Report type: Weekly Strategy

“The Nikkei Average Awaits Financial Results, Attention on Japan and Developed Countries Facing Challenges”

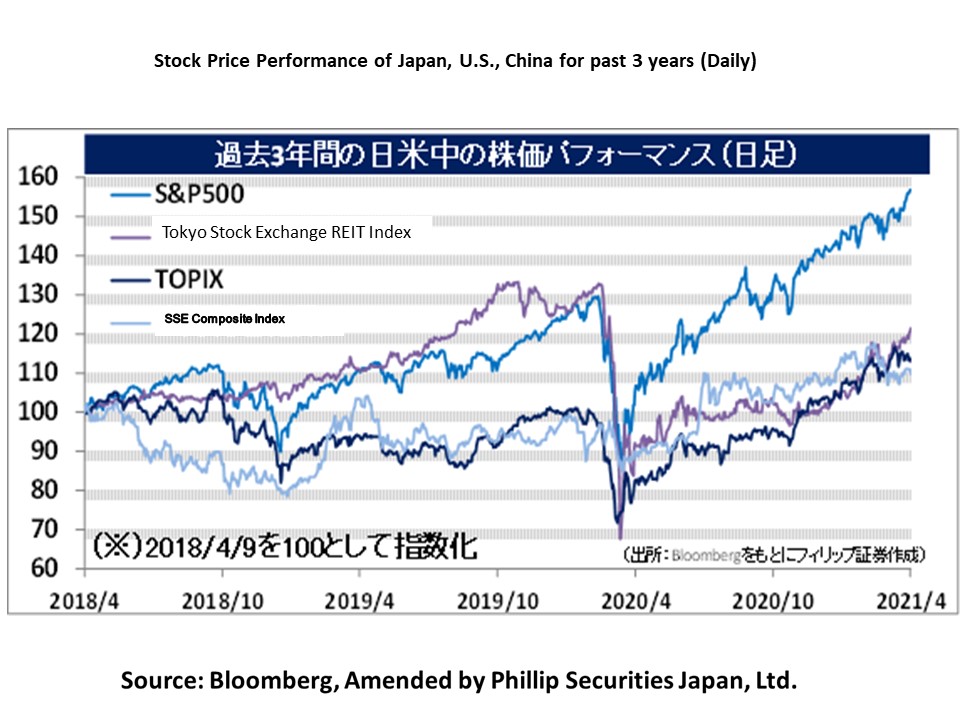

In response to the announcement by U.S. President Biden on 31/3 of the “U.S. Employment Plan”, an infrastructure investment plan of a scale of 2.25 trillion dollars, in contrast to major stock price indices in the U.S. stock market renewing their record highs across the broad at the start of the week on 5/4 just after the Easter holidays, the Nikkei average hit a plateau within a high price range. Due to the increasing trend in the Nikkei average which started from the low of 22,977 points on 30/10 and has lasted over about 5 months till now, the range around 23,000 points has been regarded as a turning point in the stock market. Taking 23,000 points as the middle level of the stock market range and presuming a range with a lower limit that is the low of 16,358 points on 19/3 last year, if we assume that the middle level is the middle of the price range from the upper limit to lower limit of the stock market range, we can estimate that the upper limit of the stock market range will be 29,642 points. Perhaps the price level around this will be regarded as a turning point in future stock market developments as well.

The Nikkei average’s closing price on 8/4 is of a 1.32 times weighted average P/B ratio (price-to-book ratio) with weight attached on the market capitalisation of index components, etc., and is a level that is close to 1.39 times in Jan 2018, which has been the greatest in the past 5 years, despite having decreased from 1.36 times on 18/3. We ought to be careful about the aspect of tending to regard it as overvalued. The weighted average BPS (net asset per share) of the Nikkei average which hit about 22,500 points on 8/4 is thought to be increasing due to the addition of each corporation’s net income to the BPS after going through every quarterly financial results announcement. Even if the weighted average BPS at the end of this year were to increase to 25,000 points, based on calculation, it will finally hit 34,750 points at the P/B ratio of 1.39 times. It would be likely impossible to justify from a fundamentals perspective to expect it to jump to 35,000 points or 39,000 points, which exceeds the record high price, without experiencing an increase in net income.

Even amongst the world, Japan stands out for its “aging population” and “natural disasters”. Perhaps there is also a

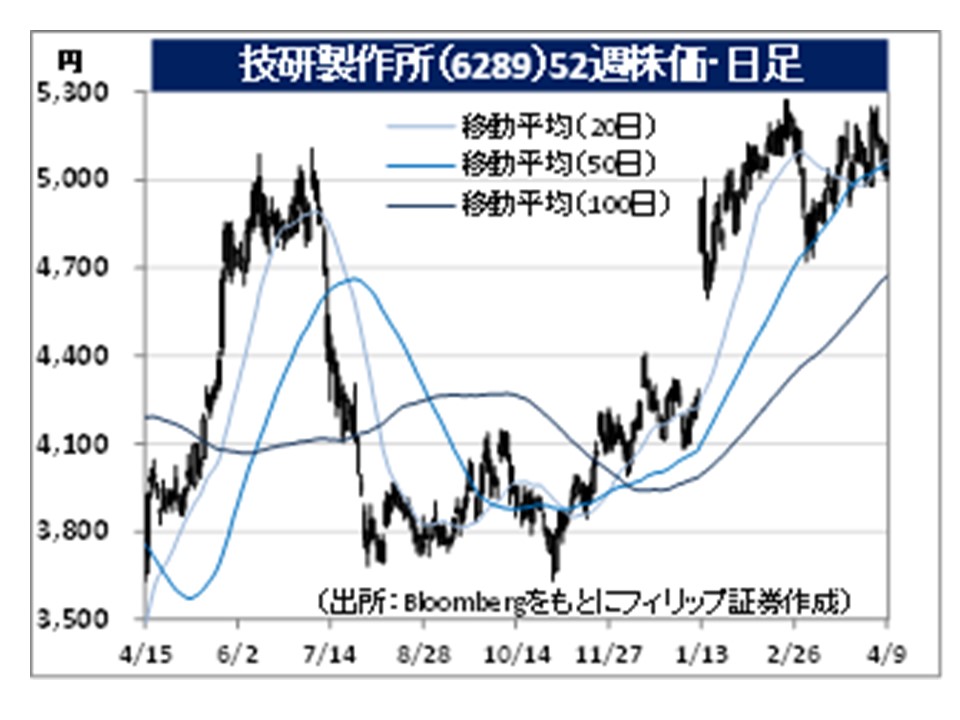

demand in international society for Japan as a developed country that faces challenges to give back to the rest of the world their results of experience and research and development in these 2 areas. Regarding an “aging population”, in terms of the “aging ratio”, which refers to the ratio comprised by those 65 years and above in the population, in 2020, Japan was top in the world at 28.7%, significantly exceeding the overall world’s 9.3%. With there being progress in aging worldwide, perhaps the acceleration in overseas expansion of “HAL”, a body-wearing robot for healthcare and nursing care handled by CYBERDYNE (7779), would be desirable internationally as well. Also, according to the “World Risk Report” released by the United Nations University in Aug 2016, as a result of analysing 28 items of indices on 5 types of national disasters, which are earthquakes, typhoons, floods, droughts and the rise in sea level, it was said that Japan was 4th in the world to be subjected to risks of natural disasters. There is also focus on the movements of GIKEN (6289), which is accelerating overseas expansion based on expertise cultivated from the National Resilience countermeasure.

In the 12/4 issue, we will be covering GIKEN (6289), ROHM (6963), Japan Securities Finance (8511), and Japan Exchange Group (8697).

・Founded in 1967. Carries out the construction machinery business, such as the development, manufacture, retail and maintenance services involving the non-vibration and noiseless hydraulic pile press fitting and extraction machine (Silent Piler), as well as the press fitting construction business, which utilises innovative construction methods of press fitting technology.

・For the company’s forecasted business performance for 1H (2020/9-2021/2) results of FY2021/8 announced on 1/4, it was revised upwards with net sales expecting to decrease by 8.1% to 13.293 billion yen (original plan 12.8 billion yen) and operating income to decrease by 13.0% to 2.169 billion yen (original plan 1.3 billion yen). The retail period for overseas products being brought forward and the decrease in cost price due to improved efficiency in press fitting construction have contributed.

・For its full year plan, net sales is expected to decrease by 10.6% to 27.1 billion yen compared to the previous year and operating income to increase by 26.1% to 3.15 billion yen. With “changing construction in the world with innovative construction methods (implant construction method)” as their management policy, in addition to current preparations on projects in Amsterdam City in the Netherlands and a tailings dam in Brazil, the company has set up a representative office in Bangkok, Thailand on 15/3. There is anticipation on the adoption of the company’s construction method in large-scale river renovation for the purpose of flood prevention measures in Thailand, where there are frequent flood damages

・Founded in Kyoto in 1954 for the development and retail of fixed carbon film resistors. Expands business segments, such as large-scale integrated circuits (LSI), semiconductor elements, modules and others (resistors, etc.). Company is top in Japan for custom LSIs.

・For 9M (Apr-Dec) results of FY2021/3 announced on 1/2, net sales decreased by 5.6% to 263.678 billion yen compared to the same period the previous year and operating income decreased by 6.8% to 24.464 billion yen. Despite a decrease in revenue and operating income due to effects of the COVID-19 catastrophe, such as restrictions in operation of factories in the Philippines, in 3Q (Oct-Dec), there was an improvement with net sales increasing by 9.9% and operating income increasing by 77.4% compared to the previous quarter.

・Company revised its full year plan upwards. As a result of trends of a sharp recovery for markets related to automobile in electronics, net sales is expected to decrease by 0.8% to 360 billion yen (original plan 340 billion yen) compared to the previous year and operating income to increase by 8.5% to 32 billion yen (original plan 23 billion yen). The company is aiming for a global share of 30% by 2025 in the SiC (silicon carbide) power devices market, which is predicted for a proper expansion in the in-vehicle inverter area following a popularisation of electric cars (EV).

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: