Report type: Weekly Strategy

The True Value Lurking in Bargain Stocks

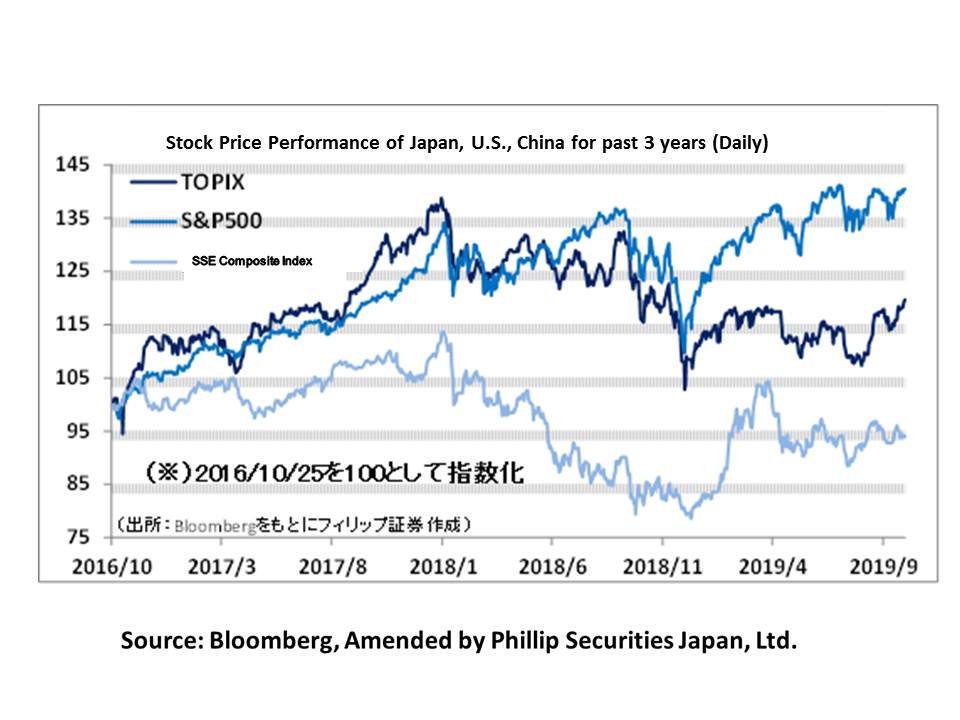

For the Japanese stock market during the week of 21/10, the “unsettled sales balance of arbitrage trading” related to “forward buying / long sales” positions was 1.5388 trillion yen (down 59.1 billion yen compared to the previous week) based on the date of 18/10. This was a solid development, considering the selling pressure from the record of 2.666 trillion yen as of the date of 6/9. Although there were negative factors resulting from the announcement of financial results for US semiconductor-related stocks and those with high sales ratio in China, the Nikkei Average bounced back after going below 22,500 points temporarily on 23/10 to reach the 22,800 points level on 25/10. However, trading was thin due to concerns ahead of full-scale announcements of financial results in the July-Sept period. In the final analysis, market development centered upon profit-taking of major semiconductor-related stocks that had risen in advance, and the buyback of shipping stocks and non-ferrous stocks where short sales by industry are high.

As a result of extensive damage brought about by Typhoon Hagibis (Typhoon 19), it was reported that five wards (Sumida, Koto, Adachi, Katsushika, Edogawa) in the Arakawa/Edogawa basin in Tokyo had temporarily considered large-scale evacuation including to regions outside Tokyo Prefecture. Since all the regular railway lines in the Tokyo metropolitan area had been suspended, in the end the advice for residents was suspended. Considering that the target number of residents is up to 2.5 million, issues like securing evacuation centers etc. had arisen, and it seems that issues relating to human life and protection of livelihood are beginning to be perceived as imminent and immediate problems confronting the Japanese populace.

The Japanese stock market is influenced by overseas activities, especially those of the US stock market. While the focus had been on IT-related stocks, those related to construction, civil engineering and other social infrastructure have generally been neglected in terms of PER (Price-to-Earnings Ratio) and PBR (Price-to-Book Ratio). Through changes in Japanese perception, investors are looking again at the true value of stocks engaging in businesses with high degrees of contribution to human life and protection of livelihood. We can therefore see the market trending towards investment in value stocks that are being more than just bargain stocks. Furthermore, we can expect investments in ESG (Environment / Society / Governance) stocks which are concentrating on “Climate Change Risks”, considered a common global problem, as well as availability of funds arising from the government’s supplementary budget.

It is not easy to realize “the true value lurking in bargain stocks” and this is a challenge for investors. There are many different themes and materials in the stock market, and it can be said that there are countless profit-generating opportunities depending on the timing of entry. Amongst these diversities, focusing on a particular stock, selecting a stock and deciding the amount to invest can indeed be said to be a demonstration of a person’s way of life.

In the 28/10 issue, we will be covering Hagoromo Foods (2831), Cybernet Systems (4312), Chugai Pharmaceutical (4519), Tokyo Steel Manufacturing (5423), Topcon (7732) and Matsuya Foods Holdings (9887).

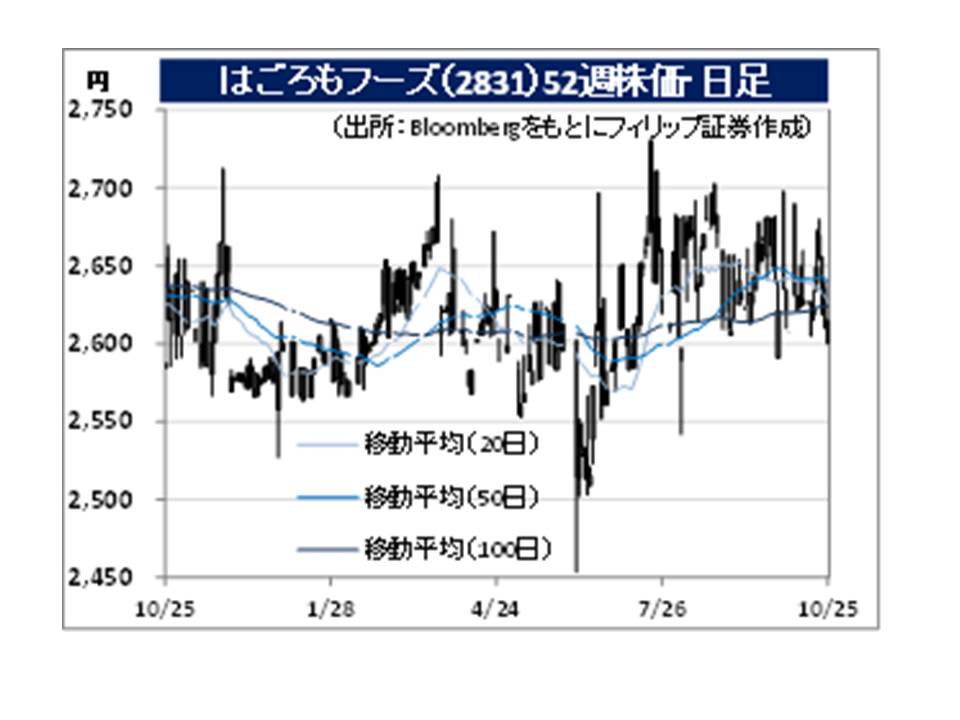

・Established in 1947 after founding the tuna canning business in 1931. Trademarked the “Sea Chicken” product name in 1958. Has the Food Business that manufactures and sells canned foods, pasta, packaged cooked rice, bonito shavings and seaweed.

・For 1Q (Apr-Jun) results of FY2020/3 announced on 14/8, net sales increased by 3.3% to 20.978 billion yen compared to the same period the previous year, and operating income increased by 8.5% to 703 million yen. Sales of mainstay tuna products, which account for 46% of sales, increased 8.5% YoY. Along with this, the strong sales of new products with high gross margin, and lowering of advertising expenses had contributed to increased sales and profits.

・For its full year plan, net sales is expected to increase by 0.6% to 80.4 billion yen compared to the previous year, and operating income to increase by 21.8% to 1.9 billion yen. Although there is a tendency for the boom in canned mackerel to push results positively, new products such as “oil-free sea chicken” that do not use oil are also selling well. The rise in price of longfin tunas, the main raw material, as a result of seawater temperature fluctuations has been absorbed by the price increase with effect from the 1/10 shipment. We can expect increased demand for canned food when evacuating during disasters. Let’s look forward to the performance of President Goto who assumed office on 15/10.

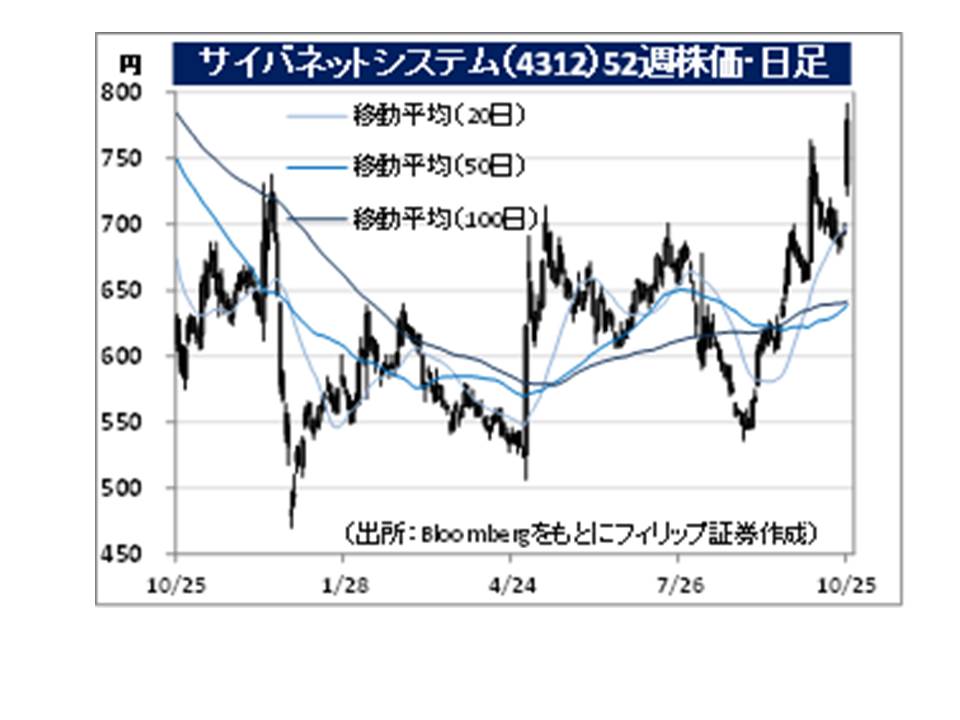

・Established in 1985 when the Japanese corporation of US Control Data Corp (CDC), a pioneer in supercomputers, established the cybernet service business as a separate company. Handles the Solutions Service Business through the provision of software and technical services. A leading company in CAE (Computer Aided Engineering).

・For 1H (Jan-Jun) results of FY2019/12 announced on 7/8, net sales increased by 9.8% to 11.798 billion yen compared to the same period the previous year, operating income increased by 55.0% to 1.624 billion yen, and net income increased by 10.1% to 1.049 billion yen. Both the CAE Solution Service and the IT Solution Service had performed well. The US development subsidiary and Asian sales subsidiaries had also been contributing to sales.

・Company has revised its full year forecast upwards on 24/10. Net sales is expected to increase by 8.0% to 21.3 billion yen compared to the previous year (original plan 20.0 billion yen), operating income to increase by 31.8% to 1.98 billion yen (original plan 1.52 billion yen), and current income to turn positive at 1.25 billion yen (original plan 958 million yen), against the loss of 656 million year the previous year. The annual dividend forecast is also increased from 15.38 yen to 20.06 yen.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: