The Reiwa Market Opens with the Risk of the US-China Cold War

What was waiting for the Japanese stock market beyond the 10-day holiday that brimmed with festive mood of the change in imperial era from Heisei to Reiwa, was President Trump’s twitter statement of a tariff increase on China, which served as a spark for a rough welcome of low stock prices and strong yen. After the Nikkei average fell below 22,000 points on 7/5, the first day after the holidays, on 9/5 it dropped under 21,500 points since 3/4. The dollar-yen market also shifted towards a strong yen (weak dollar) between 110 points from 8/5 onwards.

It is likely that the timing for the US tariff increase on China was carefully laid out by the Trump administration. First of all, the extent of the buying lead in the US stock market, such as the S&P 500 and NASDAQ renewing their highest records, etc., had leeway to allow for a fall in stock prices. Next, preliminary figures of the real GDP for the US’s Jan-Mar 2019 term announced on 26/4, along with the unemployment rate and increase in nonfarm payrolls in the US employement statistics for April announced on 3/5, indicated a strong trend in the US economy. Furthermore, US public opinion polls showed that President Trump’s approval ratings had hit its highest record. Taking these into consideration, even if the tariff increase were to pose a negative impact to its own economy, even more than that, it can be presumed that they prioritised the advantage of maintaining their own country’s economic supremacy while the vitality of the Chinese economy weakened. In this era of the new US-China cold war due to a “paradigm shift”, perhaps it is no longer possible to expect from the US the value of a US-China mutual prosperity (Win-Win) through cooperation.

However, although tariff increases on China were also imposed last year with the 1st round on 6/7, the 2nd round on 23/8 and the 3rd round on 24/9, looking at the Nikkei average, after it marked a low price of 21,574 points on 3/7, it rose to the high price of 24,448 points on 2/10. It would be too hasty to assume the view that future additional tariffs imposed on China would be directly linked to the fall in stock prices. Instead, for the time being, what we should be concerned about is the VIX Index’s (calculation based on the volatility of option transactions for the US S&P 500 index) selling on balance of futures which has hit a record high of more than 18,000 stocks as of 30/4, which has led to movements of a short-term reduction in positions from a “risk parity strategy” that will likely influence Japanese stocks.

For the investment of Japanese stocks in the era of the new US-China cold war, it will be increasingly important to choose a strategy between targeting mid and long-term domestic demand stocks that avoid “global economic risk” focusing on China, and back the government budget and system, or to aim for the rebound towards the buying of over-selling stocks which bear global economic risk.

In the 13/5 issue, we will be covering and Tayca (4027), Sysmex (6869) Toyota Motor (7203), United Arrows (7606), SBI Holdings (8473) and Pasco (9232).

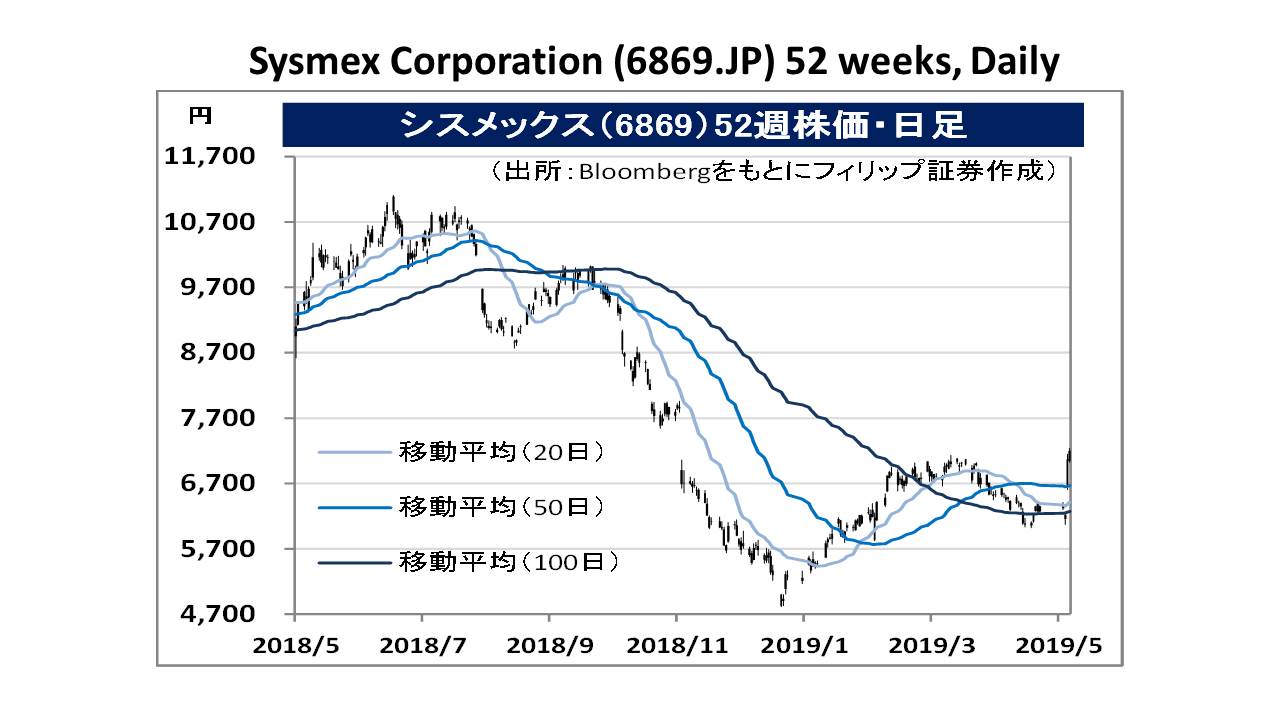

・Established in 1968 as a comprehensive supplier for laboratory tests. In addition to the fields of haematology (blood cell count test), immunological tests, coagulation tests, etc., company also carries out the research development to the manufacture, retail and service & support as a whole for equipment, reagents and software in the fields of life sciences, etc. Holds the global top shares in the field of haematology.

・For FY2019/3 results announced on 8/5, net sales increased by 4.1% to 293.506 billion yen compared to the previous period, operating income increased by 3.7% to 61.282 billion yen, and net income increased by 5.1% to 41.224 billion yen. Reagants for the blood cell count test, blood coagulation test, immunological tests, and life sciences, etc. overseas, have grown. Company has also overcome the termination of the joint venture with bioMérieux to lead to an increase in profit.

・For FY2020/3 plan, net sales is expected to increase by 9.0% to 320 billion yen compared to the previous year, operating income to increase by 4.4% to 64 billion yen, and net income to increase by 1.9% to 42 billion yen. Profitability is predicted for the life science business in the mid-term plan up to FY2022/3, and due to the expansion of applications of the cancer detection method, OSNA, etc., annual average revenue growth rate is targeted at 35.9%.

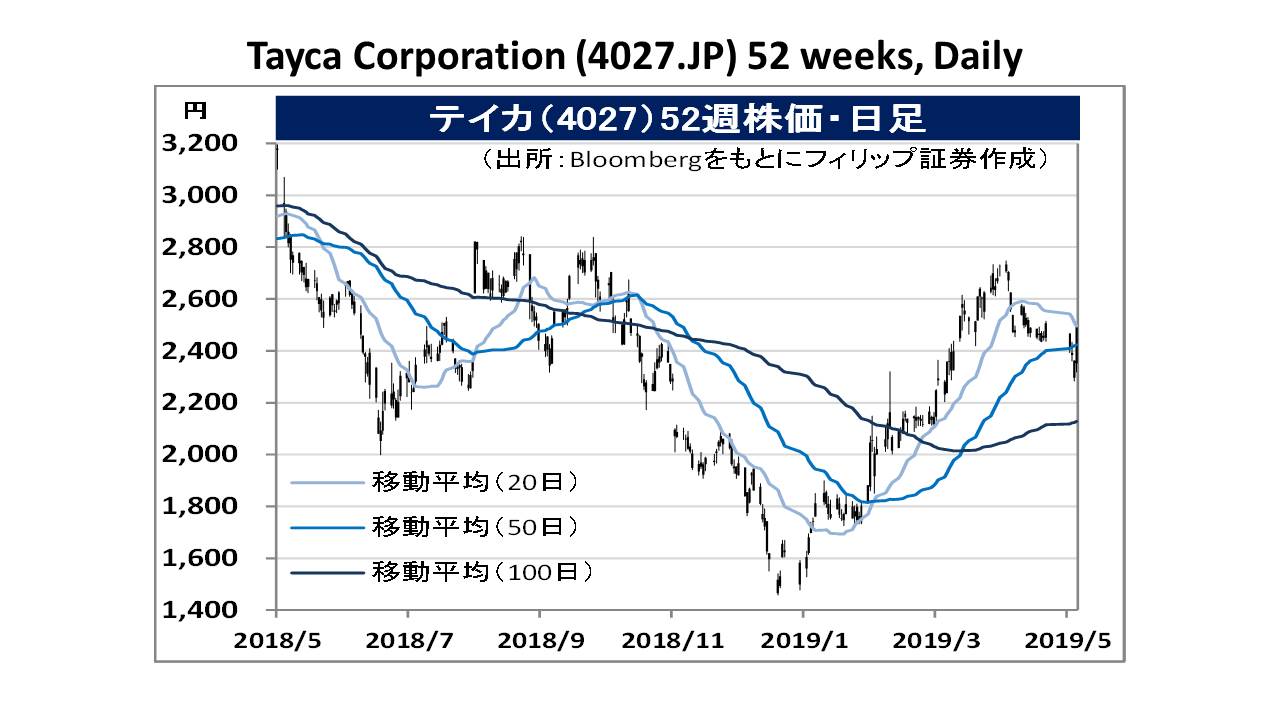

・Founded in 1919 as an imperial artificial fertiliser which had sulphuric acid and superphosphate fertilisers as their main products. Carries out the manufacture and retail of chemical industry chemicals such as titanium oxide, surfactants, sulphuric acid, particulates of titanium oxide, surface treatment products and pollution-free anticorrosive pigments, etc. In recent years, they have been focusing their efforts on new fields, such as particulate titanium oxide for cosmetics and piezoelectric ceramics for ultrasonic echos, etc.

・For FY2019/3 results announced on 9/5, net sales increased by 11.4% to 47.385 billion yen compared to the previous period, operating income decreased by 4.0% to 5.803 billion yen, and net income increased by 10.6% to 4.007 billion yen. Although sales of functional-use titanium oxide particulates and surface treatment products have performed strongly, rising manufacturing costs have been a burden. Extraordinary loss due to impairment has been recovered.

・For FY2020/3 plan, net sales is expected to increase by 9.7% to 52 billion yen compared to the previous year, operating income to increase by 17.2% to 6.8 billion yen, and net income to increase by 12.3% to 4.5 billion yen. Due to the increase in interest towards UV protection, we can expect the demand for titanium oxide particulates and zinc particulates to increase for UV cut agents. Also, the company has plans to carry out development of the South East Asian market.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: