|

Report type: Weekly Strategy |

“Stocks With Low Ratio of Margin Balance, the Export of Agricultural Products and Plastic Resource Circulation”

As mentioned in the previous issue (31st January 2022), the “ratio of margin balance”, which is obtained by dividing the margin debt balance of transactions that use the Tokyo Stock Exchange system by the margin selling balance, rose to a high level of 5.7 times on the basis of 21/1 last since Mar-Apr 2018. Despite it declining to 5.0 times on the 28th, it remains at a high level. For an actual increase and improvement in supply and demand of the overall Japanese stock market, it appears that there is a need for further decline. On the other hand, judging from individual stocks, BASE (4477), which was one of the stocks from “Selected Stocks” in the previous issue, declined to 1.79 times on the 21st. Toei Animation (4816) as well, which has been under 1.0 times since April last year onwards, was 0.49 times on the 21st with its margin selling balance greatly exceeding its debt balance. Since settlements have to be made by the final deadline 6 months after new commitments in system margin trading, there is an aspect where stocks with “more selling balance than buying balance” which have a declining ratio of margin balance while followed by a fall in market price or that is less than 1.0 times, have a tendency to have its market price reverse to increase due to some sort of trigger. The stock price of both stocks increased swiftly on 1st and 2nd February.

For the Nikkei average, the unsettled buying balance of arbitrage (unresolved balance of spot purchases in a forward selling and spot buying position) and the unsettled selling balance of arbitrage (unresolved balance of spot sales in a forward buying and long sales position) shifted in low levels. Also, changes in the ratio of margin balance of Nikkei average-linked double inverse and leveraged ETFs will likely be of reference when looking at supply and demand trends concerning the Nikkei average.

The annual export value of agricultural, forestry, fishery and food produce for 2021 announced by the Ministry of Agriculture, Forestry and Fisheries on 4/2 increased by 25.6% compared to the previous year to 1.2385 trillion yen, which greatly broke the government’s goal of 1 trillion yen. This was greatly contributed by strong sales in new markets involving sales from electronic commerce (EC) and those for retailers, etc. which adapted to the change in global consumer demand after the COVID-19 disaster. Furthermore, as of late, there has been progress in various regions across Japan involving initiatives that create new products that make use of local agricultural produce by partnering with a wide range of industries with a focus on foodstuff manufacturers and the Ministry of Agriculture, Forestry and Fisheries. The B2B e-commerce Raccoon Holdings (3031) has partnered with the Sabae Chamber of Commerce and Industry from Fukui Prefecture in participating in the planning of the cross-border EC business, “Cross Border Sabae”, which supports the overseas sale of local products. There will likely be attention on the increase in collaboration of cross-border EC and foodstuff manufacturers or supermarkets geared towards regional revitalisation.

In the Cabinet meeting on 14/1, the Japanese government decided on the cabinet order that 1st April 2022 be the enforcement date for the “Act on Promoting Plastic Resource Circulation”, which reduces the usage of 12 articles of disposable plastic products, such as straws and hangers. Regarding the products to be reduced, it would demand measures, such as having consumers confirm their intention on its necessity as well as replacing them with materials, such as paper or wood. In addition to it benefitting the paper and pulp industry, making it such that it newly recognises manufacturers and retailers in independently collecting used products will likely strengthen initiatives in recyclable plastics by chemical manufacturers as well.

In the 7/2 issue, we will be covering Sojitz (2768), NGK Spark Plug (5334), ACSL (6232) and Enex Infrastructure Investment Corporation (9286).

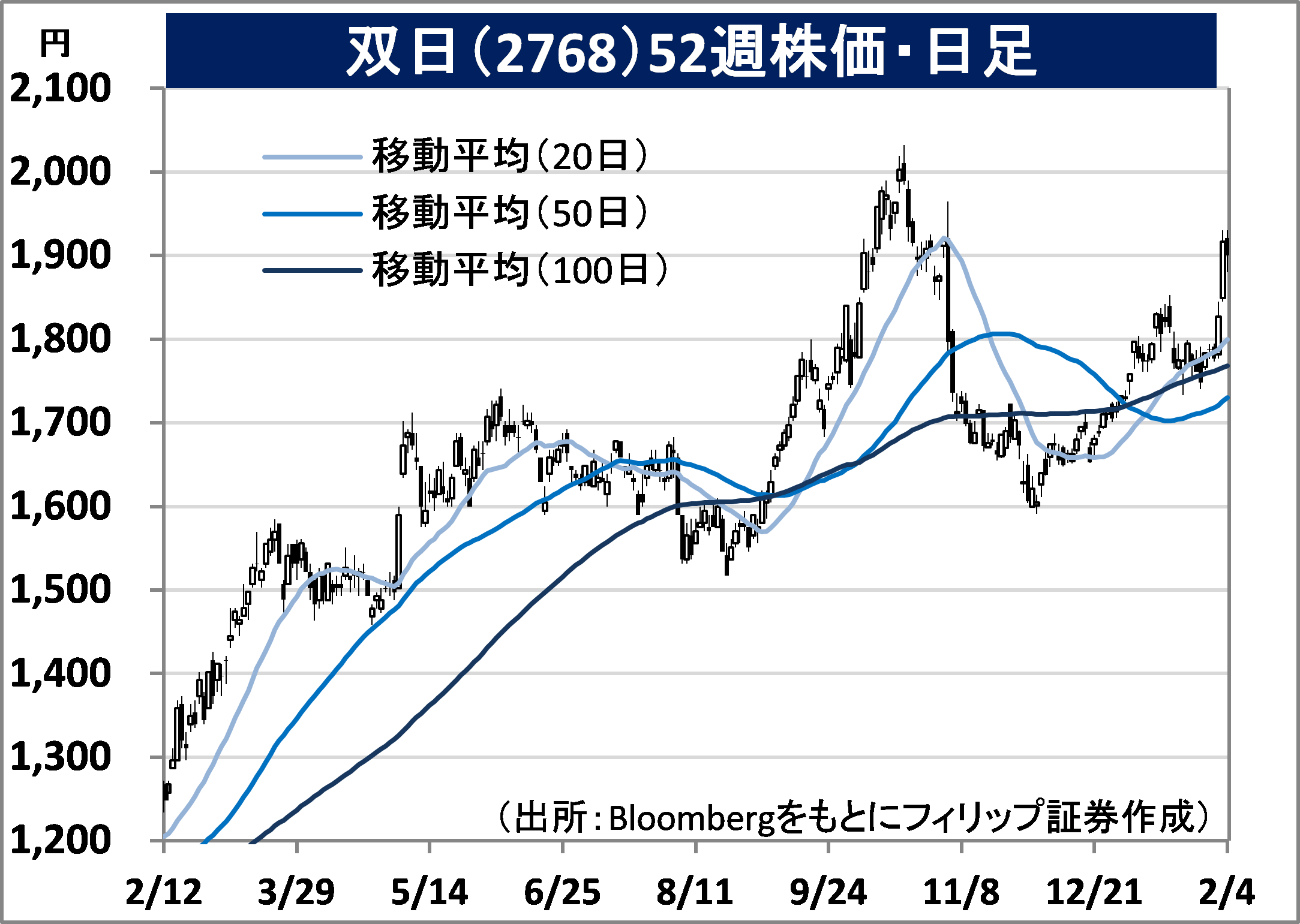

・Nichimen and Nissho Iwai integrated in 2003. Operates 9 main business segments, which are automobiles; the aviation industry and transport; machines and healthcare infrastructure; energy and social infrastructure; metals and resources; chemistry; food and agriculture; and retail and lifestyle, etc.

・For 9M (Jan-Sep) results of FY2022/3 announced on 2/2, earnings increased by 33.5% to 1.5485 billion yen compared to the same period the previous year and operating income increased by 3.5 times to 84.975 billion yen. The increase in coal price, increase in prices of precious metals, increase in quantity handled included in recycling, increase in methanol price and transactions of synthetic resins as well as the increase in retail units in the overseas automobile business have contributed to business performance.

・Company revised its full year plan upwards. Net income is expected to increase approximately by 3.0 times to 80 billion yen compared to the previous year (original plan 70 billion yen) and annual dividend to increase by 48 yen to 58 yen (original plan 45 yen). The forecast was raised following the sudden rise in coal price. The company has partnered with Vietnamese dairy product giant Vinamilk and looks to embark on the production of beef of quality on par with those for the Japanese market. Domestic beef has a high degree of contribution to the increase in export prices of agricultural, forestry, fishery and food products and is popular overseas.

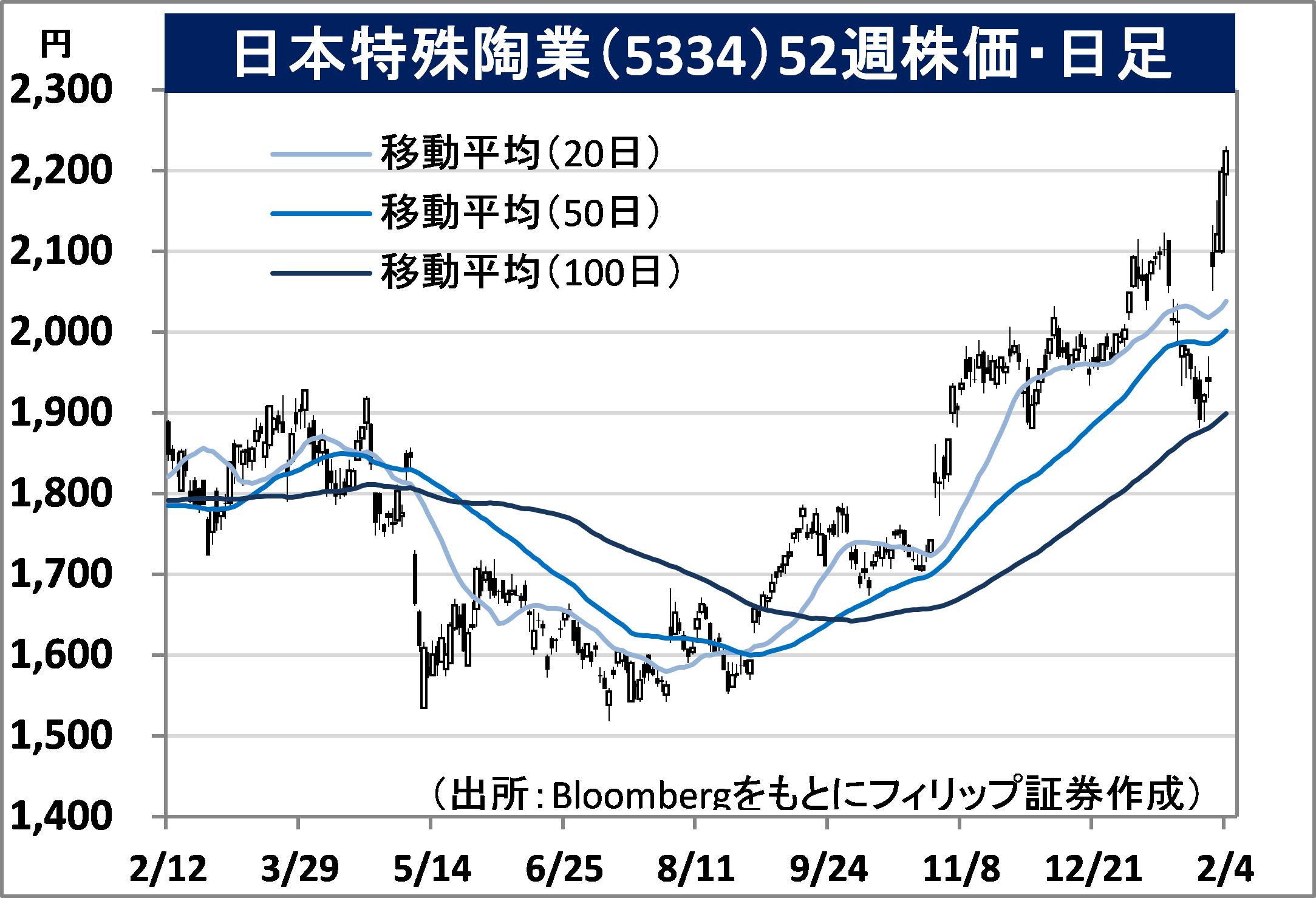

・The spark plug section separated from NGK Insulators (5333) in 1936. Operates 3 businesses, which are their mainstay “automobiles” such as spark plugs, “ceramics” involving semiconductor equipment, and “new businesses” which include the company Morimura SOFC Technology.

・For 9M (Apr-Dec) results of FY2022/3 announced on 31/1, sales revenue increased by 16.7% to 358.333 billion yen compared to the same period the previous year and operating income increased by 53.1% to 54.768 billion yen. Despite the increase in operating deficit in new businesses, for automobiles, sales of products used for repair mainly in Europe and North America has performed well. For ceramics, those for semiconductor equipment and machinery tools for those related to automobiles have performed strongly.

・Company revised its full year plan upwards. Sales revenue is expected to increase by 14.4% to 489 billion yen compared to the previous year (original plan 482 billion yen) and operating income to increase by 70.9% to 81 billion yen (original plan 68.5 billion yen). Furthermore, they are taking an aggressive stance by raising overall return propensity by announcing a 10 billion yen upper limit in stock buyback and an increase in annual dividend by 62 yen to 102 yen (original plan 96 yen). It appears that the global reduction in automobile production due to supply constraints is becoming an advantage due to the increase in demand for replacing plugs following the boom in the second-hand vehicles market.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: