation. This integration would be backed by an asset-management arm to fund the Group’s growth and provide a platform for capital recycling.

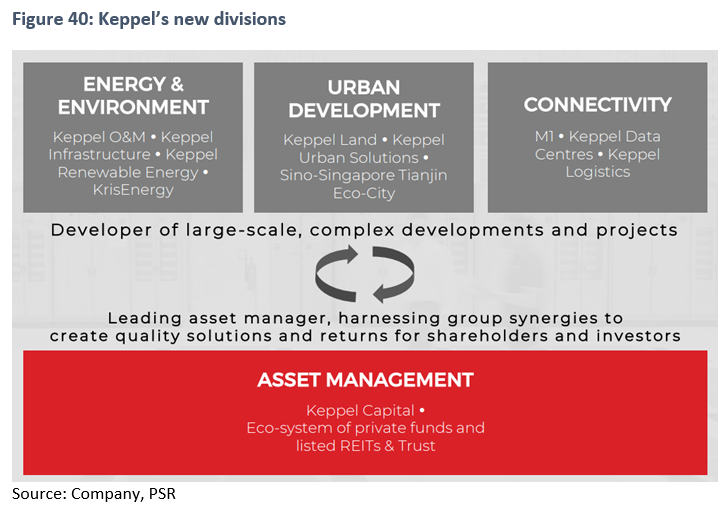

The Group’s four new focus areas of energy and environment, urban development, connectivity and asset management are all part of a connected value chain. Keppel will move away from reporting earnings under its previous four businesses – offshore & marine, property, infrastructure and investments – to these four new businesses.

Under its new classifications, energy and environment will comprise the Group’s O&M portfolio, renewable energy, infrastructure and KrisEnergy. Urban development will consist of Keppel Land, Keppel Urban Solutions and the Sino-Singapore Tianjin Eco-City. Connectivity will comprise the Group’s stakes in M1, data centres and Keppel Logistics. The Group’s asset management is made up of Keppel Capital and an eco-system of private funds and listed REITS and trusts.

Future plans – OneKeppel approach to harness synergies

We are cautious but optimistic on the Group’s plan to integrate their different units together to develop a comprehensive solution for their customers. We believe this will take time to realise, but will be increasingly important in this competitive landscape. We see the possibility of the conglomerate discount attached to Keppel narrowing over time if the Group executes well in this area, leading to higher valuations for the Group.

We see Keppel’s future focus centred around the following themes set out below:

In achieving their 15% ROE target, the Group will likely focus more on areas like renewables, environmental solutions, nearshore floating infrastructure, connectivity solutions including green data centres, as well as integrated smart district development.

The Group has also been promoting intra-company collaboration in recent years. Keppel recently announced a slew of new appointments for its new business units. Touted as its “next-generation” leaders, they are part of the team that formulated Vision 2030. As the new team works on OneKeppel to harness Group synergies and capture new profit pools that might not be available to silos, we expect the Group to enter into larger and higher-value projects. These may include large-scale urban developments or floating data-centre parks, which will rope in the different capabilities within the Group. Keppel has already announced plans to deploy M1’s digital solutions and the impending 5G network to enhance its suite of offerings.

Elsewhere, Keppel has committed to becoming a developer of renewable energy solutions. The Group has set targets to reduce carbon emissions and waste generation. It established Keppel Renewable Energy in 2019 to explore opportunities in renewable energy infrastructure. While this is still early days, this diversification is beginning to bear fruit. In 2019, Keppel O&M secured more than S$2bn in new orders, with gas and offshore renewables making up over 60% of the new orders. In order to compete in this space, Keppel O&M is also developing rigs of the future, leveraging digitalisation and analytics to enhance the efficiency and versatility of its rigs. It is building yards of the future by incorporating robotics and artificial intelligence in its manufacturing processes to ensure it remains at the forefront of the industry.

Valuation

We initiate coverage of Keppel Corp with a BUY recommendation and target price of $6.12. Our TP is based on SOTP valuation with a 10% holding-company discount. We value O&M at 0.6x book value, about a 16% discount to peers (Figure 42). We value its Property segment at a 40% discount to its RNAV, which is in-line with the sector average, and Infrastructure at 12x FY21e earnings, in-line with peers. We also value M1 at 12x FY21e earnings, a slight discount to the sector average of 13x. We value Keppel’s stake in Sino-Singapore Tianjin Eco-city at 1.5x book value.

We are cautiously optimistic on the Group’s plan to integrate its different units to develop comprehensive solutions to its customers as we believe fruition will take time. If executed well, however, we see the possibility for its conglomerate discount to narrow, potentially leading to higher valuations.

We estimate the book value of Keppel for FY20e and FY21e at S$10.7bn and S$11.2bn respectively, or S$5.90 and S$6.14 per share. Our TP of S$6.12 translates to 1.0x FY21e book value about 1.0x FY21e book value, a slight discount to their 5-year average of 1.05x.

Keppel has been deepening their efforts in recent years to promote intra-company collaboration, they have adopted a OneKeppel approach to harness the synergies of the Group and capture new profit pools that might not be available to individual business entities. Some examples of these may include but are not limited to large-scale urban developments or floating data centre parks. The development of these projects involve different capabilities within the Group, allowing them to harness their offerings to enhance its suite of offerings. We think these initiatives will take time to realise however, and we attached a 10% holdco discount to the Keppel Group to arrive at our target price of S$6.15. Over time, as the management continue to break down the silos within the different divisions, we see the potential for this discount to narrow over time, which could lead to higher valuations for the Group.

Risks

Lack of clear resolution in strategic review of Keppel O&M. Keppel has launched a strategic review of their O&M unit, with an outcome expected next month. The failure to chart a clear plan for their O&M unit could lead to added uncertainty on the Group’s future outlook.

Collapse in oil prices leading to contract cancellations or delays in new orders. Oil prices remain below pre-Covid-19 levels. This could have an adverse impact on the sector in terms of increased cancellations or defaults. Keener competition from Chinese yards after the recent merger of China’s CSSC and CISC could affect the Group’s order wins and profitability.

Economic slowdowns could affect take-up and demand for Keppel’s new property launches. Covid-19 has slowed down the development of new properties in Singapore, China and the rest of the world. The delays, accompanied by an uncertain economic outlook, can affect take-up and demand for the Group’s integrated developments and properties.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Terence specialises in the consumer, conglomerate and industrials sector. He has over five years of experience as an analyst in the buy- and sell-side. As an institutional fund management analyst, he sat on the China-Hong Kong desk. Terence was ranked top 3 for Best Analyst under the small caps and energy category in the Asia Money poll 2018.

He graduated from the Singapore Management University with a major in Finance (Honours), and is the honoured recipient of the CFA scholarship.