Report type: Weekly Strategy

“Reskilling budget of 1 trillion yen over 5 years, capital investment proceeding in Japan”

Delivering a policy speech at an extraordinary session of the House of Representatives on 3/10, PM Kishida announced that he would expand “investment in people” measures such as “reskilling” (relearning) for employment in growth sectors, and invest 1 trillion yen over five years. This is a significant increase from the “Basic Policies for Economic and Fiscal Management and Reform (Bold and Firm Policy)” approved by the Cabinet four months ago, which called for 400 billion yen to be invested over three years. Reskilling is the process of relearning to enable working adults to take on new jobs or to acquire job-related skills that will be needed in the future, and differs from “recurrent” study, which is the process of relearning at a university or other institution of higher education on one’s own. This is due to the lack of digital human resources to implement and establish digital transformation (DX) amidst the ongoing DX of society.

In the 13 June, 2022 issue of our weekly newsletter, we had mentioned KIYO Learning (7353), which focuses on “investing in people” with its “Studying” online certification course for individuals, and Business Breakthrough (2464), which provides management guidance and human resource development education. Even while both company stock prices are down from early June, there are still many small growth companies related to reskilling. As the flow of money and other procedures related to the increased government budget from four months ago become clearer, the stock prices of undervalued stocks are expected to rise.

Canon (7751) reportedly is planning to build a new semiconductor equipment plant in Tochigi Prefecture. Aiming to start operations in spring 2025, and with a total investment of over 50 billion yen, the company plans to increase production of exposure systems used to form circuits, the core process of semiconductors. At the same time, according to the Nihon Keizai Shimbun, Yaskawa Electric Corporation (6506) will establish a new plant in Japan in 2027 for key components that improve the energy-saving performance of home appliances and other products, and expects to invest 50 to 60 billion yen. The objective is said to be to focus on increasing domestic production and reduce the ratio of Chinese-made parts. Regarding the procurement of parts from China, Daikin Industries (6367) plans to build a supply network during FY2023 that will enable it to produce air conditioners without Chinese-made parts in the event of an emergency. In addition, Nitori Holdings (9843) had announced its withdrawal from the US at the end of September. Citing high tariffs on imports of goods from China, as well as soaring container freight costs as reasons for the move, the company said it would reallocate funds and human resources to the East and Southeast Asian regions.

We are seeing a partial return of factory production to Japan amid the weakening of the yen in the forex market. In addition, there appears to be a “China plus one” trend of reassessing investment in China while seeking other alternative investment locations. In such a case, we can expect a greater shift towards Japan’s domestic market. The BOJ’s Tankan survey released on 3/10 also showed an improvement in firms’ outlooks for price inflations as well as sales price hikes. The investment environment in Japan is therefore expected to improve further.

In the 11/10 issue, we will be covering Nakayama Steel Works (5408), Anicom Holdings (8715), Konoike Transport (9025), and Benesse Holdings (9783).

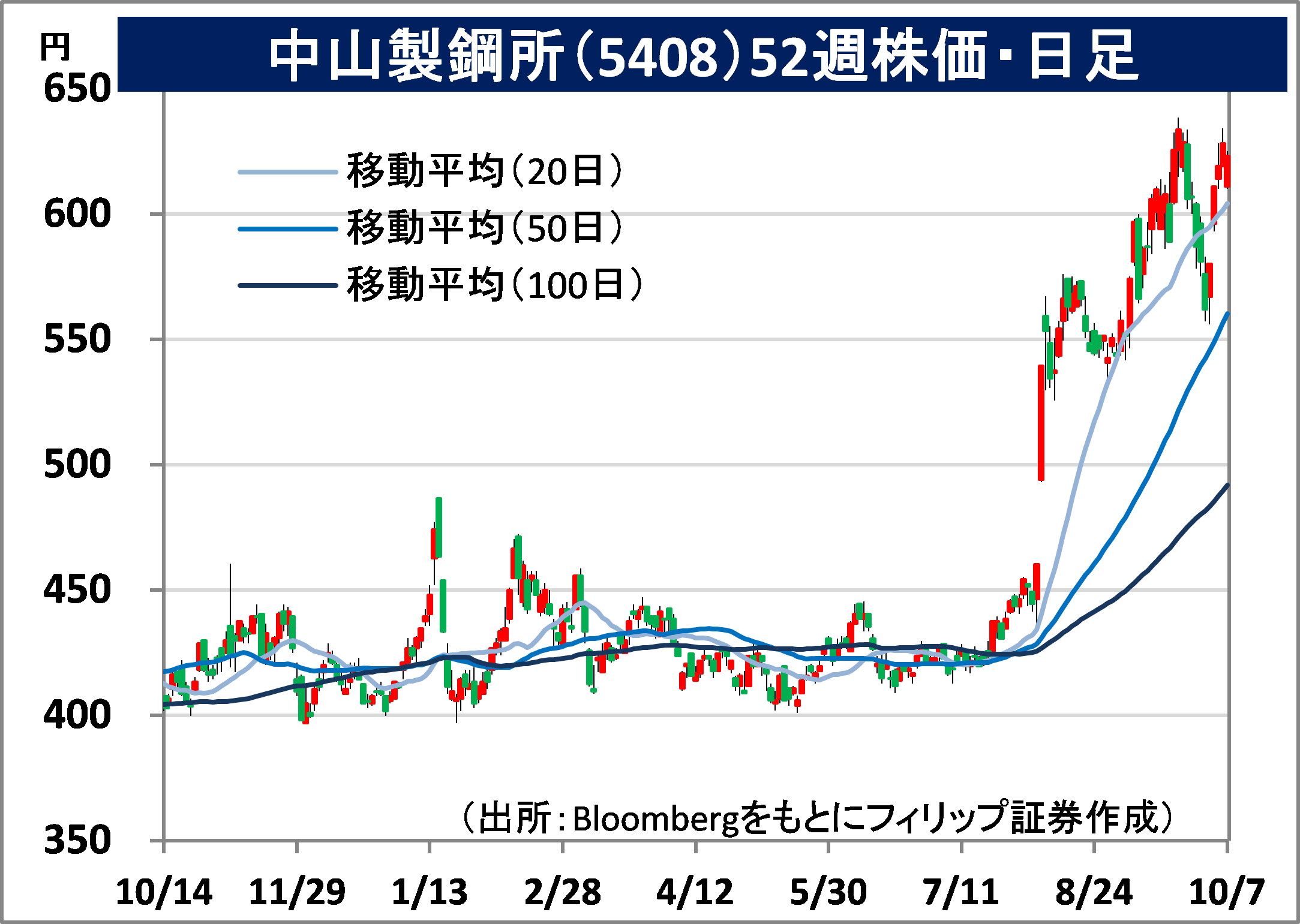

Nakayama Steel Works, Ltd (5408) 625 yen (7/10 closing price)

・Founded in Osaka in 1923 by Etsuji Nakayama. A long-established manufacturer of steel sheets, bars and wires. Affiliated with Nippon Steel Corp (5401). Strong in rolling technology developed through a combination of in-house electric furnaces and blast furnaces. First in the world in industrial production of fine-grain hot-rolled steel.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 4/8, net sales increased by 34.5% to 47.796 billion yen compared to the same period the previous year, and operating income increased 3x to 3.275 billion yen. Improved electric furnace material costs while increasing electric furnace production by 12% YoY as part of industry “decarbonization”. Steel spreads improved as higher prices for main raw material scrap and steel billets were passed on to steel sales prices.

・For its full year plan, net sales is revised downward to 198.0 billion yen (original plan 200.0 billion yen), up 18.8% YoY, but operating income is raised to 11.5 billion yen (original plan 6.5 billion yen), up 58.6% YoY. Company is expecting higher steel selling prices and lower prices for main raw materials compared to the initial plan. Annual dividend is increased by 4 yen to 20 yen. In April 2021, company signed a comprehensive business alliance agreement with Chubu Kohan (5461), an electric furnace plate specialist. Company is expected to gain an advantage in the restructuring of the electric furnace industry.

Anicom Holdings, Inc (8715) 552 yen (7/10 closing price)

・Established in 2000. Core business is damage insurance centering on pet insurance, which has the largest market share in Japan. Other businesses include veterinary hospital support services, insurance agency services, and research and clinical services in the field of veterinary medicine.

・For 1Q (Apr-Jun) results of FY2023/3 announced on 5/8, ordinary income increased by 5.2% to 13.953 billion yen compared to the same period the previous year, and ordinary profit increased by 11.5% to 778 million yen. The number of insurance policies had increased by 2.0% from the end of the previous period due to increase in demand for pet ownership. In comparison, the expense ratio based on premiums earned improved by 3.3 percentage points YoY to 94.5%, mainly due to an increase in the number of applications for “Dobutsu Kenkatsu”.

・For its full year plan, ordinary income is expected to increase by 7.5% to 57.0 billion yen compared to the previous year, and ordinary profit to increase by 15.3% to 3.65 billion yen. Company is the largest pet insurance company in Japan, with a market share of over 50%. According to the company, the pet insurance subscription rate in Japan is just over 10%, low compared to Europe and the US. The market is therefore expected to grow as pets live longer. Company’s stock price continues to weaken in reaction to the surge in stay-at-home demands due to the Covid-19 pandemic. However, it is expected to recover as a result of growth expectations.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: