|

Report type: Weekly Strategy |

“The Context for Exceeding 28,000 Points and Expectations of a Revaluation of the P/E and P/B Ratio Levels”

The Nikkei average finally exceeded the big mark of 28,000 points on the 5th. While resisting successive stresses and unfavourable conditions in the external environment, such as the sudden occurrence of geopolitical risks, such as the firing of warning anti-ballistic missiles and the large-scale military exercise by China after Pelosi, the Speaker of the U.S. House of Representatives, visited Taiwan, as well as the appreciation of the yen against the dollar until the 130 yen mark, we can infer that short positions had accumulated while it repeatedly fought on whether to hit the big mark on the 22nd, 28th and 29th of last month and on the 1st and 4th of this month. Once it surpasses the big mark, the increase in the Nikkei average by about 100-200 points at once from the big mark due to the involvement of forward buying for the purpose of delta hedging on price fluctuation risks involving short positions of call options as well as cutting losses by the sellers are likely familiar movements involving a big mark.

It is not only these supply and demand factors, but it is likely that the factor of fundamentals based on corporate performance is also important for having surpassed the big mark on the 5th. With the announcement of the FY2022 Apr-Jun period financial results underway, on the basis of the closing price on the 4th, the Nikkei average’s forecasted P/E ratio (price-earnings ratio) based on a weighted average that has considered differences, such as market capitalisation, etc., became 12.78 times and its weighted average P/B ratio (price-to-book ratio) became 1.15 times. Although this is not to the extent of the same forecasted P/E ratio of 11.97 times and P/B ratio of 1.10 times on 9/3 which marked the low since the start of the year, we can likely say that it is of a sufficiently undervalued level. Excluding the impact of abnormal movements during the initial response to the spread of COVID-19 in March 2020, in the past 10 years, the same forecasted P/E ratio generally shifted within the level of 12-24 times and the P/B ratio in the level of 0.9-1.5 times. Based on a comparatively shorter timeframe from mid-May last year onwards, the same forecasted P/E ratio has been shifting within the level of 12 to 14 times.

Also, the trend of the increase in the negative range of inflation-linked bonds or the real interest rate which has deducted the expected inflation rate from the nominal interest rate due to the continuation of the Bank of Japan’s quantitative monetary easing should theoretically be a factor that supports a revaluation of the forecasted P/E and P/B ratio. Perhaps there is room to reconsider the many Japanese stocks that are being neglected at present which are predicted to have a reinforced return to shareholders, improved performance and have a P/B ratio of under 1.0 as investment targets where one can expect a mid-term increase and being undervalued.

The increase in the negative range of the real interest rate tends to work in favour of growth stocks as opposed to value stocks. In the Tokyo Stock Exchange growth market, there are stocks that have exceeded a market capitalisation of 100 billion yen, such as Visional (4194), Freee K.K. (4478), ANYCOLOR (5032) and JTOWER (4485), etc., which are also gaining attention for their transition to the prime market in the future. ANYCOLOR is likely appealing in terms of future growth potential from its good compatibility between V-Tubers and the metaverse (online virtual space). Also, as indicated from the good financial results of the communications measurement equipment Anritsu (6754), there is a need to focus attention on JTOWER as it is being watched for the recent increase in demand for faster network speed and 5G communications development.

In the 8/8 issue, we will be covering McDonald’s Holdings Company (Japan) (2702), Toyo Suisan Kaisha (2875), JTOWER (4485) and Tokyo Keiki (7721).

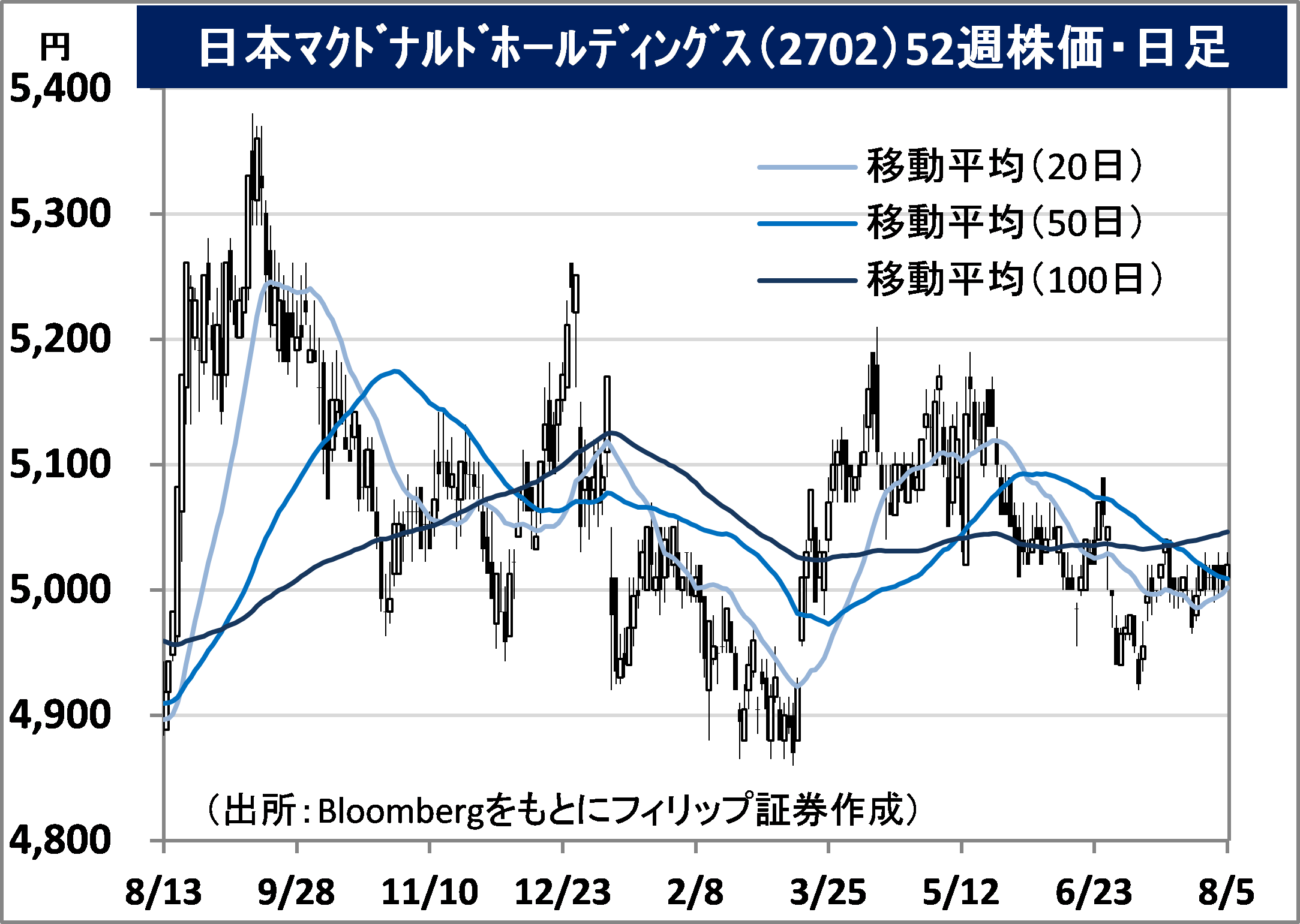

・Became a holding company in 2002. Holding ratio related to the U.S. McDonald’s headquarters is approx. 35%. Expands directly managed stores and stores via the franchise method which accounts for approx. 70%. The U.S. McDonald’s pays royalties for licenses.

・For 1Q (Jan-Mar) results of FY2022/12 announced on 12/5, net sales increased by 11.1% to 84.289 billion yen compared to the same period the previous year and operating income increased by 4.5% to 9.643 billion yen. Despite retail restrictions following delays in potato imports from North America and the same number of 10 stores in both new store openings and store closures, digital strategy, such as mobile ordering, delivery and drive-thrus have been successful.

・For its full year plan, net sales is expected to increase by 4.8% to 333 billion yen, operating income to increase by 1.4% to 35 billion yen and annual dividend to remain unchanged at 39 yen. Same-store sales for July announced on 4/8 increased by 8.1% year-over-year. Although the number of customers increased by only 2.3%, customer transaction increased by 5.6%. Digital policy for delivery, takeaway and drive-thru and their strategy to reinforce the dinnertime period are progressing smoothly. There is a slight delay in stock price compared to the U.S. McDonald’s (MCD).

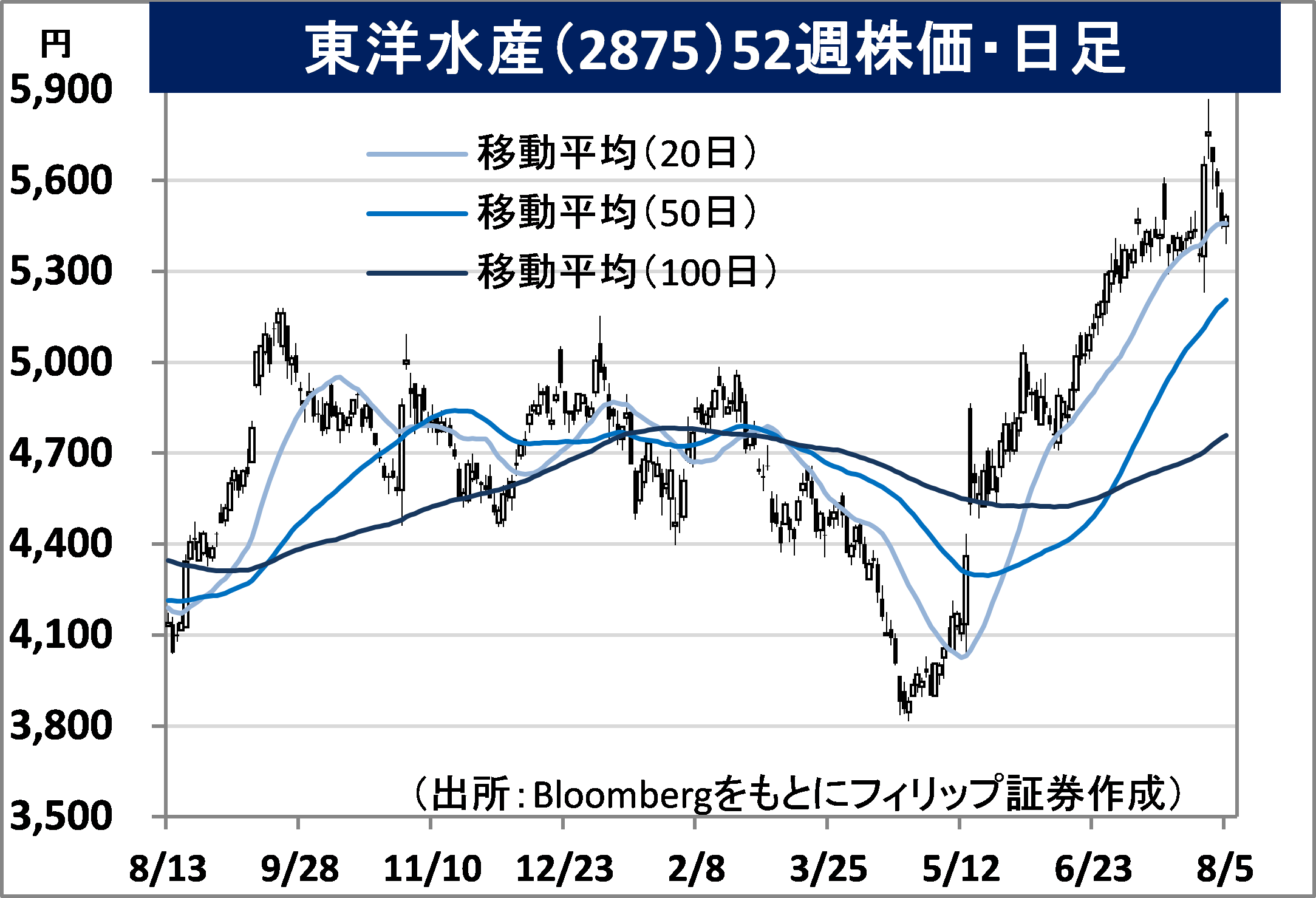

・Established in 1953 as Yokosuka Suisan in Tsukiji fish market. Mainly manages 6 businesses, which are marine foodstuff, overseas instant noodles, domestic instant noodles, cold foodstuff, processed foodstuff and cold storage. Their overseas instant noodles holds the top spot in the U.S. and Mexico and their domestic instant noodles is No.2.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 29/7, net sales increased by 23.3% to 103.127 billion yen compared to the same period the previous year and operating income increased by 27.7% to 10.727 billion yen. For their overseas instant noodles business which accounts for a sales distribution ratio of approx. 40%, their packet noodles “Ramen” and cup noodles “Instant Lunch” and “Yakisoba”, etc. have performed favourably in the U.S. and has performed strongly with an increase in revenue by 72%.

・For its full year plan, net sales is expected to increase by 12.0% to 405 billion yen compared to the previous year, operating income to increase by 22.7% to 36.5 billion yen and annual dividend to remain unchanged at 90 yen. Presumed exchange rate to USD is 122 yen. With the company assuming subjects of concern in their business performance forecast to be a continuance of a low-cost-oriented mindset and an awareness to safeguard lifestyles by consumers in the F&B industry, the tightening of consumers’ purse strings due to an intensification of inflation in Mexico and the U.S. is becoming an advantage to their overseas instant noodles business.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: