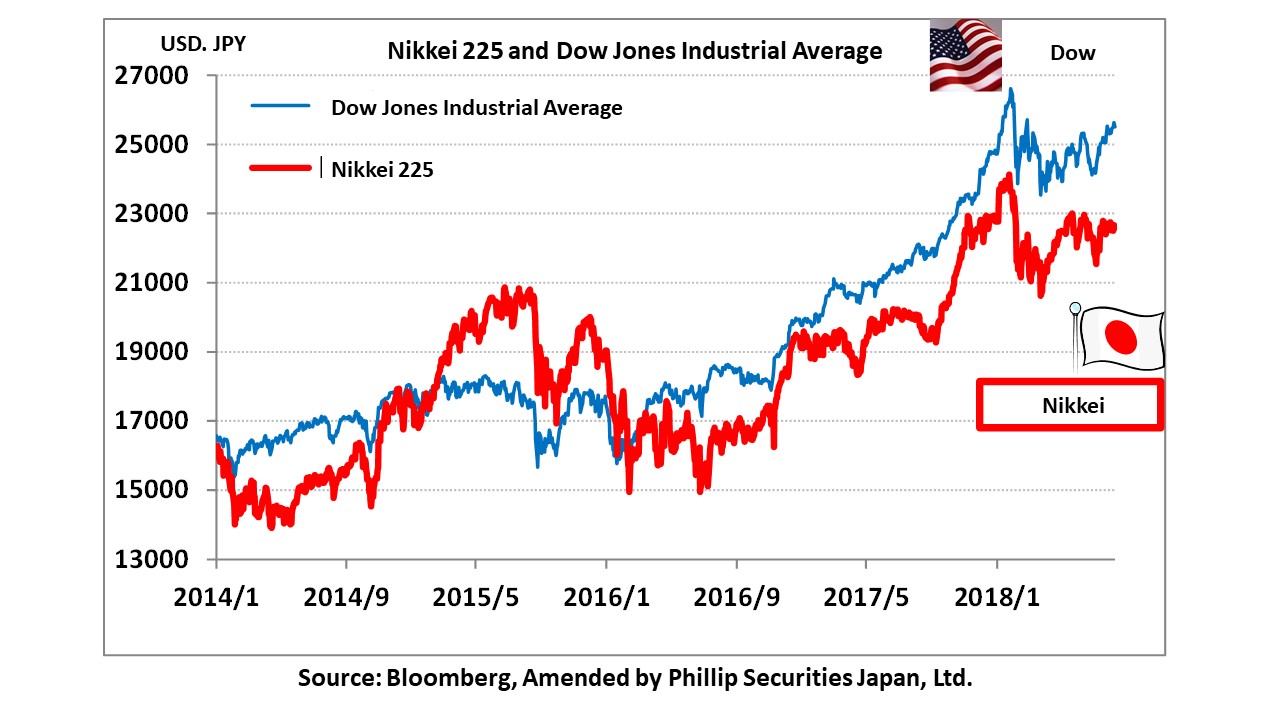

Japanese stocks are in a stalemate situation over concerns about trade frictions, especially that between the US and China. Beginning with the US, corporate earnings for the Apr-June period expanded globally, and rate of net income increase of domestic listed companies seems to have increased more than 20%. Meanwhile, the Nikkei Average is currently moving within a narrow range of between 22,400 and 22,800 points.

Komatsu (6031), a major stock related to China, announced an 86% increase year-on-year in its operating profit to 96 billion yen for the Apr-June period. Despite this record-breaking earnings announcement which has exceeded market expectations, its stock price continued to struggle. Toyota Motor (7203) has also announced record earnings, but has kept its FY2019/3 plan unchanged with expected decrease in income and gains. The company has announced that, with the imposition of 25% additional tariffs on automobiles and related parts by the US, exports from Japan alone would incur an additional tax burden of 470 billion yen. At present, the shadow cast by this trade friction is hovering over the market, and investors are extremely cautious as a result.

On the other hand, we can also focus on business opportunities for Japanese companies as the trade war intensifies. As countermeasures against trade friction, China is planning monetary easing measures and expansion of infrastructure investment. On its part, in addition to considering additional tax cuts, the US, besides investments in domestic infrastructure, has also announced, as a countermeasure against China, 113 million dollars (about 12.5 billion yen) worth of investments in new technology, energy and infrastructure in the Indian Ocean region. However, there are views that as part of its “One Belt One Road” strategy, China will be investing a maximum of 1.3 trillion dollars (about 144 trillion yen) over the next 10 years on trunk roads, railways, pipelines, power plants, etc. Although Caterpillar (CAT) has the top share of heavy machinery in the world, there is also a possibility that alternate demands may switch to Komatsu (6301) and Hitachi Construction Machinery (6305).

The US is also becoming increasingly wary of advancing high-technologies in China. US sanctions against ZTE, a leading Chinese telecom equipment manufacturer, are still fresh in our memory. The US-China trade war is also strongly inclining towards a fight for high-tech supremacy. Advanced technology is indispensable for communication, data and military usage. Such technologies also cannot be overlooked from the security viewpoint. Chinese technological progress is remarkable. For example, China’s memory semiconductor company, YMTC, has announced the launch of second generation 32-stages 3D NAND flash memory. China is actively pursuing construction of semiconductor factories. There are therefore possibilities for business opportunities for Japanese semiconductor-related companies to expand further. We should therefore pay attention to the activities of semiconductor manufacturing equipment makers like Tokyo Electron (8035). We may therefore also like to bear in mind these silver linings as a result of the trade frictions.

In the 8/13 issue, we will be covering Pressance Corp (3254), Sushiro Global HD (3563), Daikin Industries (6367), Brother Industries (6448), Nitto Denko Corp (6988) and Tokyo Electron (8035).

Selected Stocks:

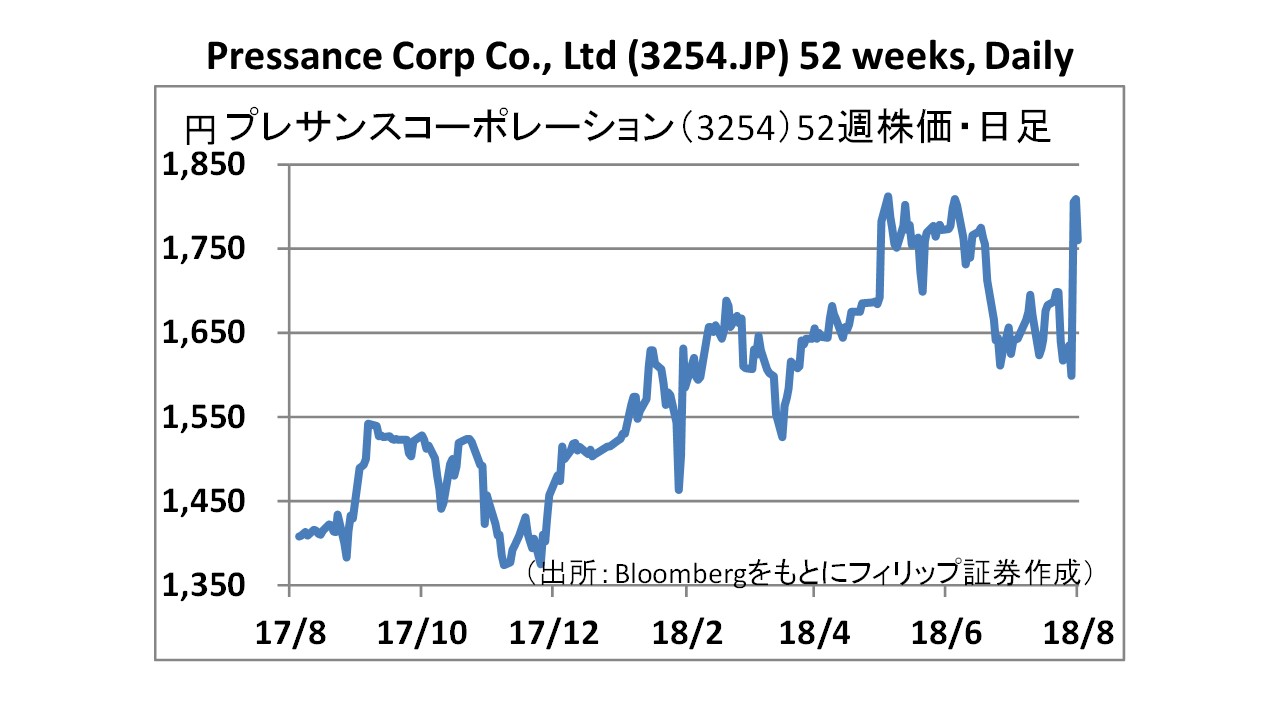

Pressance Corporation Co., Ltd (3254)

・Established in 1997. Plans, develops and sells one-room apartments (investment apartments rented out mainly to singles) and family apartments (apartments intended for family use). Business operations mainly in Kansai, Tokai, Kanto and Okinawa regions. Also manages rental and leasing of one-room apartments.

・For 1Q (Apr-June) of FY2019/3, net sales increased by 2.3 times to 81.514 billion yen compared to the previous period, operating income increased by 2.8% to 19.274 billion yen, and net income increased by 2.9 times to 13.111 billion yen. Sales of family apartment complex, “Legend Biwako”, and one-room apartment complex, “Pressance Osaka Fukushima Shieru”, were strong. Rental real estate operation is also doing well.

・For FY2019/3 plan, net sales is expected to increase by 13.7% to 152.471 billion yen compared to the previous year, operating income to increase by 20.5% to 24.541 billion yen, and net income to increase by 17.3% to 16.132 billion yen. As of the end of 2018/6, the main apartment sales business consisting of actual sales and expected revenue bookings has already secured 93.1% of company’s sales plan.

Sushiro Global Holdings Ltd (3563)

・Founded in 1984 as “Sushi Taro”. Developing conveyor-belt sushi shops domestically through direct management via the “Sushiro” brand. Overseas, developing conveyor-belt sushi shops through direct management in Korea. Purchasing, in-store cooking, utilization of IT systems are its main source of competitiveness. As of the end of 2018/6, there are a total of 512 stores consisting of 502 domestic stores and 10 overseas stores.

・For 3Q (2017/10-2018/6) of FY2018/9, net sales increased by 11.5% to 128.044 billion yen compared to the same period the previous year, operating income increased by 35.9% to 8.918 billion yen, and net income increased by 36.7% to 5.957 billion yen. Besides sweets, discount fairs had also contributed.

・Because of strong sales at existing stores and successful cost reduction efforts, company has revised its 2018/9 plan upwards. Net sales is expected to increase by 11.9% to 175.0 billion yen compared to the previous year (original plan 169.361 billion yen), operating income to increase by 26.0% to 11.6 billion yen (original plan 9.939 billion yen), and net income to increase by 12.2% to 7.8 billion yen (original plan 6.62 billion yen).

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: