Report type: Weekly Strategy

“Renewable Energy to Become a Pillar of Regulatory Reform in the Suga Administration”

With the U.S. presidential election drawing close, the Japanese stock market has been displaying a growing wait-and-see stance. The trading value of the TSE Section 1 also fell below 2 trillion yen consecutively over 9 business days from 12/10 to 22/10. In contrast to the stock market where watchful waiting continues, the characteristics of the Suga administration, whose slogan is regulatory reform, seems to be becoming more defined. There is a side to it which seems to bear resemblance to the regulatory easing demonstrated and promoted in the “structural reform without sanctuary” by the Koizumi administration, rather than the “growth strategy” which is the 3rd arrow in Abenomics, whose driving force was regulatory easing. In an interview in The Nikkei on 20/10, Kono, the Minister of Regulatory Reform, expressed that a thorough inspection will be carried out on existing systems towards the promotion of the use of renewable energy, and mentioned rolling out self-driving cars nationwide and drones limited to specific wards, standardising copyright rules involving the simultaneous transmission of broadcasting and on the internet, the digital storage of receipts, as well as abolishing the obligation for industrial physicians to be permanently stationed following the use of AI at nursing care sites.

Amongst them, it appears that the promotion of the use of renewable energy will become a major pillar of the regulatory reform. It is said that Prime Minister Suga will target for zero actual greenhouse gas emissions in 2050 at his first general policy speech scheduled for 26/10 after his appointment. From the amount of greenhouse gas emissions, such as CO2, etc., the aim is to make it zero in 2050 after deducting the amount which is absorbed by forests, etc. Firstly, this means that there will be a need to raise the composition ratio of renewable energy by revising the existing basic plan for energy, where the targeted composition ratio of renewable energy in 30 years is 22-24%. Secondly, if the emissions trading system is officially implemented in the future, we can also infer that it signifies that there will be a greater possibility of corporations in the forestry business who are able to contribute to the reduction of greenhouse gas emissions, such as Sumitomo Forestry (1911), who possesses forests accounting for approx. 1/900 of those in Japan’s

land, being able to hold credit.

With the transmission networks having capacity restrictions due to the country’s guidelines being allocated to coal-fired thermal power and nuclear power with priority, it was said in end June this year that via a cooperation between Mitsubishi Corporation (8058) and NTT (9432), who owns the entire country’s telephone exchange networks, their policy was to make an official entry into the renewable energy business by equipping with electric power production and supply networks in advance. Regarding this point, since this would allow any corporation including those making a new entry in the renewable energy business to fairly utilise power transmission and distribution facilities, since April this year, telecommunications business operators are obligated to legally separate their power transmission and distribution sections. In the future, there may be efforts to promote the use of renewable energy as a result of competition between NTT and power companies.

Also, regarding the standardisation of copyright rules involving the simultaneous transmission of broadcasting and on the internet, we can expect that the expansion of high quality programme content assets to the internet will serve as a trigger to review the low P/B ratio (price-to-book ratio) of the stock prices of terrestrial television station corporations.

In the 26/10 issue, we will be covering Resorttrust (4681), UACJ (5741), Kintetsu World Express (9375), and Nippon Television Holdings (9404).

・Established in 1973 in Nagoya. Handles the management and construction of membership-based hotels and golf courses, the retail of hotel membership, etc., and the medical business (including the retail of medical memberships and medical consulting), etc.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 7/8, net sales decreased by 40.4% to 23.416 billion yen compared to the same period the previous year, and operating income fell into the red from 2.442 billion yen the same period the previous year to (884) million yen. Due to the impact from the spread of COVID-19, the reduction and limitation in operating activities involving the sale of memberships and the closure of hotel block facilities have affected.

・For its full year plan, net sales is expected to decrease by 0.7% to 158 billion yen compared to the previous year and operating income to decrease by 45.9% to 6.3 billion yen. Although the effects of the COVID-19 catastrophe are persisting, it is predicted that the decrease in revenue will be small due to the sale of the “Yokohama Baycourt Club” membership, which opened for business in Sep this year. With restrictions on overseas travel due to the COVID-19 catastrophe, supported by the demand from the wealthy who are avoiding crowds but want to go out, there is a prominent trend in the increase in the price of memberships for resort clubs and golf courses in the outskirts of major cities such as Tokyo.

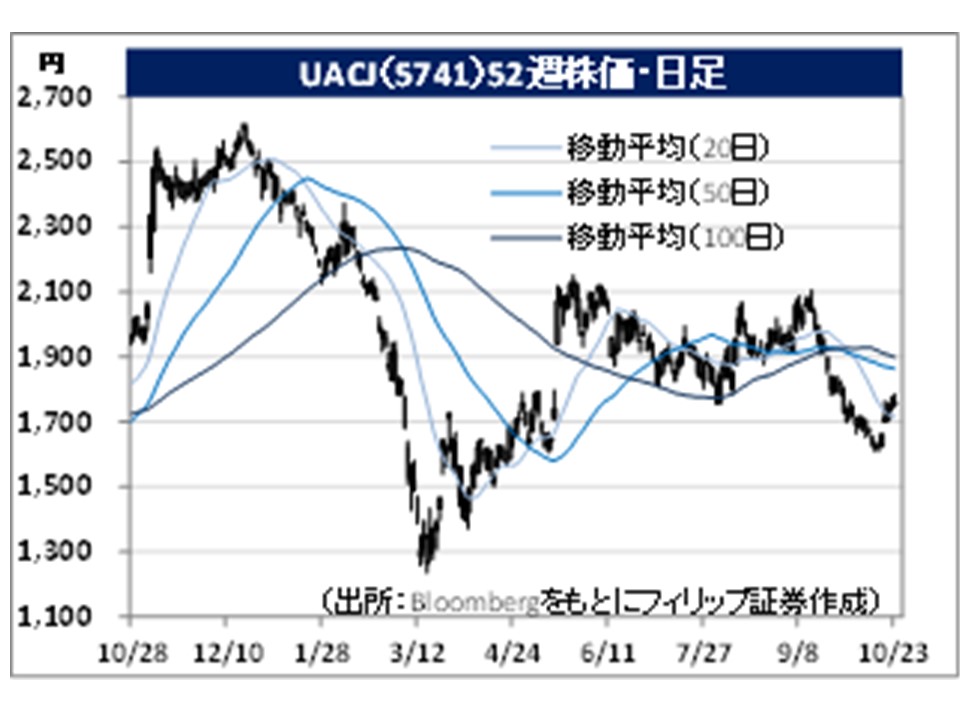

・Started from a business merger between Furukawa-Sky and Sumitomo Light Metal Industries in 2013. Furukawa Electric (5801) is their top shareholder with a shareholding ratio of 24.9%. Has the top production capability in Japan for aluminium rolling products and is 3rd in the world after the American Alcoa and Novelis.

・For 1Q (Apr-Jun) results of FY2021/3 announced on 6/8, net sales decreased by 16.6% to 133.3 billion yen compared to the same period the previous year and operating income fell into deficit from 1.311 billion yen to (575) million yen. Although sales in Thailand, etc. for canned materials for overseas performed well, the decrease in overall sales volume due to the COVID-19 catastrophe and the decrease in the price of aluminium base metal have affected.

・Their full year plan is undecided due to the present inability to reasonably calculate the effects from the COVID-19 catastrophe. They are targeting a 40% increase in their global production capability of aluminium plates by 2022 compared to 2019, and predicts a reinforcement in the capability of their Thailand factory by investing 39 billion yen. With the increase in environmental awareness from marine pollution by plastic trash, an increase in global demand for aluminium cans are predicted such as from progress in the switch by beverage companies from PET bottles to beverage cans that can be easily recycled, etc.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: