|

Report type: Weekly Strategy |

“The FY22 Apr-Jun Corporate Performance in the U.S. and Japan, Economic Risk in China and Europe”

On a weighted average basis, the Nikkei average’s (closing price on the 18th) forecasted P/E ratio (price-earnings ratio) was 13.01 times and its P/B (price-to-book) ratio was 1.18 times. After a cycle of financial results announcements, it is also a situation where the pressure of the increase in stock price based on a business performance aspect tends to weaken. Considering that its P/E ratio exceeding 13 times is also approximately equivalent to the recent Nikkei average’s 29,000 points, it appears that the high is not rising further.

According to The Nikkei, for the FY2022 Apr-Jun period, those which had record high net income in the same period were mainly industries that benefited from high resource prices, such as trading companies, petroleum and iron and steel, etc., and had increased to 1 out of 4 of the total number of companies. On the other hand, net income for overall listed enterprises decreased by 26% compared to the same period the previous year. While the depreciation of the yen has its advantages, automobiles and electrical machinery were in a slump due to supply constraints and high raw material prices.

In comparison, for the U.S. S&P 500 index’s constituent enterprises (until the 2nd, a survey by Refinitiv) in the Apr-Jun period, net sales increased by 12.5% and net income increased by 8.1%, which had strong performance exceeding the forecast. Towards Jul-Sep, Apple (AAPL) predicts growth in iPhone following an easing of supply chain constraints. In Japan as well, enterprises forced to have a profit decrease due to supply constraints are likely expected to recover in the Jul-Sep period. In particular, despite there being an increase in revenue in business segments related to medical equipment due to them being supported by strong demand, there will be focus on the glaring example of a significant profit decrease as a result of the shortage of components and raw materials mainly arising from the semiconductor shortage.

Regarding resource prices, there is concern on the trend of China’s economy, which accounts for a large percentage of consumption related to commodities. Retail net sales for July announced on the 15th increased by 2.7% year-on-year, which slowed down from the previous month (3.1% increase). Industrial production had a 3.8% increase, which declined in growth rate by 0.1 points from the previous month. In particular, for precious metals, it is likely that the continuous fall in the CMX Gold Futures price from the 15th to 18th was attributed by concerns on weak demand in the Chinese economy.

Between fall to winter, we should be most wary of Europe trends. In the UK, the Consumer Price Index (CPI) for July announced on the 17th increased by 10.1% year-on-year, which had a 0.7 point increase in growth rate from June and was of a high level last since approx. 40 years ago. In the Eurozone as well, revised figures of the Eurozone’s CPI for July announced on the 18th increased by 8.9%, which had a 0.3 point increase in growth rate, renewing the record high.

In Europe, electricity and gas prices are expected to rise significantly from October onwards, and an acceleration in inflation and more large interest rate hikes are predicted. It is likely that the ECB (European Central Bank), which faces the issue of market segmentation due to a yield discrepancy between Germany and Italy, will face difficult leadership. There is also the possibility of an acceleration in the global long-term interest rate due to its origin in Europe. Also, Germany’s gas and electric company, Uniper SE, which fell into financial difficulty due to the energy crisis, recorded a deficit of 12.3 billion Euros in net profit or loss in the FY22 Jan-Jun period. Between fall to winter, last year, China’s real estate development enterprises were shaken. This year, there will likely be a need to watch out for European enterprises.

In the 22/8 issue, we will be covering NTT Data Intramart (3850), Takeda Pharmaceutical (4502), Nikkiso (6376) & Nissha (7915).

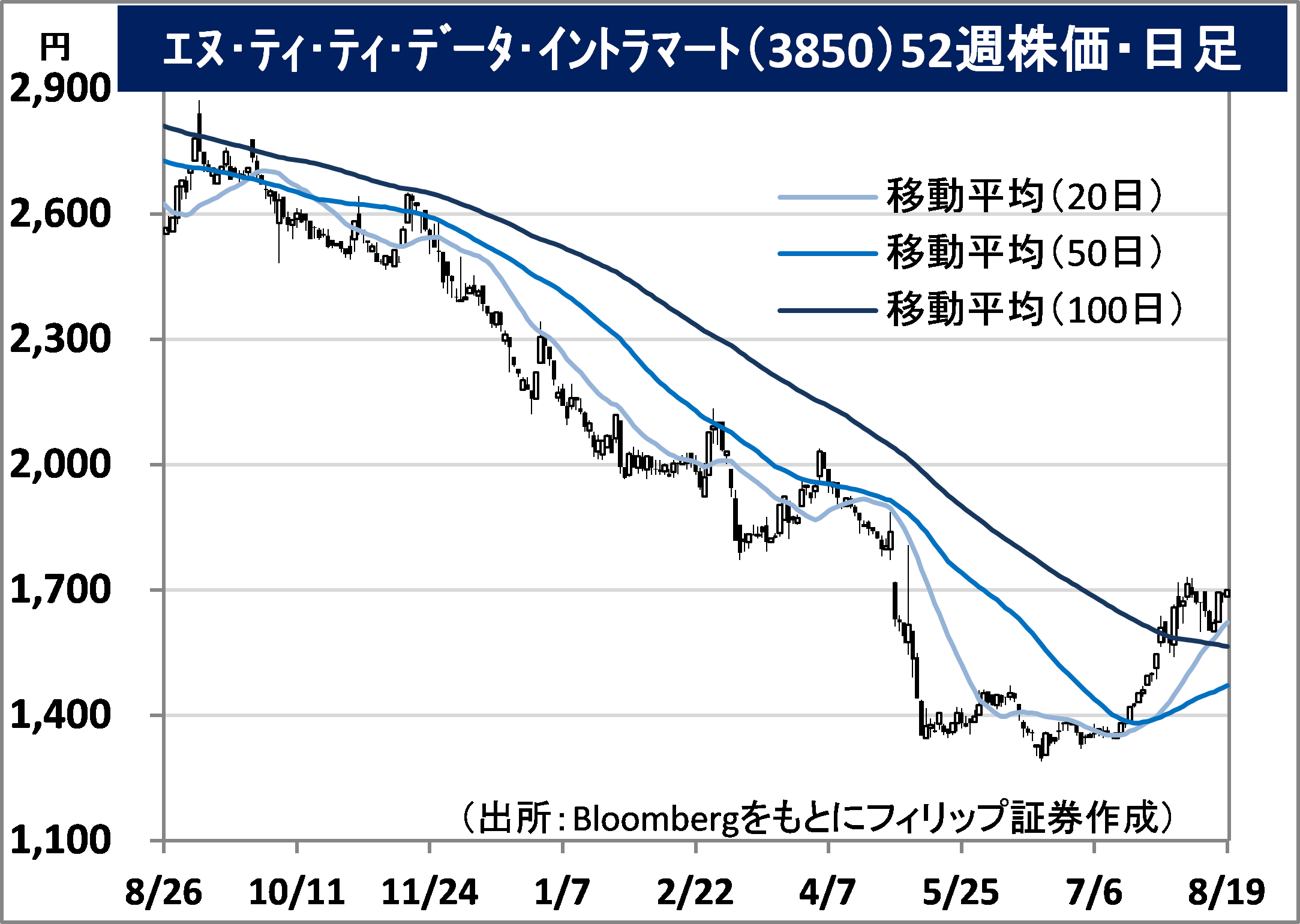

・Established in 2000 with its predecessor being an in-house venture of its parent company, NTT Data (9613). Develops and provides the web system construction infrastructure product “IAP” and the work task application “intra-mart series”, which uses it.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 27/7, net sales increased by 21.9% to 2.023 billion yen compared to the same period the previous year and operating income increased by 24.5% to 184 million yen. The software business, which has a sales distribution ratio of 58%, had a 29% increase in revenue from the strong performance of higher infrastructure products following a shift in “intra-mart” from its previous workflow to the core field. The service business also had a 14% increase in revenue.

・For its full year plan, net sales is expected to increase by 1.6% to 7.78 billion yen compared to the previous year and operating income to decrease by 52.6% to 400 million yen. Based on the mid-term management plan from FY2022 to 25, in the current period, they are expecting a decrease in profit as a result of planning significant investment for the purpose of reinforcing promotion and enriching products and services. In addition to the issue of resolving parent-subsidiary listing in terms of corporate governance, the company’s “EV/EBITDA ratio after adjustment”, which is also the simplified acquisition ratio, was a low level of 2.7 times (as of 17/8), which ought to be watched out for.

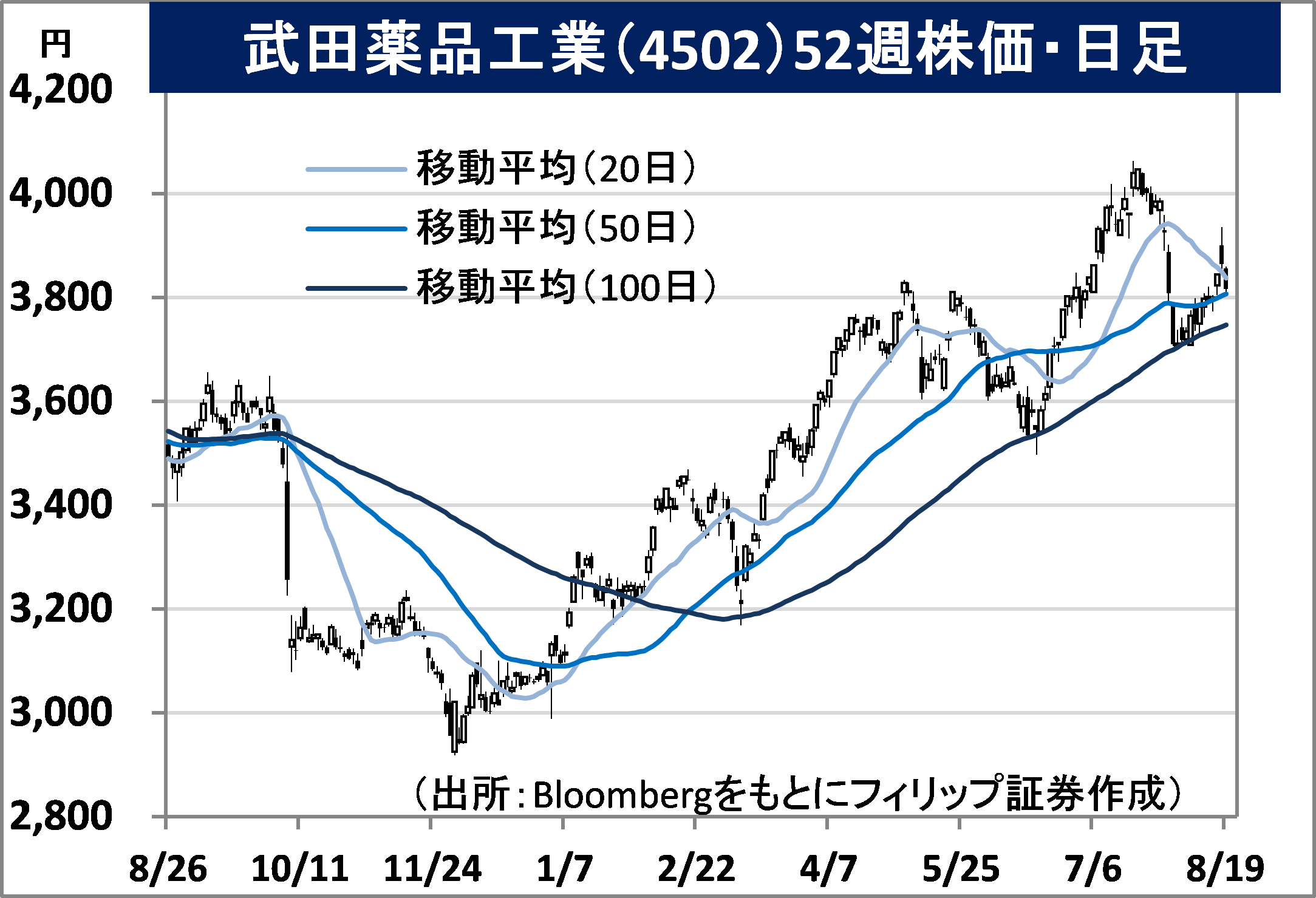

・Founded in 1781 (the first year of Tenmei) in Doshomachi, Osaka by Chobe Omiya. Focuses on digestive system diseases, rare diseases, immune diseases, cancer and neuropsychiatric disorders, etc. Acquired Ireland’s Shire in 2019 for 6.2 trillion yen.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 28/7, sales revenue increased by 2.4% to 972.465 billion yen compared to the same period the previous year, and core operating profit excluding impact from temporary factors increased by 28.2% to 319.1 billion yen. Despite transferring their Japan diabetes therapeutic agent portfolio of 133 billion yen to Teijin Pharma in the same period the previous year, strong performance in the field of major diseases and the depreciation of the yen have contributed to an improvement in business performance.

・For its full year plan, net sales is expected to increase by 3.4% to 3.69 trillion yen compared to the previous year, core operating profit to increase by 12.8% to 520 billion yen and annual dividend to remain unchanged at 180 yen. On the 17th, it was reported that the company would be the first enterprise in Japan to begin the worldwide retail of a vaccine. The vaccine for dengue fever will be retailed in 30 countries worldwide and net sales target is set at approx. 210 billion yen. They are global leaders in the development of treatments for “neglected tropical diseases (NTD)”, where there are approx. 20 types in Japan.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: