Report type: Weekly Strategy

“The Political Market and Value Investing Are Factors for Supporting Japanese Stocks”

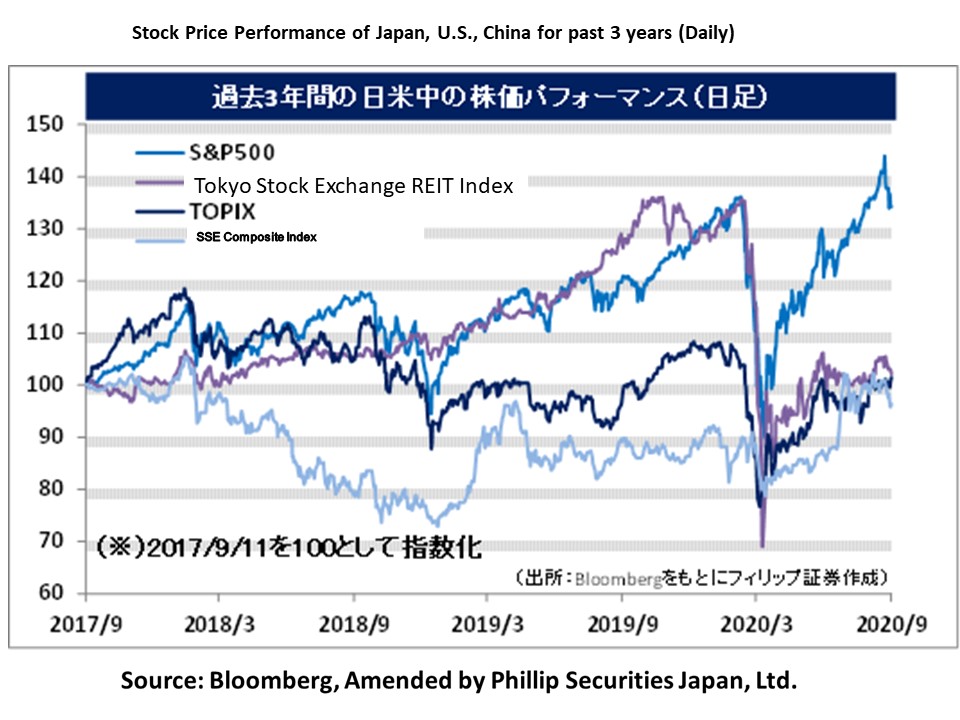

In the 31st August 2020 issue of our weekly report (Focus on the COVID-19 Catastrophe Shifting to Nursing Care and the Start of the Political Market), 11/9 was an SQ day involving futures and options transactions of the Nikkei average, and we mentioned the need to be careful of the increase in stock price volatility in the 2 weeks leading up to it. Even with the large fall in the U.S. stock market from 3/9 mainly in high-tech and IT stocks, the Japanese stock market performed strongly for the most part within a narrow range. Compared to the Nikkei average’s closing price on 28/8 at 22,882 points, the SQ value calculated based on the opening quotation of 225 stocks comprising the index was 23,272 points. We can consider the following 2 points as the main factors for the strong market turnout in Japanese stocks which differed from U.S. stocks.

The first is that the political market had begun. For the Liberal Democratic Party presidency election, the joint plenary meeting for the party members from both houses of the Diet is to be held on 14/9 with voting and counting to take place, and on 16/9, the next prime minister is scheduled to be nominated via a convocation for an extraordinary Diet session. Chief Cabinet Secretary Suga, who is a strong candidate for the next prime minister and is running for the Liberal Democratic Party’s presidency election, demonstrated a careful stance in the dissolution of the House of Representatives and the general election after repeatedly expressing his thoughts on “the ought to prioritise COVID-19 countermeasures over all” in a commercial broadcast program on 8/9, however, since Kono, the Minister of Defence who participated online in the U.S. think tank event remarked that “an early snap election will likely be held sometime in October”, perhaps market participants have begun to be aware of the dissolution of the House of Representatives and the general election. Including the time in autumn 3 years ago, the dissolution and general election is often regarded as a strong source of material for the purchase of Japanese stocks, and is regarded as one of the factors for Japanese stock purchasing.

The next factor is the trend of “value stock” investing coming into full force, which is represented by Warren Buffett’s purchases of general trading company stocks. Regarding investments in low P/B (price-to-book ratio) or value stocks with high dividend yield, in our 25th May 2020 issue of our weekly report, “Breaking Away From “PBR Shakeup” and Low PBR Stocks”, with the uncertainty involving the impact of the COVID-19 catastrophe, attention was already on low P/B ratio stocks, where the P/B ratio is regarded to have higher certainty as a measure of investment over the forecasted P/E ratio (price-earnings ratio), however, due to the fall in prices of “growth stocks” that are expected to grow which are represented by U.S. high-tech and IT stocks, it appears that there might have been an increase in the pace of the shift from growth to value. Also, regarding the overly low market capitalisation of large corporations which involve national policy, from the viewpoint of the risk of them being acquired by overseas corporations, it seems that the Japanese government will not be able to overlook them.

For the Japanese stock market for the time being, there is a need to be wary of risks of a fall in U.S. stock prices due to the election of Joe Biden as the U.S. president, who mentions a tax hike, as well as the growing possibility of a full-scale stop in semiconductor export from corporations utilising U.S. technology to China’s Huawei.

In the 14/9 issue, we will be covering Nippon Steel (5401), NEC (6701), AOKI Holdings (8214), and INES (9742).

・Steel manufacturer that established in 1950. Nippon Steel started from a merger between Yawata Iron & Steel and Fuji Iron & Steel in 1970, and after starting Nippon Steel & Sumitomo Metal after a merger with Sumitomo Metal Industries in 2012, they changed their company name to the current one in 2019.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 4/8, sales revenue decreased by 25.7% to 1.1316 trillion yen compared to the same period the previous year, business profit went from 60.6 billion yen the same period the previous year to (27.51) billion yen and net income from 33.325 billion yen the same period the previous year to (42.071) billion yen, which fell into the red. The sudden drop in sales of steel materials, etc. for automobiles due to COVID-19 have affected.

・For its FY2021/3 plan, for business profit which indicate results of sustainable business activities, compared to (150) billion yen in the first half (Apr-Sep), the latter half (2020/10-2021/3) is predicted to return to profit at 30 billion yen due to the increase in crude steel production. Due to the prioritisation of the production facility structure countermeasure which was decided on 7/2 this year, the company predicts that they will pass dividends. Expectations are on the earlier than expected achievement of the targeted company profit growth of 100 billion due to the decrease in the scale of crude steel production capability of 5 million tonnes per year and a 4 cardinal number decrease in the blast furnace cardinal numbers.

・Founded in 1899. Manages system integration and outsourcing cloud services via 5 businesses, which are public, enterprise, network services, system platforms, and global.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 31/7, sales revenue decreased by 10.1% to 587.729 billion yen compared to the same period the previous year, and operating income fell into the red from 3.382 billion yen the same period the previous year to (10.274) billion yen. Despite the improvement in selling, general and administrative expenses at a 3.3% decrease, the decrease in large-scale projects and the demand in updating business PCs completing a cycle have affected, which led to a revenue decrease and operating deficit.

・For its full year plan, sales revenue is expected to decrease by 2.1% to 3.3 trillion yen compared to the previous year and operating income to increase by 17.5% to 150 billion yen. Company is strengthening efforts in the 5G area, such as the joint development of 5G core networks with Rakuten Mobile which was announced on 3/6, as well as the capital business partnership with NTT (9432) involving the joint development on 5G technology which was announced on 25/6, etc. Ahead of the implementation of rules on the Chinese communications giant, Huawei, by the U.S. on 15/9, the company’s shares in overseas 5G communication base stations are predicted to increase.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: