Report type: Weekly Strategy

Value Stocks May Appear in the Gap Between Zero and Negative

Right before the Bank of Japan’s Monetary Policy Meeting on 19/9, it was found that President Hashimoto of Sumitomo Mitsui Trust Bank had thoughts of introducing “account maintenance fees” if the Bank of Japan decides to go ahead with deeper “negative interest rates” as an additional monetary easing policy, which will charge a 0.1% annual handling fee when money is deposited from private banks. Within those that account for more than half of the cash and deposits under individual financial assets, there would be many people, especially those in the elderly generation, who have the stable-minded values of “As long as it doesn’t decrease, I don’t mind if there is zero interest”. Within those, as a result of the opinion of “If my deposit decreases, that’s a different story”, we cannot deny the possibility of a structural change occurring where it shifts from cash and deposits to other assets.

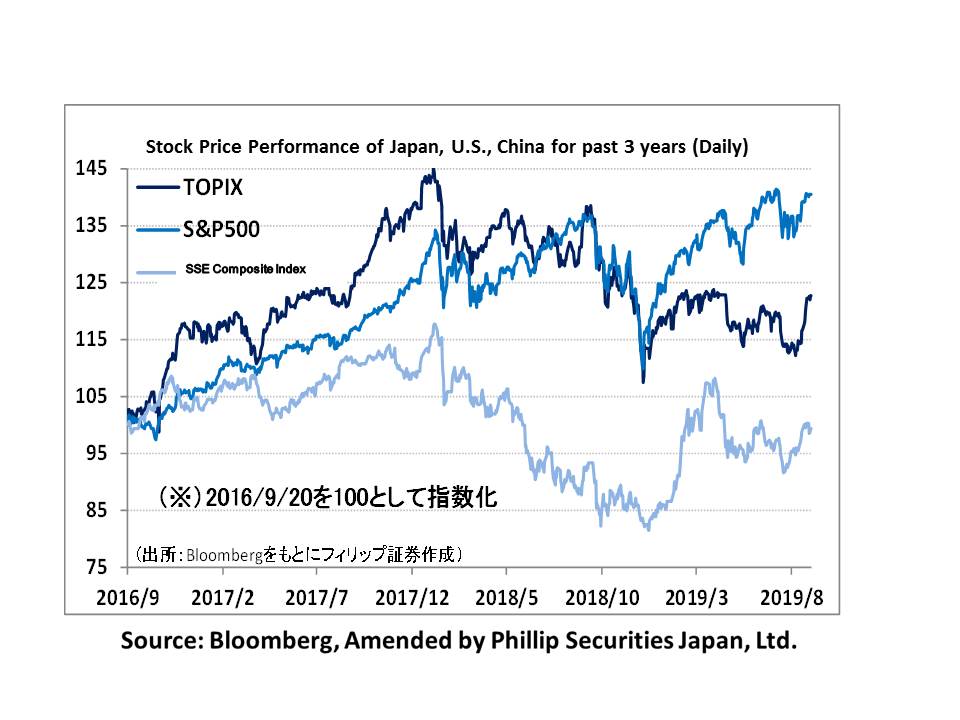

For the Japanese stock market in the week of 17/9, regarding the drone attack on major Saudi Arabian oil facilities on 14/9, as a response towards global crude oil supply concerns, it was reported that there were predictions to recover their production capacity prior to the attack by end September, which saw the Nikkei average stock price exceeding 22,000 points on 17/9 and showing steady movements after. The 0.25% cut on the policy interest rate at the US FOMC on 18/9, along with the 0.3% cut on the interest rate for excess reverses by the FRB, and the display of the stance towards permitting asset growth were favoured. On the other hand, at the Bank of Japan’s Monetary Policy Meeting, it was decided that they would maintain the current monetary easing policy. Although they decided to hold on to their “additional easing card” based on the risk of a yen appreciation in the future, etc., as of end 7/2019, the Bank of Japan’s total assets grew to 5.23 trillion dollars, and in proportion to the GDP, the Bank of Japan is close to 100% compared to the FRB that is slightly under 20% and the ECB at about 40%. Due the current situation where it is difficult to further raise their total assets, there is less likelihood of a move towards additional monetary easing, and if the US and Europe continue with further monetary easing, it may also result in a situation where it could evoke a sharp rise in the value of the yen.

Based on these circumstances, if the stocks of companies that prioritise private investors, such as having shareholder benefits and which continue to stably pay out dividends every year, etc., were to become significantly lower than their “book value per share (BVPS)”, they may act as a recipient of the capital shift from cash and deposits. Although estimated profits of companies fluctuate easily, as long as the net assets, which are the shareholder value, do not create a deficit, they have the tendency to increase year after year without decreasing. Based on that, from the aspect of the stability of undervalued stock prices, we can say that low PBR value stocks are superior to low PER stocks. However, companies with many fixed assets could also factor in impairment risk, etc., hence, there is also a need to keep an eye on low PBR stocks.

In the 24/9 issue, we will be covering Kuraray (3405), Infocom (4348), Strike (6196), Ferrotec HD (6890), Japan Securities Finance (8511) and Square Enix HD (9684).

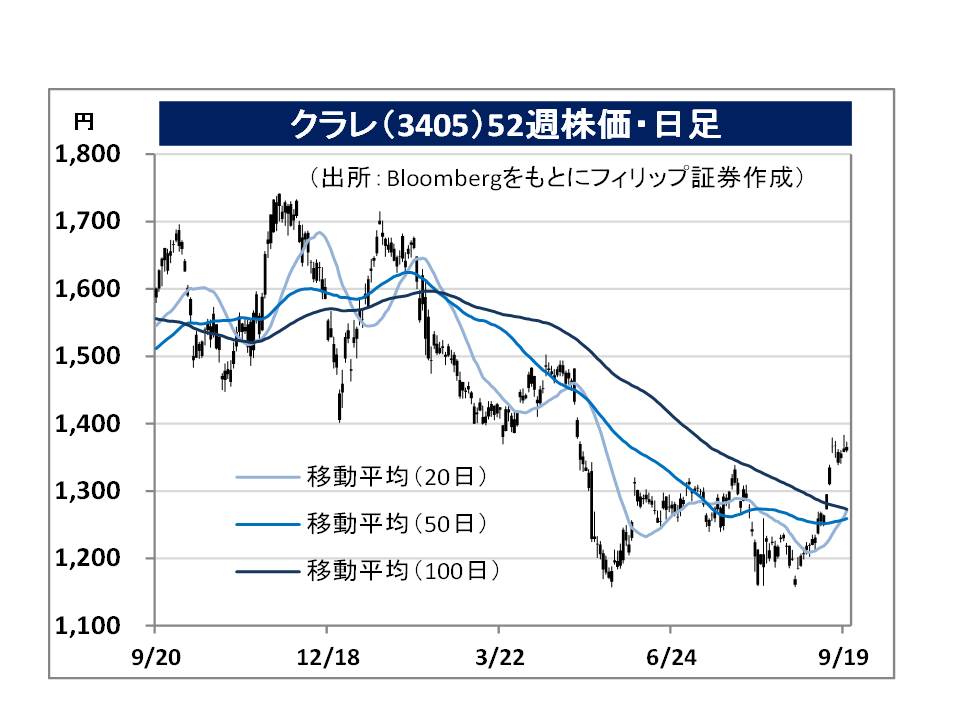

・Established in 1926 for the purpose of commercialising rayon. Handles Poval and EVOH resin / film, isoprene chemicals / fine chemicals, heat-resistant polyamide resin, thermoplastic elastomers, metacrylic resin, carbon materials, and vinylon / artificial leather, etc. Has the top shares worldwide for Eval and the Poval film for optical use.

・For 1H (Jan-Jun) results of FY2019/12 announced on 8/8, net sales decreased by 4.6% to 287.419 billion yen compared to the same period the previous year, operating income decreased by 23.0% to 27.921 billion yen, and net income decreased by 41.3% to 13.254 billion yen. Sales volume for Poval resin has decreased due to the economic slowdown. EVOH resin used for automobile petrol tanks have also been affected by the decrease in the number of automobile production units.

・For its full year plan, net sales is expected to decrease by 0.5% to 600 billion yen compared to the previous year, operating income to increase by 1.8% to 67 billion yen, and net income to increase by 13.2% to 38 billion yen. According to Nikkei, Inc., it was reported on 19/9 that the company plans to raise net sales of their biodegradable plastics business to 100 million dollars in 2026, which is 5 times that of the forecast in 2019.

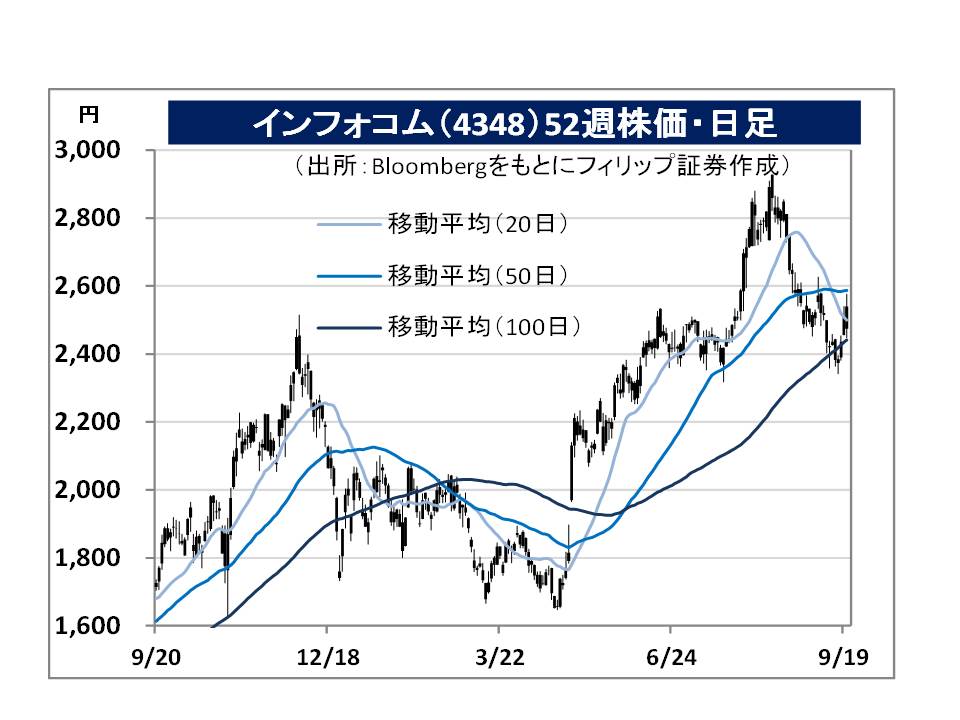

・Established in 1983 as a subsidiary of Nissho Iwai. Offers IT services such as the planning, development, operation and management, etc. of information systems for companies, pharmaceutical / medical institutions, nursing care operators and public and educational research institutions. Also handles Japan’s largest digital comic distribution service, “Mecha Comic”, in addition to the distribution service of digital contents.

・For 1Q (Apr-Jun) results of FY2020/3 announced on 30/7, net sales increased by 21.2% to 12.687 billion yen compared to the same period the previous year, operating income increased by 83.1% to 1.24 billion yen, and net income increased by 79.4% to 859 million yen. Their digital comic distribution service has performed strongly. Advertising reinforcements in June, such as their first TV commercial and the seat advertisements in Meiji Jingu Stadium have contributed.

・For its full year plan, net sales is expected to increase by 10.2% to 57 billion yen compared to the previous year, operating income to increase by 13.2% to 7.8 billion yen, and net income to increase by 8.7% to 5.2 billion yen. Within the company’s subsidiary, GRANDIT, which carries out the development and retail of complete Web-ERP, began offering Amazon Web Services (AWS) in addition to Microsoft Azure as a cloud platform on 13/9.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: