Report type: Weekly Strategy

Things to Consider in the Midst of the COVID-19 Market Situation

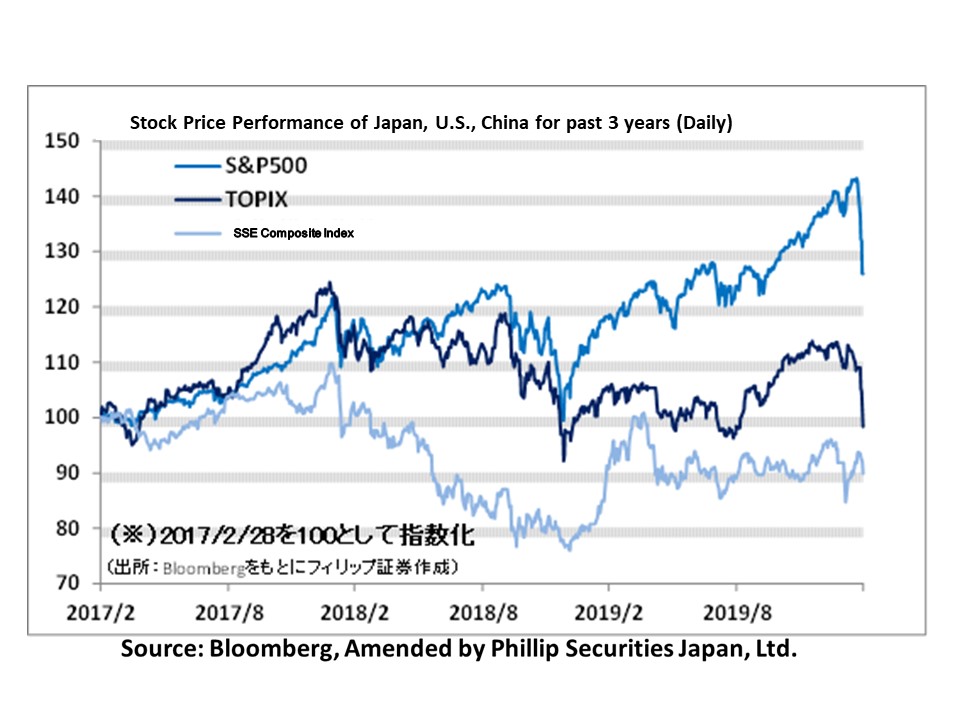

COVID-19 infection has spread to the US, and US stocks, which until recently had been performing solidly, plunged, thereby also inducing a big plunge in the Japanese stock market. On 27/2, PM Abe made an unusual request for elementary, junior and senior high schools nationwide to close simultaneously from 2/3. On 28/2, the Nikkei Average fell from the previous day’s closing of 21,948 points to below 21,000 points. On 28/2, the Nikkei Average volatility index (an index showing investors’ expectations of future fluctuations in the Nikkei Average) came within the 40% range since 2016/1 when it was shaken by the China shock. The approximate value of the Nikkei Average weighted average BPS (Book-value Per Share) considering market capitalization and equity capital was 20,738 points at the closing price on 27/2. This is approaching the 1.0 times weighted average PBR (Price Book-value Ratio) attained on 26/12/2018 and 16/8/2019. A weighted average PBR at closing price of below 0.99 times will be a first since 21/11/2012, before the inauguration of the second Abe administration. The Nikkei Average closing price at that time was 9,222 points (the approximate weighted average BPS was 9,507 points), meaning that the net assets of the Nikkei Average stocks had increased 2.2 times over a period of 7 years and 3 months. Normally, if net profits are not in the red, net assets are expected to increase even if profits were to decrease. We need to stay cool and consider whether the impact of COVID-19 is so great or not that the corporate profits of the Nikkei 225 leading Japanese companies will turn red on average.

It has been reported that the number of new infected and deceased people in China has been increasing at a slower pace since mid-February. As a result, the number of new infections worldwide between 25-27/2 had been 1,429, 1,093 and 637, while the number of new deaths during the same period had been 36, 40 and 13 people, with both showing decreasing trends. Despite criticism of the surveillance system from a human rights perspective, it appears that China has achieved some success in containing the spread of infection through the usage of the latest acquired big data technology. In addition, we are also seeing efforts to develop therapeutics to counter COVID-19 from drugs treating Ebola hemorrhagic fever, influenza and HIV. On 27/2, Director General Tedros of the World Health Organization (WHO) warned that all nations must “prepare for everything” in order to avoid pandemics, and advocated the securing of medical equipment, training of medical personnel and tests at airports and borders. Therefore, investment sentiments for the time being shall most likely be centering on stocks related to securing of medical equipment, and those involved with testing equipment used for the detection of infections.

In the 2/3 issue, we will be covering Teikoku Sen-I (3302), Healthcare & Medical Investment Corp (3455), Nissui Pharmaceutical (4550), and INES (9742).

・Founded in 1887 and established in 1907 by Teikoku Seima, its predecessor. Major business segments include the Disaster Prevention & Preparedness Business, which deals with various types of fire hoses, disaster prevention equipment, search equipment and alarms, and the Textile Business which deals with hemp and functional fibers.

・For FY2019/12 results announced on 14/2, net sales increased by 19.3% to 35.393 billion yen compared to the previous year, and operating income increased by 25.4% to 5.612 billion yen. Sales of the Disaster Prevention & Preparedness Business increased 31.4% to 28.235 billion yen, contributing to increased sales and profit. In addition to the expansion in sales of large-scale disaster prevention materials and security equipment for airports, sales of rescue work vehicles and airport chemical fire trucks were also firm.

・For its FY2020/12 plan, net sales is expected to decrease by 9.6% to 32.0 billion yen, and operating income to decrease by 34.1% to 3.7 billion yen. There is a consideration for a decline due to a temporary upside in the initial plan for the previous fiscal year (net sales of 30.0 billion yen and operating income of 45.0 billion yen). In addition to sales expansion of large-scale water supply and drainage systems for flood-related social problems, the products of the Disaster Prevention & Preparedness Business, namely pandemic (new infectious diseases)-related products as well as products for decontamination outside hospitals, that cater to prevention of the spread of COVID-19 deserve our attention.

・A healthcare-focused J-REIT that has Sumitomo Mitsui Banking Corp and NEC Capital Solutions as major sponsors in addition to Ship Healthcare Holdings, which engages in the nursing care business. Acquired a J-REIT-first hospital asset in 2017/11.

・For the FY2019/7 (Feb-July) results announced on 13/9, operating revenue increased by 54.4% to 2.008 billion yen compared to the previous period (FY2019/1), operating income increased by 83.9% to 1.189 billion yen and distribution per unit including excess profit was 3,643 yen (distribution in excess of profit per unit was 318 yen). Acquired 8 properties in 2019/2 for a total acquisition price of 22.691 billion yen. Has a total of 35 properties at end of fiscal year.

・For FY2020/1 plan, operating revenue is expected to increase by 0.2% to 2.012 billion yen compared to the previous period (FY2019/7), operating income to decrease by 7.4% to 1.101 billion yen, and distribution per unit including excess profit to decrease by 8.3% to 3,304 yen. The annual distribution yield (based on the closing price on 27/2) based on the company forecast for FY2020/7 is 4.83%. With the ageing of society and the declining population providing nursing care, it is expected that more healthcare facilities will need to be established and society’s demand for nursing care and medical services will increase.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: