Report type: Weekly Strategy

The Japanese Stock Market in 2019 and the Outlook for 2020 and Thereafter

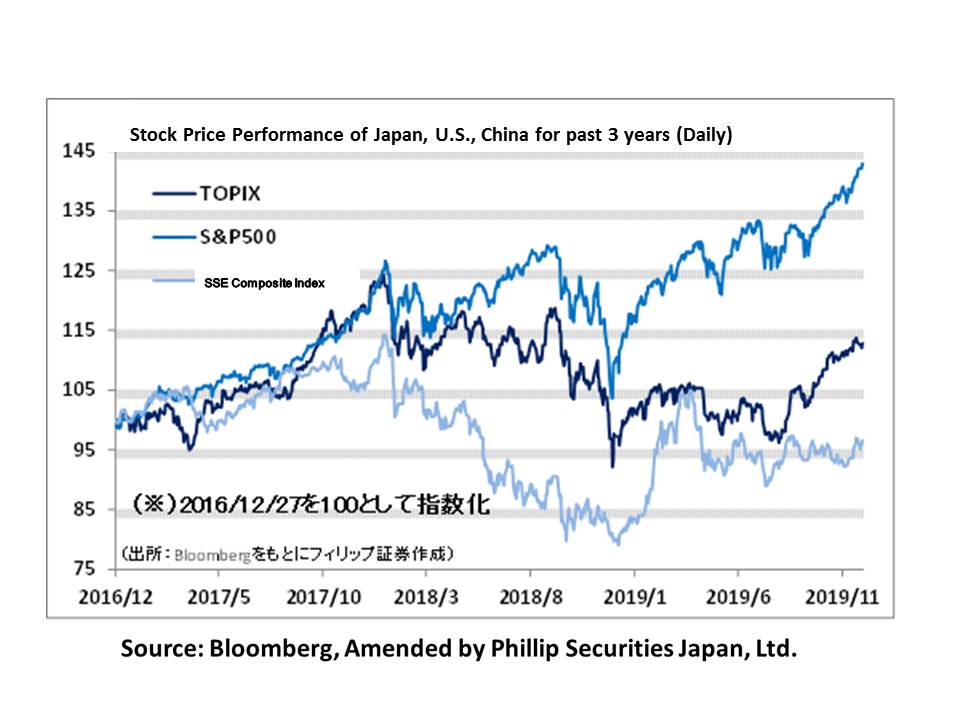

We are at the last trading day of 2019. For the Japanese stock market, the Nikkei Average had fluctuated at a rate of around 20% since the beginning of the year. Indeed, looking back at the past 12 months, we can remember it as a year with good transitions. However, the process along the way was far from smooth. Firstly, concerns over risks regarding the US-China trade war have led to strong selling from the start of the year. In credit transactions, short sales exceeded margin buying, resulting in the appearance of “long shares” with margin debt balance ratio below 1.0. However, we could also see market support when there were movements to buy back before the March closing date and the long holidays commemorating the change of era. The selling pressure affected the Nikkei Average as a result. In arbitrage trading involving spot and futures trades of the index, the “unsettled sales balance” vastly exceeded the “unsettled buying balance” after 2019/6. In early September, we even saw the unsettled buying balance becoming less than 20% of the unsettled sales balance.

Under such selling pressures, the Nikkei Average plummeted to its lowest value for year 2019 to 20,110 points on 6/8. At that time, the weighted average PBR (Price to Book Ratio) of the 225 stocks adopted by the Nikkei Average was 1.01 times, and did not fall below the BPS (Book Value per Share) which is the liquidation value of a company. That provided an opportunity to review the overselling which reached a level where there were no justifiable reasons in terms of fundamentals. Indeed, it afforded an opportunity to highlight the relative cheapness of Japanese equities compared to their asset values. Since autumn, repurchase of spots owing to elimination of unsettled sales balance of arbitrage trading related to the Nikkei Average has been the driving force for the rise in market prices. On 2019/12, for the first time in about six months, the Nikkei Average rose to around 24,000 points when the unsettled buying balance exceeded the unsettled sales balance.

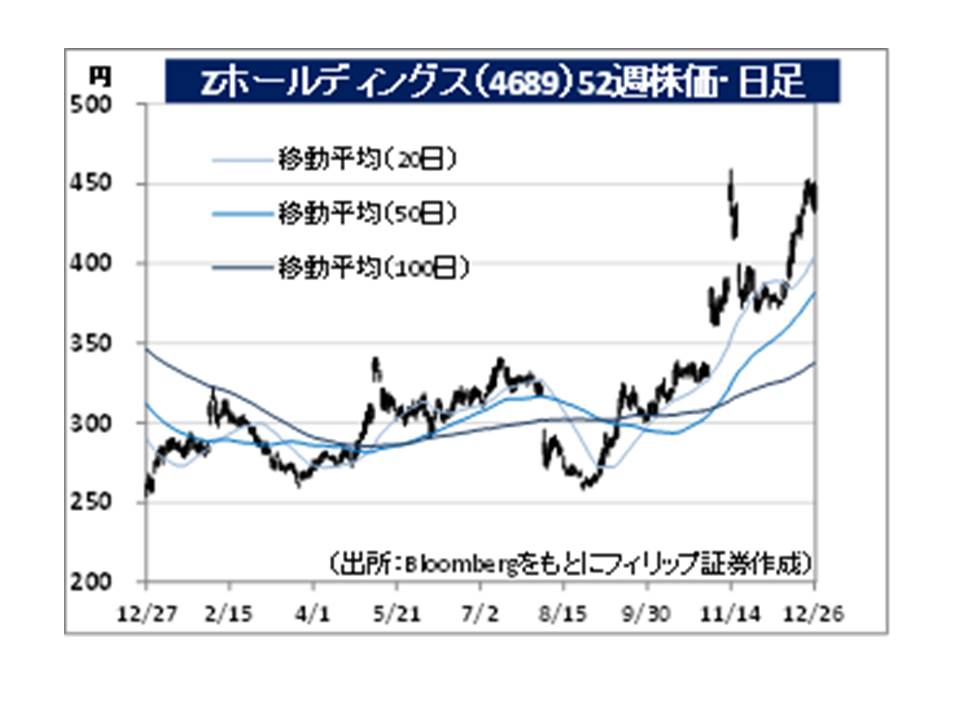

What then are the main issues confronting the Japanese economy and Japanese companies from 2020 onwards. Firstly, as seen in the integration of LINE (3938) and ZHDS (4689), there will be increasing expectations in the stock market to see companies aiming for “super APPs” that can compete with huge platformers not only in the Japanese market, but also in the world. Next are expectations placed on “Local 5G”, for which the Ministry of Internal Affairs and Communications has started accepting license applications on 24/12. Manufacturing productivity will be greatly improved if every device is automated and connected to the internet at factories belonging to manufacturers, and data are collected in real time in a 5G communication environment. Let’s pay attention to this as-yet unmasked sector having great potential to revive the Japanese economy.

In the 30/12 issue, we will be covering Z Holdings Corp (4689), Kawasumi Laboratories (7703), Nintendo (7974), and NTT (9432).

・Established in 1996 as a subsidiary of the current Softbank G (9984). Involved with Ecommerce and media businesses. Had a change in company name from Yahoo Japan on 2019/10. Finalized an agreement for business integration with LINE (3938) on 2019/12.

・For 1H (Apr-Sept) results of FY2020/3 announced on 1/11, revenue increased by 4.1% to 484.145 billion yen compared to the same period the previous year, and operating income decreased by 9.0% to 75.661 billion yen. Advertising revenue and increase in consolidated subsidiary sales had contributed to increase in revenue. Operating income declined due to an increase in depreciation and SG&A expenses, as well as a gain on sales of IDC Frontier Inc. recorded in the same period of the previous year as a one-time factor.

・For its full year plan, revenue is expected to increase by between 4.7-6.8% amounting to 1.00-1.02 trillion yen compared to the previous year, and operating income to increase by between 0.1-6.7% amounting to 140.6-150.0 billion yen. Finalized an agreement for business integration with LINE on 23/12. Positioning LINE, which is also popular in Thailand and Taiwan, as a “platform-based APP (super APP) that will be the starting point for various businesses and lifestyles. Let’s pay attention to its strategy of using PayPay, its payment application, as a main pillar to compete with major overseas platform companies.

・Established in 1954. Main businesses include the manufacture and sale of blood and intravascular products such as blood bags and blood sampling kits, as well as medical equipment and pharmaceuticals related to extracorporeal circulation such as dialyzers (artificial kidneys) and physiological saline.

・For 1H (Apr-Sept) results of FY2020/3 announced on 7/11, net sales decreased by 2.6% to 11.324 billion yen compared to the same period the previous year, and operating income increased 8.6 times to 535 million yen. Sales declined due to withdrawal from unprofitable businesses and sales decline of physiological saline. However, operating income increased owing to structural reforms and improvement in cost of sales ratio and reduction in personnel costs through cost reduction efforts.

・For its full year plan, net sales is expected to decrease by 7.9% to 22.2 billion yen compared to the previous year, and operating income to increase by 50.4% to 900 million yen. In the extracorporeal circulation business, the company has been withdrawing from unprofitable businesses and consolidating its sales bases. Meanwhile, in the endovascular field, the company has been working on selecting and concentrating on businesses such as launching new products and expanding sales of stent grafts in Europe. As international expansion of medical devices is a priority area of the government’s growth strategy, we can expect push factors going forward.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: