Report type: Weekly Strategy

“Will Bank Stocks Take Center Stage in BOJ’s Monetary Easing Correction?”

At its monetary policy meeting held on 19-20/12, the BOJ decided to revise its easing policy on a large-scale, increasing the allowable range of fluctuations in long-term interest rates from around 0.25% to 0.5%. This is the first increase in the fluctuation range since March 2021, when it was raised from 0.2% to 0.25%. The policy framework for allowing long-term interest rates to fluctuate was introduced in September 2016 as “Quantitative and Qualitative Monetary Easing with Long- and Short-Term Interest Rate Control”, and at the same time, an “overshooting commitment” was also introduced to continue monetary easing even if 2% inflation is reached over several months on a historical basis, while allowing some upward swing in inflation. As far back as January 2016, “Quantitative and Qualitative Monetary Easing with Negative Interest Rates” was introduced, which applied a negative interest rate of -0.1% to a portion of BOJ current accounts held by financial institutions.

If short-term interest rates remain unchanged and long-term interest rates rise, this will directly affect the earnings of financial institutions, which will see their interest margins on deposits and loans expand. Asset management yields of insurance companies are also expected to improve. In fact, there is a correlation between the TOPIX bank stock index and the 10-year JGB yield, as shown in the section “Long-Term Interest Rates, Bank Stocks, and the Regional Bank System” below. The 10-year breakeven inflation rate, which represents the expected inflation rate for the next 10 years, has also been generally in the range of 0.8-1.0% since April of this year, and 0.5% is likely to be below actual levels. We should therefore pay attention to the fact that the expansion of the allowable range of long-term interest rate fluctuation in the near future may be abolished prematurely after the new BOJ governor assumes office. Essentially, unlike short-term policy rates, which can be controlled directly by the central bank, long-term interest rates should reflect the supply and demand in the bond market. If the bond market regains its original function, then there are possibilities of a further rise in long-term interest rates and an expansion of financial institution earnings.

If risk tolerance for lending increases as earnings of financial institutions expand, capital investment may grow through credit expansion. In contrast to the current US and European markets, where a “reverse yield”, with long-term interest rates being lower than short-term rates, is said to be a sign of economic recession, in Japan, the “forward yield”, or the gap when long-term interest rates exceed short-term rates, is expanding, which should raise expectations that it will lead to economic expansion. However, a rise in long-term interest rates in Japan is likely to be reflected in a stronger yen in the foreign exchange market. Even when long-term interest rates rose from 2003 to 2006, the dollar-yen exchange rate appreciated from the 120-yen per dollar level at the beginning of 2003 to the 101-yen per dollar level by the end of 2004.

In relation to the “2024 logistics problem” deadline (1st April, 2024), the response to the transportation capacity shortage is expected to be through unmanned delivery by drones as well as automated driving. The ban on “Level 4” permits, which are for fully-automated driving under specific conditions such as driving routes, is scheduled to be lifted on 1st April next year.

In the 26/12 issue, we will be covering AISAN Technology (4667), Future Corp (4722), Chubu Steel Plate (5461) and Japan Post Insurance (7181).

AISAN Technology Co., Ltd (4667) 1,516 yen (23/12 closing price) ※TSE Standard Stock

・Established in 1970. Main business is the development and sales of its own software for the surveying and civil engineering construction industries. Operates a Public Sector segment for the surveying and real estate market and a Mobility segment related to automobiles and MaaS. Strengthening automatic driving-related products.

・For 1H (Apr-Sep) results of FY2023/3 announced on 9/11, net sales decreased by 10.2% to 1.76 billion yen compared to the same period the previous year, and operating income decreased by 45.6% to 72 million yen. Sales by business segment were down 3.1% YoY to 1.369 billion yen in the Public Sector segment and down 29.0% YoY to 385 million yen in Mobility. Many projects require time from order receipt to delivery, and profits are expected to be recorded in the October-December period and beyond.

・For its full year plan, net sales is expected to increase by 9.8% to 4.6 billion yen compared to the previous year, operating income to increase by 24.3% to 320 million yen, and annual dividend to increase by 1 yen to 14 yen. In June, a joint development agreement was signed with Tokai Rika, a Toyota-affiliated parts manufacturer, for a remote monitoring and operation system for automated vehicles, and in August, a collaboration agreement was signed for the introduction of automated buses between JR Komatsu Station and Komatsu Airport. A 3D map verification experiment for setting the travel route of an automated vehicle was also conducted from 28/10-6/11.

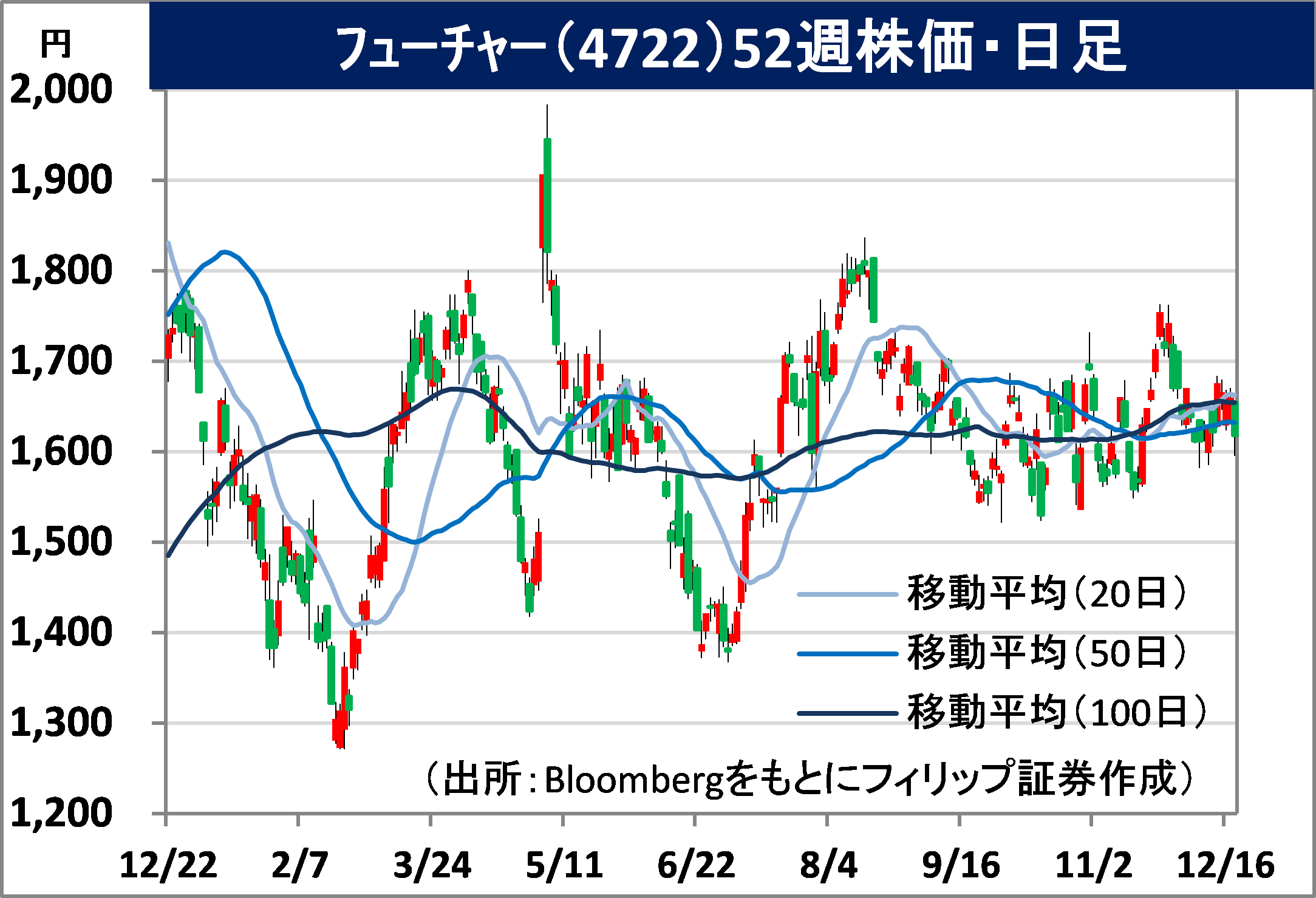

Future Corp (4722) 1,640 yen (23/12 closing price)

・Established in 1989. Mainly involved in the digital transformation (DX) of client companies, focusing on business systems, and also operates an IT Consulting & Services business as well as a business innovation business.

・For 9M (Jan-Sep) results of FY2022/12 announced on 26/10, net sales increased by 10.7% to 39.614 billion yen compared to the same period the previous year, and operating income increased by 43.0% to 9.361 billion yen. The IT Consulting and Services business, which accounts for 85% of total sales, saw steady progress in large-scale projects from a wide range of client companies that contribute to strategic, medium- to long-term growth, resulting in a 60% increase in operating income YoY.

・For its full year plan, net sales is expected to increase by 14.0% to 55.5 billion yen compared to the previous year, operating income to increase by 33.3% to 12.0 billion yen, and annual dividend to increase by 8.5 yen to 34 yen after adjusting for stock split. Future Architect, a subsidiary, introduced “FutureBANK”, a loan support system, to a number of member banks of the “TUBASA Alliance”, a framework for wide-area collaboration involving 10 regional banks, including Chiba Bank. A project to introduce next-generation banking for regional financial institutions is currently underway.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: