Report type: Weekly Strategy

Will the Stimulus Package Save the Japanese Economy in 2020?

On 5/12, the Cabinet approved a stimulus package involving a fiscal expenditure of 13.2 trillion yen from the country and its regions. Added with the expenditure from the private sector, the scale of the project comes up to 26 trillion yen, and within fiscal expenditure, public investment accounts for about 6 trillion yen. Although we ought to emphasise on a policy which will prepare for risks of an economic downturn and lead to economic growth after the Tokyo Olympics, with concerns on personal consumption after the consumption tax hike, would it actually be able to save the Japanese economy?

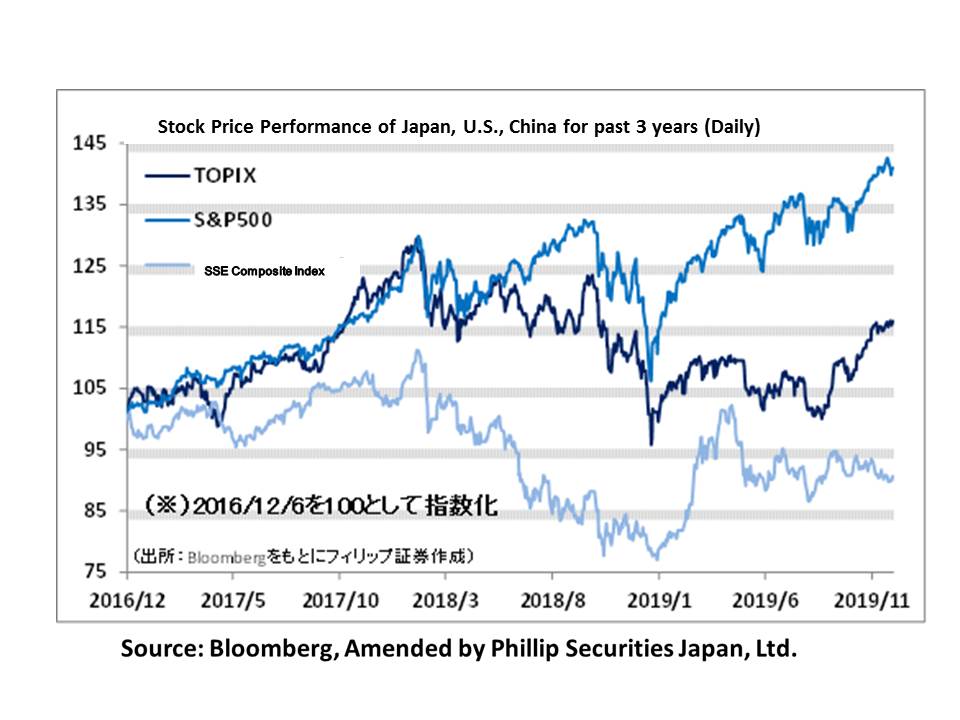

For the Japanese economy in the week of 2/12, as a result of November’s Purchasing Managers’ Index (PMI) announced on 30/11 by the National Bureau of Statistics of China going against market predictions to exceed 50 which was last seen 7 months ago, as well as the PMI for the private sector announced on 2/12 at 51.8, which was at a high level last seen since Dec 2016, on 2/12, the Nikkei average rose to exceed 23,500 points. However, due to growing uncertainty on the future as a result of US President Trump’s statement on 3/12 that “he liked the idea of waiting until after the presidential election for the China deal”, as well as the announcement of additional sanctions of tariffs on South American steel, etc., on 4/12, the Nikkei average fell to 23,044 points. Following which, expectations towards the US-China agreement began to rise once again, and it rebounded to 23,412 points on 5/12.

The three pillars of the stimulus package approved by the Cabinet are as follows: ① The recovery / restoration and to ensure safety / security from disasters” due to the series of natural disasters suffered, by reinforcing river banks that have a high risk of flood occurrences, as well as to eliminate utility poles on roads in urban areas which are used for transport in times of emergency. Since we are unable to know when disasters will strike and there has been a trend in their growing scale year after year, we can expect demand to be brought forward as well as long-term demand. ② Support towards “overcoming risks of an economic downturn” via a measure which mainly targets small and medium sized enterprises / small businesses by incorporating subsidies to promote an improvement in productivity, such as through digitalisation. Although there has already been an increasing trend in investments for improved work efficiency and labour-saving in small and medium-sized enterprises whom have adopted a “work style reform”, it is predicted that it will require prolonged efforts for its benefits to be reflected in system or software development companies. ③ “To enhance and maintain economic vitality for a future beyond the Tokyo Olympics” such as by enabling all elementary and middle school students to use IT devices such as PCs by fiscal year 2023. Due to an increase in ICT demand in education and at the same time, a growing importance of security countermeasures, there will likely be room for the involvement of a wide variety of related industries.

From the aspect of corporate governance, there have also been stock price movements that have predicted the resolution of parent-subsidiary listings, and focus in the week of 2/12 has been on Fujitsu (6702) group. There is a need to continue to keep an eye on corporate groups that have parent-subsidiary listing.

In the 9/12 issue, we will be covering Racoon Holdings (3031), Taiko Pharmaceutical (4574), Murata Manufacturing (6981), AEON (8267), Tokyo Rakutenchi (8842) and NTT Data (9613).

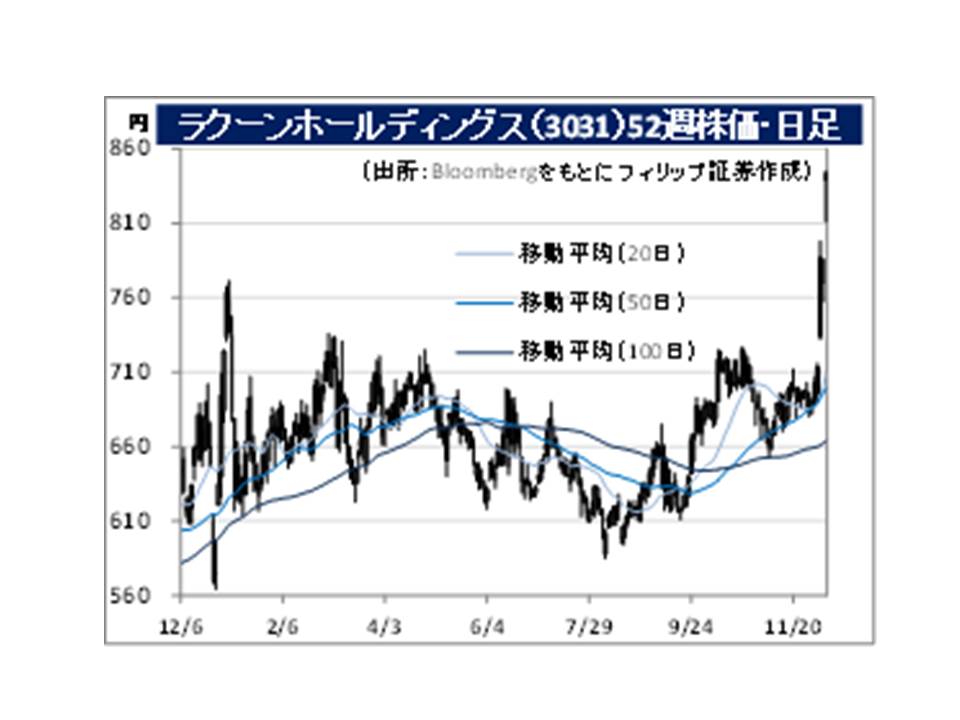

・Founded in 1993. Creates and provides new infrastructure in B2B transactions. Expands a cloud-based ordering system which performs the integrated management of placing and receiving orders for B2B transactions and the operation of B2B transaction sites involving apparel / miscellaneous goods, agency work for the payment and collection of payments that incur in B2B transactions, as well as accounts receivable / commercial rent guarantee services, etc.

・For 1H (May-Oct) results of FY2020/4 announced on 5/12, net sales increased by 23.4% to 1.667 billion yen compared to the same period the previous year, operating income increased by 34.8% to 365 million yen and net income increased by 30.1% to 236 million yen. There was significant growth in the distribution amount of business operators other than retail in the wholesale / supply site, “Super Delivery”. The start of product supply to Amazon Fashion has also contributed.

・For its full year plan, net sales is expected to increase by 15.8% to 3.45 billion yen compared to the previous year and net income to increase by 12.0% to 425 million yen. The content announced on 13/6 remains unchanged. In Super Delivery, they have begun dealing with tools such as DIY supplies and carpenter’s tools from October. Furthermore, the launch of advertisements geared at companies exhibiting their products have also contributed, and their product listing has exceeded 1 million.

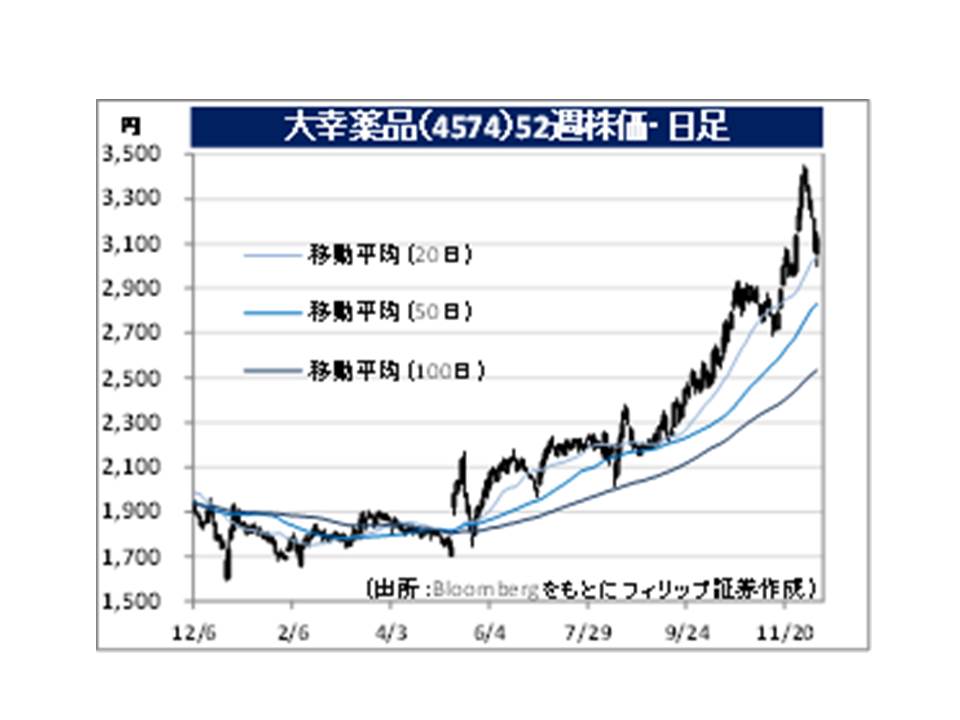

・Established in 1946. Succeeded the manufacturing and retail rights of Chuyu Seirogan (currently “Seirogan”). Expands 3 businesses, which are “Pharmaceuticals”, which carry out the manufacture and retail of general pharmaceuticals, “Infection Management”, which utilises patented technology involving chlorine dioxide gas, and “Others”.

・For 1H (Apr-Sep) results of FY2020/3 announced on 8/11, net sales increased by 14.6% to 4.385 billion yen compared to the same period the previous year and operating income increased by 52.3% to 980 million yen. Sales of the “Leave-on-type Cleverin” and “Cleve & And” in their infection management business have performed strongly. The 27.3% increase in net sales to 1.675 billion yen and the 2.8 times increase in segment profits to 434 million yen in this business have also contributed to an increase in both sales and profit.

・For its full year plan, net sales is expected to increase by 8.1% to 11.26 billion yen compared to the previous year and operating income to increase by 8.4% to 2.2 billion yen. Shipments in their pharmaceutical business for the Chinese market are planned to begin from Oct 2019. In addition, due to an increase in brand awareness from the marketing strategy to remove the “trumpet logo” in the infection management business, as well as a rise in demand for virus elimination / disinfectants such as influenza in the office, we can expect a sustained popularity for Cleverin.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: