Report type: Weekly Strategy

“The ‘Twisted Parliament’ in the U.S. Bringing About an Appreciation of the Yen Against the Dollar”

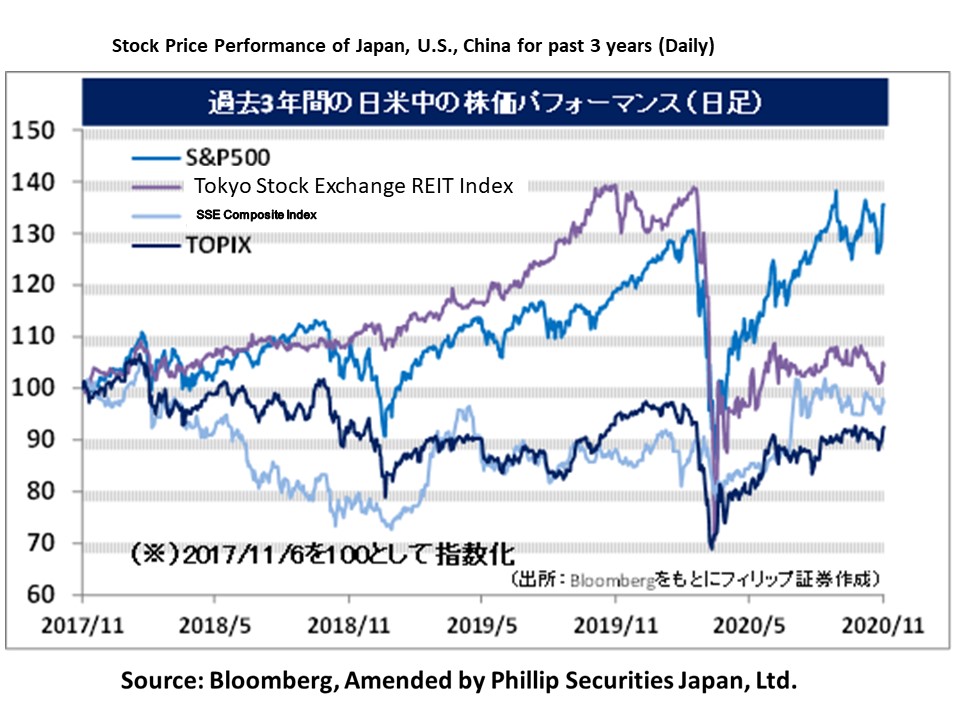

Although presently the results of the U.S. presidential and parliamentary elections which took place on 3/11 have not been confirmed, the global stock market saw an acceleration of risk-on movements at once under the prediction of a “twisted parliament”, where Biden is elected and there is a majority of the Senate from the Republican Party and a majority of the House of Representatives from the Democratic Party. The Nikkei average, which saw a growing standstill at the 23,000 point level from June onwards, hit over 24,000 points on 5/11 last seen in Jan this year, and marked the 24,300 point level on 6/11 last seen in Oct 2018. With movements focusing on the 22,000 point level throughout May to Sep 2018 without exceeding close to 23,000 points, these movements appear to be a turn of events similar to the time where there was an accelerated rise in market price after exceeding 23,000 points in mid Sep up to the 24,400 point level in early Oct. We can presume that the accumulation of short positions focusing on futures within a narrow boxed market and the market exceeding the upper limit of the range could invoke a short squeeze of cutting losses and easily cause an accelerated increase in market price.

Prior to the U.S. presidential election, if it were to result in a “blue wave” where the Democratic Party holds a majority of the Senate and the House of Representatives involving the parliament and the president, there was the likely scenario where we could expect an increase in the U.S. long term interest rate and economic expansion following increased large-scale government spending towards economic policies, in addition to the monetary easing by the Fed thus far. In contrast, the scenario where there is an increase in the U.S. long term interest rate following an expansion in the scale of government spending has become less likely due to the Republican Party holding a majority of the Senate. According to the “Mundell-Fleming model” in macroeconomics, an increase in the long term interest rate following an expansion of government spending under a floating exchange rate system is said to be a factor for high home currency due to it attracting money that demands high interest rates. In other words, while the sudden depreciation of the dollar was being held back due to the offset of the factor for a depreciation of the dollar from monetary easing by the Fed under

the blue wave by the factor for an appreciation of the dollar from increased government spending, because of the appearance of the prediction that the Republican Party would hold the majority of the Senate, it is suggested that loss of the factor for the appreciation of the dollar would easily lead to an advancement in the depreciation of the dollar in one go. This can be said to be a major factor for the advancement of the appreciation of the yen against the dollar to the 103 yen level which occurred after overseas markets on 5/11.

This advancement in the appreciation of the yen against the dollar appears to be different from the appreciation of the yen as a form of escape to risk-free assets when there is a decrease in risk appetite. Under the Abe administration, the depreciation of the yen following unprecedented monetary easing by the Bank of Japan pushed up the earnings of Japanese export corporations and international blue-chip corporations. Perhaps this time it would be the turn to expect a similar increase in earnings in U.S. corporations through monetary easing by the Fed. On the other hand, for Japanese corporations, if they are able to enjoy lower raw material and energy costs due cheaper crude oil in addition to the appreciation of the yen against the dollar, we can presume that it would be easier than ever to raise earnings.

In the 9/11 issue, we will be covering Enigmo (3665), Maruyama Mfg. (6316), Hitachi (6501), and Yamaha Motor (7272).

・Established in 2004. Operates the social shopping site, “BUYMA”, which enables the retail of and putting up popular items for sale locally by Japanese residing overseas and who register as a personal shopper. Sony (6758) is their principal shareholder.

・For 1H (Feb-Jul) results of FY2021/1 announced on 14/9, net sales increased by 10.0% to 2.964 billion yen compared to the same period the previous year and operating income decreased by 0.5% to 1.127 billion yen. Due to the promotion of an early switch to private international distribution services in response to temporary delivery suspensions and delays following city lockdowns in various overseas countries due to the COVID-19 catastrophe, they were able to limit the negative impact on their services to a minimum.

・Their full year plan is unannounced due to the difficulty in reasonably calculating the impact of the COVID-19 catastrophe. As a growth strategy for BUYMA, they are currently promoting a reinforcement to their selection of goods by collaborating with corporate sellers such as overseas specialty shops, and expanding the English version of BUYMA. With self-restraint in going outdoors to continue due to the COVID-19 catastrophe, there has been an expansion in their user bracket such as in overseas users, etc., who began selling due to the implementation of telecommuting. There has also been increased diversification in products, such as furniture and interior, etc. due to the demand from staying at home.

・Established in 1937. Their main businesses are the manufacture and retail of agriculture and forestry machines (pest control machines, silvicultural machines, components, etc.), industrial machines and other machines (firefighting machines and others). Their mainstay, the pest control machines for farmers, account for about 70%.

・For 9M (2019/10-2020/6) results of FY2020/9 announced on 7/8, net sales decreased by 2.9% to 24.406 billion yen compared to the same period the previous year and operating income increased by 2.4 times to 591 million yen. Although there was an increase in demand for sprayers as a measure for COVID-19, the decrease in high-performance pest control machines for farmers following a self-restraint in business influenced the decrease in revenue. In terms of profit, they succeeded in cutting expenses which lead to an increase in profit.

・Company revised their full year plan downwards. Net sales is expected to decrease by 4.6% to 34.5 billion yen compared to the previous year (original plan 37 billion yen) and operating income to increase by 38.1% to 600 million yen (original plan 700 million yen). In the general policy speech by Prime Minister Suga held after the call for the extraordinary Diet session, the export value of agricultural products from Japan (900 billion in 2019) is targeted at 2 trillion yen in 2025 and 5 trillion yen in 2030. Towards achieving the target, here would be a need for increased efficiency in agricultural production, and we can likely expect an increase in demand to introduce machines for farmers.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: