The US-North Korea summit scheduled for 6/12 had been cancelled. In his letter to Chairman Kim Jong Un on 5/24, President Trump stated that “it is inappropriate, at this time, to have this meeting”.

In addition to national security adviser Bolton’s appeal to North Korea to adopt the “Libyan model” seeking immediate and unconditional abandonment of nuclear weapons development, VP Pence’s remark on 5/21 that North Korea “may end like Libya” greatly angered the North Koreans. North Korea’s vice-foreign minister Choe Son-hui strongly warned of a “nuclear showdown”, with both countries escalating their war of words. As a result, we expect the situation involving North Korea will become tense again.。

On the other hand, Kim Kye Gwan, 1st vice-foreign minister of North Korea, stated on 5/25 that “we have the intent to sit with the US side to solve problem(s) regardless of ways at any time”. There are views that North Korea holds the initiative, and while short-term solutions look remote, the route to denuclearization is not completely closed as yet. Despite the suspension of the talks, the stock market had remained stable, and the impact may be limited. However, it is necessary to follow developments closely including future response of Japan, China and South Korea.

Market focus seems to be on the US automotive import tariff increase, US-China trade negotiations and US long-term interest rates, etc. Uncertainty has surfaced again, and Japanese stocks are expected to face price escalation resistance in the meantime. Using security concerns as an excuse, the Trump administration is considering raising the 2.5% customs duty on passenger cars to 25%. There are views that imposing this customs duty may be difficult, but as the automotive industry has a wide array of supporting industries, there is concern about the impact on the world economy especially those of Japan and Europe. The third round of US-China trade talks will be held in China from 6/24. The US has temporarily suspended tariff imposition on China, but commerce secretary Ross, who has advocated tariff hikes on steel and aluminium, and who takes a hard line on China, will be visiting China. There is therefore a possibility that a trade war might reignite. Meanwhile, in response to the FOMC minutes, US interest rates had declined, but depending on the economic indicators, there is still the possibility of interest rates rising together with higher USD occurring. We need to pay close attention to US economic indicators such as business confidence, housing and employment situation.

In the 5/28 issue, we will be covering TORIDOLL HD (3397), Tomoku (3946), Park24 (4666), Tokai Carbon (5301), Pigeon (7956) and MS&AD Insurance GHD (8725).

Selected Stocks

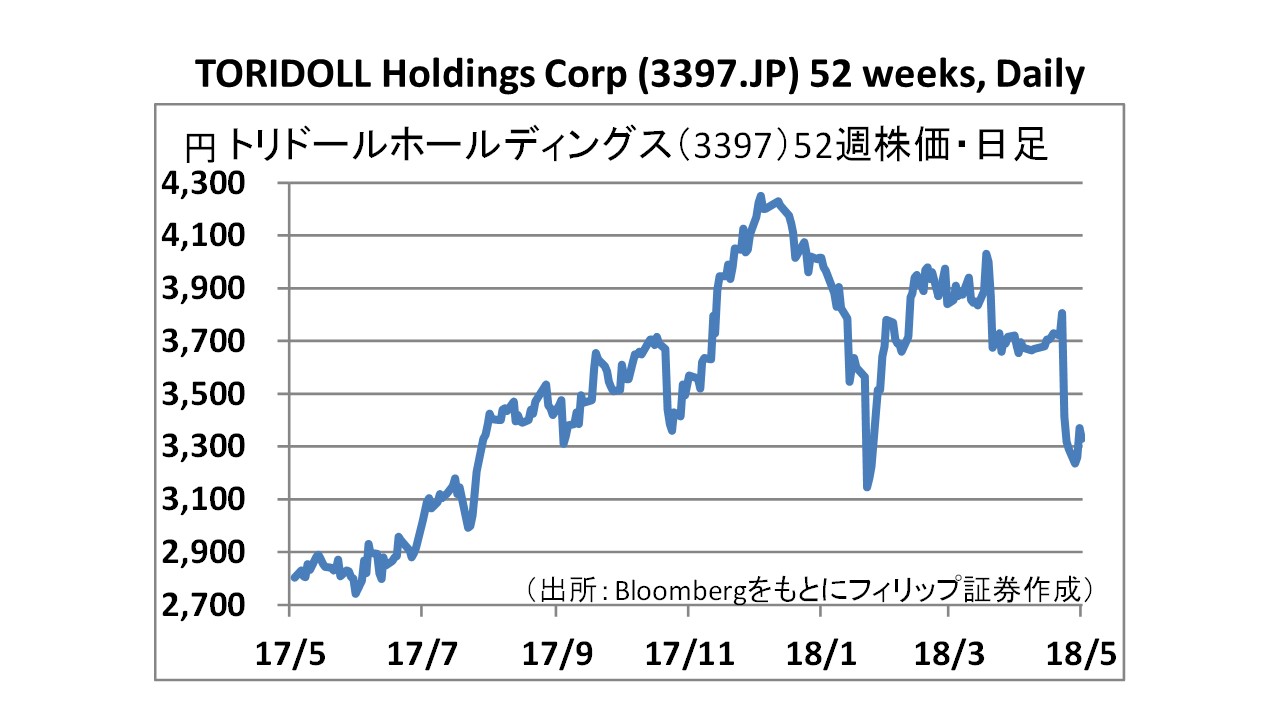

TORIDOLL Holdings Corporation (3397)

・Established in 1995. Conducts dining business through direct management and franchising. Has the following brands – “Marugame Seimen” selling Sanuki kamaage udon, “Toridoll Yakitori” focusing on yakitori family dining, soy sauce ramen specialty store “Marushoya”, yakisoba specialty store “Nagata Honjo”, and beauty and lifestyle brand “Sonoko”, amongst others. Has a total of 1,211 stores in Japan and overseas.

・For FY2018/3, net sales increased by 14.5% to 116.504 billion yen compared to the same period the previous year, operating income decreased by 11.4% to 7.635 billion yen, and net income decreased by 17.2% to 4.665 billion yen. Sales had been increasing steadily with those of existing Marugame Seimen stores growing steadily for the 43rd consecutive month in comparison with the same month the previous year. However, profit declined due to increasing personnel expenses, outsourcing expenses and forex losses.

・For FY2019/3 plan, net sales is expected to increase by 31.5% to 153.213 billion yen compared to the previous year, operating income to increase by 29.2% to 9.865 billion yen, and net income to increase by 39.7% to 6.515 billion yen. The company’s announced mid-term management plan’s targets are: FY2021/3 net sales of 212.306 billion yen, operating income of 15.722 billion yen, and net income of 10.943 billion yen.

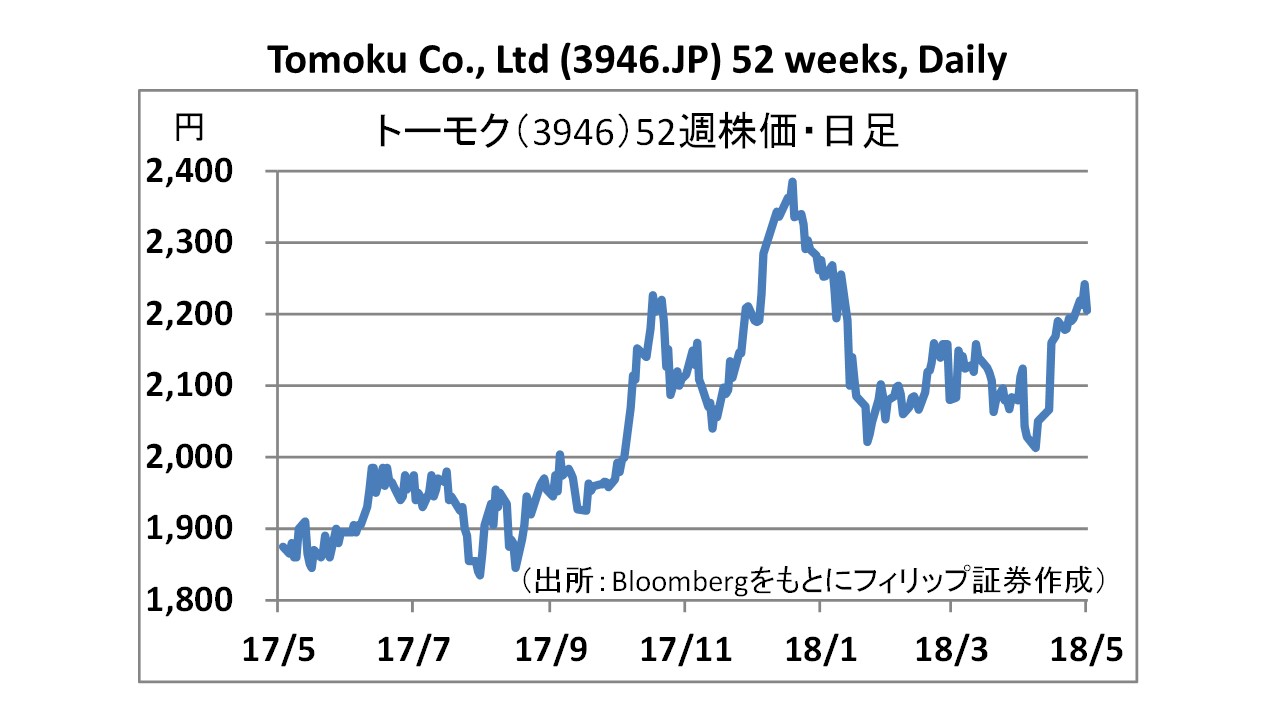

Tomoku Co., Ltd (3946)

Tomoku Co., Ltd (3946)

・Established in 1949 as “Toyo Wood Products Co., Ltd”. A general packaging manufacturer handling corrugated boards, housing, transportation and warehousing. Besides manufacturing and selling corrugated sheet, corrugated packing containers and printed packaging, in the housing business that began in 1984, company also imports housing materials made in Sweden, and designs, constructs and sells detached houses using these materials.

・For FY2018/3, net sales increased by 6.2% to 161.514 billion yen compared to the same period the previous year, operating income decreased by 19.5% to 5.878 billion yen, and net income decreased by 14.4% to 3.87 billion yen. Production volume of mainstay corrugated boards increased due to increased demand in the processed food, mail order / home delivery sectors. However, profit declined due to soaring base paper prices. Housing sales were good owing to expansion of sales channels to the younger generation.

・For FY2019/3 plan, net sales is expected to increase by 5.3% to 170 billion yen compared to the previous year, operating income to increase by 36.1% to 8 billion yen, and net income to increase by 29.2% to 5 billion yen. Company intends to pass on price increases in the corrugated board sector due to soaring raw material prices, and, in the housing sector, expand sales of “HUS ECO ZERO” housing compatible with ZEH which emphasizes energy conservation.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: