|

Report type: Weekly Strategy |

“The Bank of Japan’s Fixed-Rate Purchase Operations and the Yen Depreciation Market, and the Rise in Demand for Travel & Leisure”

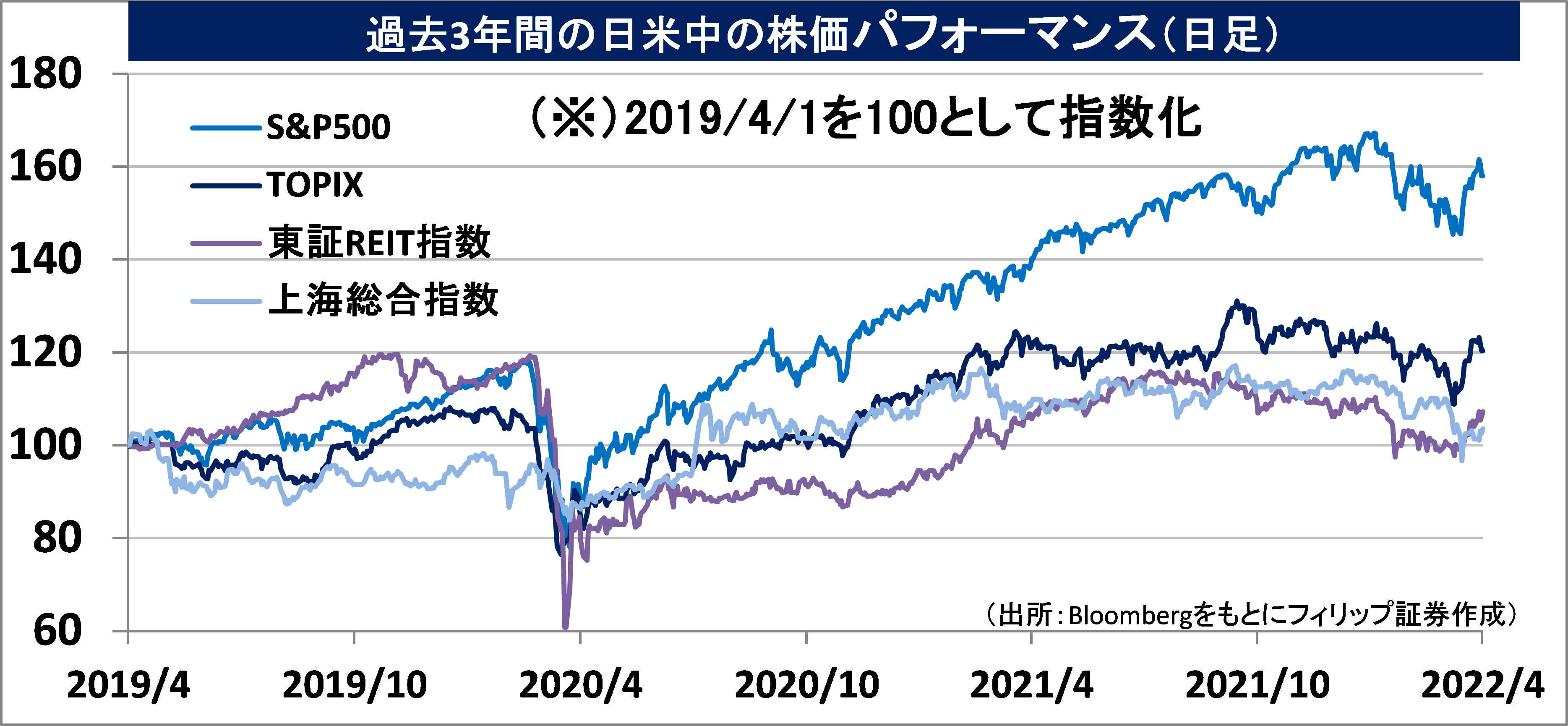

While the long-term interest rate was being adjusted by the Bank of Japan to shift within a fluctuation range of “about 0% and +-0.25%”, temporary measures known as the “fixed-rate purchase operations for consecutive days” were implemented for 3 days between 29th-31st March which made unlimited purchases of the 10-year Japanese government bonds at a yield of 0.25%. Due to the increase in the difference between the Japanese and U.S. long-term interest rates following the increase of the U.S. 10-year government bond yield to close to 2.5% as well as the growing observation of implementing multiple large interest rate increases of 0.5% on policy interest rates by the U.S. FRB, on the 28th, the depreciation of the yen against the dollar progressed to a level of 125 yen to 1 USD since August 2015. Regarding the yen depreciation, perhaps it was also supported by concerns of a current account deficit becoming commonplace for Japan, which relies on thermal power generation as a result of persistent skyrocketing energy prices due to the drawn-out Russian invasion of Ukraine.

Regarding whether there will be a stronger forecasts of large interest rate increases by the FRB due to the confirmation of a strained labour market from the U.S. employment statistics announced on 1/4, and whether Japan’s current account balance and trade balance for February announced on 8/4 will spur concerns of falling to a country with a current account deficit, etc., there will likely be attention on the trends of both the WTI crude oil futures market and the U.S. bond market. As a stock that will benefit from the depreciation of the yen, we can consider Nintendo (7974), which as a high cash holding ratio in foreign currency denominations from the planned release of “Nintendo Switch Sports” on 29/4, and on the other hand, as a stock that will benefit from a yen appreciation in the direction of keeping an eye on a reversal to a yen appreciation, there is Nitori Holdings (9843), which imports and sells overseas-produced products in Japan.

The semi-emergency coronavirus measures were lifted for all prefectures in Japan on 21/3 and it appears that there has been an increase in expectations of a recovery in travel and leisure demand. Regarding COVID-19, although progress in its replacement to the Omicron subvariant “BA.2” and the implementation of a large-scale city-wide lockdown in China’s Shanghai City are source material for concern, if the strain on hospital beds can be avoided from the popularisation of added vaccinations, perhaps it would not hinder economic reopening and normalisation.

In addition to those related to travel, such as the use of airplanes and hotel accommodations, etc., there will likely be consideration on the selection of stocks to buy from the perspective of leisure as well. In the U.S. market, similar to the near-10% increase in stock price of Canada’s womens casual sportswear giant Lululemon Athletica the day after announcing their strong business results forecast on 29/3, there will likely be attention on outdoor-related sports and fashion towards the reopening of the economy in Japan as well. Perhaps those that would match well with outdoor would be the competition shoes, sneakers and competition wear Asics (7936); Uniqlo’s Fast Retailing (9983), which is also strong in casual sportswear; the comprehensive outdoor Snow Peak (7816), such as automobile camping; as well as Kyoritsu Maintenance (9616), which has been popular for its free “Yorunaki Soba” at their accommodation hotels (Dormy Inn) after an excursion.

In the 4/4 issue, we will be covering Sumitomo Seika Chemicals (4008), Ibiden (4062), Nippon Denko (6330)and Nitori Holdings (9843).

・Established in 1944 via joint investment between Sumitomo Chemical (4005) and Taki Chemical (4025). Sumitomo Chemical currently owns 30%. Operates 3 mainstay businesses, which are absorbent resins, where its strength is in those used for paper diapers; functional chemicals; and gases and engineering.

・For 9M (Apr-Dec) results of FY2022/3 announced on 3/2, net sales increased by 11.9% to 84.234 billion yen compared to the same period the previous year and operating income decreased by 14.1% to 6.556 billion yen. Despite an increase in revenue and operating income in functional chemicals as well as gases and engineering, absorbent resins which account for 67% of net sales increased in revenue by 13.6%, however, the increase in distribution expenses and prices of raw materials and fuel have affected, which led to a 51.5% decrease in operating income.

・Company revised its full year plan upwards. Net sales is expected to increase by 11.4% to 115 billion yen compared to the previous year (original plan 109 billion yen) and operating income to decrease by 20.8% to 8 billion yen (original plan 7 billion yen). In the Chinese market, an alleviation of the burden of raising children in households with children was announced in the “National People’s Congress”, and strong performance is predicted in the paper diapers market. Also, on 31/3, Japan’s Ministry of Economy, Trade and Industry announced a policy on the stable supply of essential goods. The policy which advances the domestic production of gases for semiconductor manufacturing up to 2025 will likely be beneficial.

|

Ibiden Co., Ltd. (4062) 6,020 yen (1/4 closing price) ・Founded in 1912. Operates the electronics business such as printed circuit boards and package substrates, the ceramics business involving the environmental related, special carbon, fine ceramics and ceramic fibre products, and other business such as those related to construction materials, resins and equipment construction, etc. ・For 9M (Apr-Dec) results of FY2022/3 announced on 4/2, net sales increased by 30.2% to 299.2 billion yen compared to the same period the previous year and operating income increased by 98.9% to 54.4 billion yen. While the exhaust system components market in the automobile industry is tough for the time being due to the global semiconductor shortage, for the semiconductor and electronics components market, in addition to the strong PC market, there has been growth in the server market for data centres. ・For its full year plan, net sales is expected to increase by 23.7% to 400 billion yen compared to the previous year and operating income to increase by 61.8% to 62.5 billion yen. While the sales distribution ratio of those for the American Intel accounts for 36% in FY2022/3, since products from the American Intel have been popular in the domestic retail market for CPUs, which are responsible for the brains of a PC, due to the high performance of its latest model, as well as products from its competitor, the American Advanced Micro Devices, having increased prices due to the global semiconductor shortage, the market share has recovered to a level of that since 4 years ago. |

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: