Report type: Weekly Strategy

Will We Be Freed from Negative Interest Rates from Next Year Onwards?

At the Monetary Policy Meeting held on 19/12, the Bank of Japan decided to maintain their large-scale monetary easing policy which will see the short-term interest rate controlled at -0.1% and the long-term interest rate at 0%. With the US FRB implementing a policy from Oct 2019 as a plan up to FY2020/4-6 to expand their balance sheet by buying 60 billion dollars of short-term government bonds per month in order to resolve insufficient funds in the short-term monetary market, as well as the ECB in Europe to carry out a policy review starting from early next year which will last for about a year, these policies explore the “reversal rate”, where the harmful effects of a negative interest rate will outweigh its good effects.

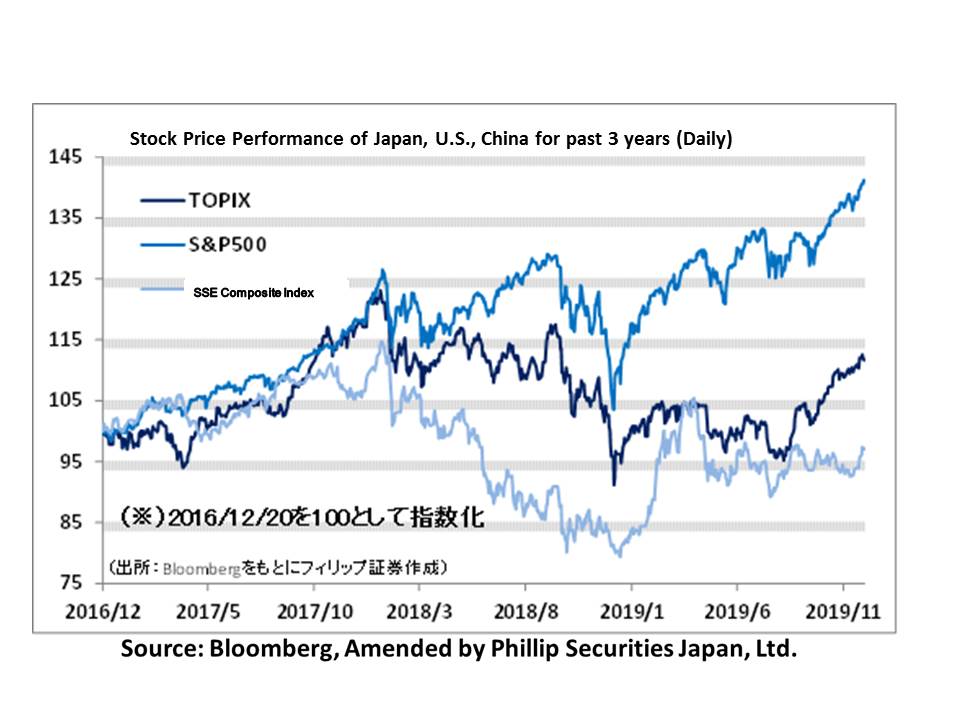

For the Japanese stock market in the week of 16/12, due to the phase-one deal being reached in the US and China trade talks in the weekend before which led to an easing of concerns of the US-China trade friction causing a burden on the global economy, on 17/12, the Nikkei average rose to 24,091 points. After which, it was pushed back by profit-taking, which saw the Nikkei average falling to the 23,700 point level on 20/12. In terms of supply and demand, based on the reference of 13/12, the ratio obtained by dividing the “unsettled selling balance of arbitrage” by the “unsettled buying balance of arbitrage” involving spot and futures arbitrage rose to 0.95 times. It appears that the buying pressure which followed the relief of positions of the unsettled selling balance of arbitrage had come full circle.

In contrast with Japan, the US and Europe, on 19/12, the central bank of Sweden raised its policy interest rate from a negative interest rate to 0%. While side effects are increasing in severity to a point where it cannot be ignored, such as not being able to curb the swelling household debt, worsening pension fund management, a decline in bank revenue as well as prolonging the lifespan of companies with low profitability, it seems to have been a decision that was made because there were no signs of improvement in the economy and in prices. Although Sweden was traditionally an export-dominated economy strong in the manufacturing industry, its industry structure is changing due to the emergence of IT companies, and in the background, there is also a decreasing demand for a weaker currency. On the other hand, a yen appreciation has been viewed as a source of concern for the Japanese stock market and the Japanese economy. This could indicate that its export-dominated economic structure has not changed as much when compared with Sweden. Despite recent new developments such as movements from the business merger between LINE (3938) and Yahoo Japan’s parent company, ZHDS (4689), there is the glaring fact that there is still insufficient transformation in the industry structure involving an emergence of IT companies, etc. In addition, there are over 1,800 trillion yen of individual financial assets in Japan. We can also consider the route of having the economy develop as a financial nation by bringing in money from across the world via the adoption of a flexible strong currency policy such as Singapore. However, this would likely be regarded as contradictory to Abenomics policies. From next year onwards, attention will likely be on the Bank of Japan’s monetary policies when the side effects of negative interest rates come to the fore.

In the 23/12 issue, we will be covering Yokohama Reito (2874), Kobe Bussan (3038), TerraSky (3915), PARK24 (4666), Isuzu Motors (7202) and Mitsubishi Estate (8802).

・Established in 1948. Carries out the chilled / frozen storage business involving seafood / agricultural and livestock products, etc., the food products retail business involving processing, retail, import and export, etc. and real estate leasing, etc. Owns a distribution centre in Yokohama and Osaka (Yumeshima), which is a proposed site for the IR.

・For FY2019/9 results announced on 14/11, net sales decreased by 18.5% to 139.979 billion yen compared to the previous period (93.3% compared to the plan) and operating income decreased by 1.1% to 4.774 billion yen (81.7% compared to the plan). Despite an increase in both sales and profit in their cold storage warehouse business due to operations proceeding smoothly in the distribution centre newly built last year, the decrease in both income and profit in seafood products in the food products retail business has affected.

・For its FY2020/9 plan, net sales is expected to decrease by 2.2% to 143 billion yen compared to the previous year and operating income to increase by 13.1% to 5.4 billion yen. While pork and beef imports are soaring from lower tariffs due to the TPP and EPA coming into effect, slow domestic consumption of livestock products have led to warehouses storing chilled / frozen import food products being filled to the brim across the country. In addition, concerns on the spread of the ASF infection in China is spurring an increase in imports, therefore, an increase in revenue from storage fees / stevedorage is predicted.

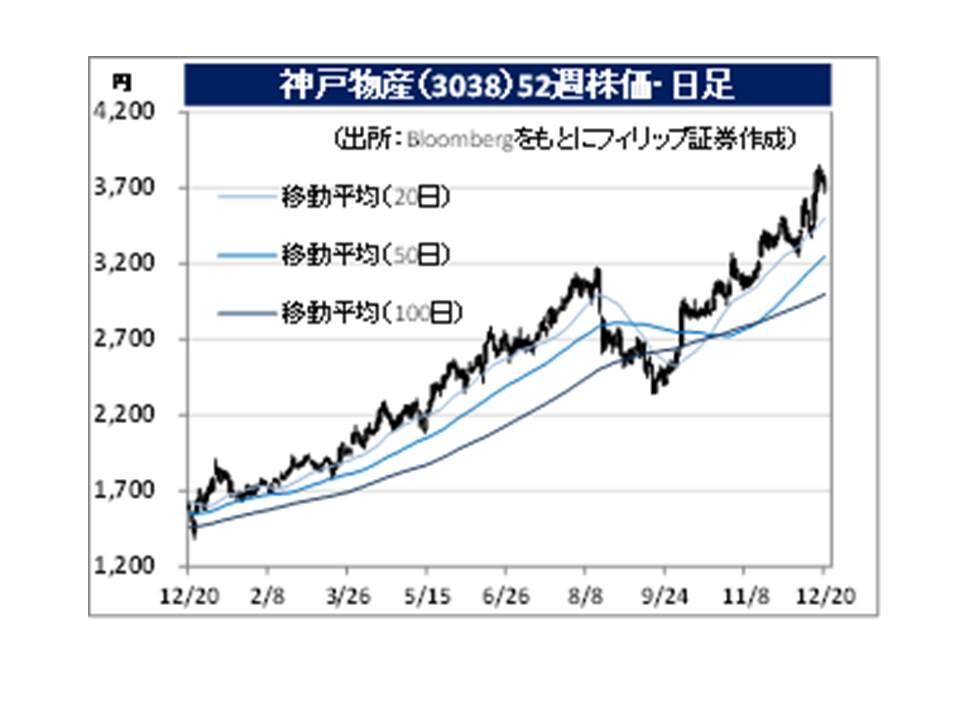

・Established in 1981. Carries out the manufacture, wholesale and retail of industrial use foodstuffs, etc. Expands the foodstuff supermarket “Gyomu Super”, which targets industrial-use customers via the franchise method. Also manages ready-made meals and food service chains such as “Kobe Cook World Buffet”, “Green’s K” and “Green’s K Teppanyaki Buffet”, etc. as well as renewable energy, etc.

・For FY2019/10 results announced on 13/12, net sales increased by 12.1% to 299.616 billion yen compared to the previous period, operating income increased by 22.4% to 19.239 billion yen and net income increased by 16.3% to 12.056 billion yen. Company has been working towards reinforcing their domestic group factories and their own import products, etc. and is focusing their efforts on developing PB products. Their PB products being featured in the media have also led to an increase in customers.

・For its FY2020/10 plan announced together with FY2019/10, net sales is expected to increase by 4.1% to 311.8 billion yen compared to the previous year, operating income to increase by 5.5% to 20.3 billion yen and net income to increase by 10.3% to 13.3 billion yen. Company also newly announced their 3-year plan from FY2020/10 to FY2022/10. FY2022/10 target net sales is at 346.7 billion yen and operating income at 23 billion yen.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: