|

Report type: Weekly Strategy

|

Will There Be a Paradigm Shift in Japanese Equity Investment?

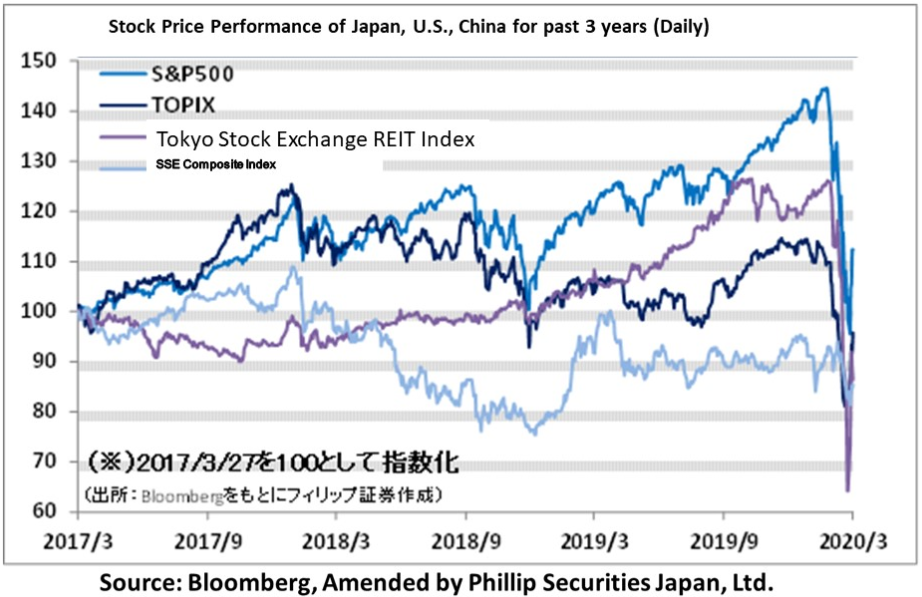

Additional monetary easing measures announced by the BOJ on 16/3 are having an impact on the stock market. The Nikkei Average started reversing after falling to 16,358 points on 19/3, and rose 19.6% to 19,564 points on 25/3. Until 13/3, the BOJ’s daily EFT purchases this month had been 100.2 billion yen, but these increased to 120.4 billion yen on 17/3, and 200.4 billion yen after 19/3. According to disclosures from the BOJ, out of the annual ETF purchase target of 6.0 trillion yen from 2018/8 onwards, TOPIX-related purchases were 4.2 trillion yen and the three indices-related purchases (TOPIX, Nikkei 225 and JPX Nikkei 400) were 1.5 trillion yen in proportion to each of the index. Approximately 80% were for TOPIX-related purchases. If the purchase target were doubled using the same calculation method, about 9.6 trillion yen out of 12.0 trillion yen per year will be geared towards TOPIX-related ETF purchases.

TOPIX is an index composed of the stocks of about 2,000 companies listed on the First Section of the TSE, and composition ratio is determined by the size of each company’s market capitalization. On the other hand, the Nikkei Stock Average consists of 225 stocks, and is a stock price averaged over these 225 stocks after adjusting for the effects of stock splits/consolidation and replacement of stocks adopted. In terms of constituent stocks, TOPIX consists of stocks with large market capitalizations, and is relatively susceptible to stocks closely connected with domestic demands. On the other hand, the Nikkei Average consists of high-tech and export-oriented stocks that are susceptible to overseas economic and exchange rate fluctuations.

As the globalization of the economy progresses, factors such as the expansion of the global economy centered on the US, the yen depreciation together with the strengthening of the US dollar, have improved the outlook for high-tech and export-oriented stocks. In the process, this tended to raise the Nikkei Average as a result. Typically, higher oil prices coupled with a weak yen would reduce domestic consumption due to rising import costs. Even more so, these factors would also apply for Japanese equity investment if they imply a strong global economy.

However, if the spread of Covid-19 halts the movements of people and goods and the global economy malfunctions as a result, it is likely that domestic demand, especially consumption, will increase in importance for an economy. Lower oil prices and a stronger yen are more desirable from the perspective of boosting domestic demand. As the doubling of the BOJ’s ETF purchase target increases the importance of equities with domestic demands in the Japanese stock market, NYMEX’s WTI crude futures price fell 70% from a high of 65.65 dollars per barrel on 8/1 to 19.46 dollars per barrel on 20/3. Oil price depreciation might be a negative factor for a global economy in which high-tech/export-oriented stocks are important, but there may be room to consider it as a positive factor for future Japanese equity investments.

In the 30/3 issue, we will be covering Raito Kogyo (1926), Itochu-Shokuhin (2692), GLP J-REIT (3281), and Japan Securities Finance (8511).

・Established in Sendai in 1948. Company engages in civil engineering work with a reputation for its technical capabilities (slope and slope stabilization work, foundation and ground improvement work, repair and reinforcement work, and environmental restoration work), general civil work and construction and other related works.

・For 3Q (Apr-Dec) results of FY2020/3 announced on 6/2, net sales increased by 2.2% to 74.81 billion yen compared to the same period the previous year, and operating income decreased by 3.4% to 6.589 billion yen. Increased orders from government agencies for construction work on slopes and slope stabilization, as well as restoration works arising out of natural disasters that occurred frequently in the previous fiscal year, together with the smooth progress of these works, had contributed to increase in sales. However, operating income decreased due to an increase in SG&A expenses.

・For its full year plan, net sales is expected to increase by 0.2% to 103.0 billion yen compared to the previous year, and operating income to increase by 1.0% to 9.8 billion yen. 2020 is the final year of the “Three-year Emergency Measures for Disaster Prevention, Mitigation and National Resilience”. On top of that, the business scale of recovery and reconstruction from disasters determined in the economic measures by the Cabinet in 2019/12 is about 7 trillion yen. This is a seasonal stock of which the stock price tends to rise during times of natural disasters. Indeed, the saying “Buy a straw hat while in winter” may be a useful reminder here.

・Established in 1918. Formed a capital and business alliance with Itochu Corp (8001) in 1982, with Itochu Corp currently holding 50.7%. Wholesale of liquors and foods in the Food Wholesale Business, and storage and transport of these goods in related businesses.

・For 3Q (Apr-Dec) results of FY2020/3 announced on 30/1, net sales decreased by 1.8% to 518.628 billion yen compared to the same period the previous year, and operating income decreased by 6.8% to 3.643 billion yen. Despite an increase in transactions through deeper business dealings with organized retailers, finally sales declined mainly due to sluggish beer sales. SG&A expenses fell 3.4% YoY, but profits declined due to a decrease in gross profit.

・For its full year plan, net sales is expected to increase by 4.9% to 700.0 billion yen compared to the previous year, and operating income to increase by 16.3% to 4.7 billion yen. Company is working with Confex Holdings, a confectionery wholesaler, and investing in Prima Meat Packers (2281), to expand and deepen its existing core businesses. In response to the spread of Covid-19, the Tokyo Metropolitan Government has called residents to refrain from going out unnecessarily on weekends as well as on weekday nights. There may therefore be concerns about hoarding of food and goods.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: