|

Report type: Weekly Strategy |

“Relaxation of border control measures, change in nuclear power policy, easing of semiconductor shortages”

Working remotely after testing positive for Covid-19 through a PCR test, PM Kishida held two virtual press conferences of great importance to Japan’s politics, economy, and society on 21/8.

First, the government will further relax its border control measures for Covid-19 from next month onward, raising the maximum number of people entering the country per day from the current 20,000 to 50,000, and allowing those who have completed the third dose of the Covid-19 vaccine to enter the country without undergoing pre-departure tests from their overseas locations. Furthermore, the government has decided to revise the current system for reporting total number of Covid-19 cases in order to reduce the burden on medical institutions and public healthcare centers.

Following these developments, share prices of travel-related stocks, including airline stocks such as Japan Airlines (9201) and ANA Holdings (9202), and department store stocks for which inbound spending is expected to increase, such as J. Front Retailing (3086), Isetan Mitsukoshi HD (3099), and Takashimaya (8233), soared from 23/8 onward. Kyoritsu Maintenance (9616), which operates “Dormy”, student and employee dormitories for foreign students and workers, is also continuing its upward trend.

Second, the policy after the Great East Japan Earthquake, which does not envision the construction of new nuclear power plants, was reversed, and instructions were given to consider the development and construction of next-generation nuclear power plants. In addition to this, aiming to secure power supply over the medium to long term, the government plans to increase the number of nuclear reactors to be restarted from the current maximum of 10 to a maximum of 17 after next summer. As a result, nuclear power plant-related stocks have been on the move since 24/8. TEPCO Holdings (9501), which has the Kashiwazaki-Kariwa No. 6 and 7 reactors, which are currently not operating but have passed the Nuclear Regulation Authority’s safety review, Sukegawa Electric (7711), which specializes in thermal control technology and has a strong track record in the nuclear power industry, Japan Steel Works (5631), which manufactures cast and forged steel components (shell flanges) for nuclear pressure vessels, Kimura Chemical Plants (6378), which handles nuclear fuel transportation containers, enrichment-related equipment, and radioactive waste treatment equipment, and Okano Valve Manufacturing (6492), which manufactures valves for nuclear power plants, are all in the limelight.

The persistent semiconductor shortage that has plagued various manufacturers of products from automobiles to smartphones appears to be easing. European automaker Volkswagen said on 28/6 that it will increase production of electric vehicles (EVs) in the second half of this year as a result of easing semiconductor shortages. In addition, according to Nikkei Asia, Samsung Electronics, the world’s largest semiconductor manufacturer by sales, has asked vendors in June to reduce shipments because of ballooning inventories. Increased capital expenditures by semiconductor manufacturers and softening demand due to the lockdowns of Chinese cities are factors that are apparently easing supply shortages of semiconductors in the supply chain. Businesses that have been having reduced profits due to shortages of parts may therefore have an opportunity to improve their performance.

In the 29/8 issue, we will be covering Lawson (2651), FUJIFILM Holdings (4901), Nichicon (6996), and Nintendo (7974).

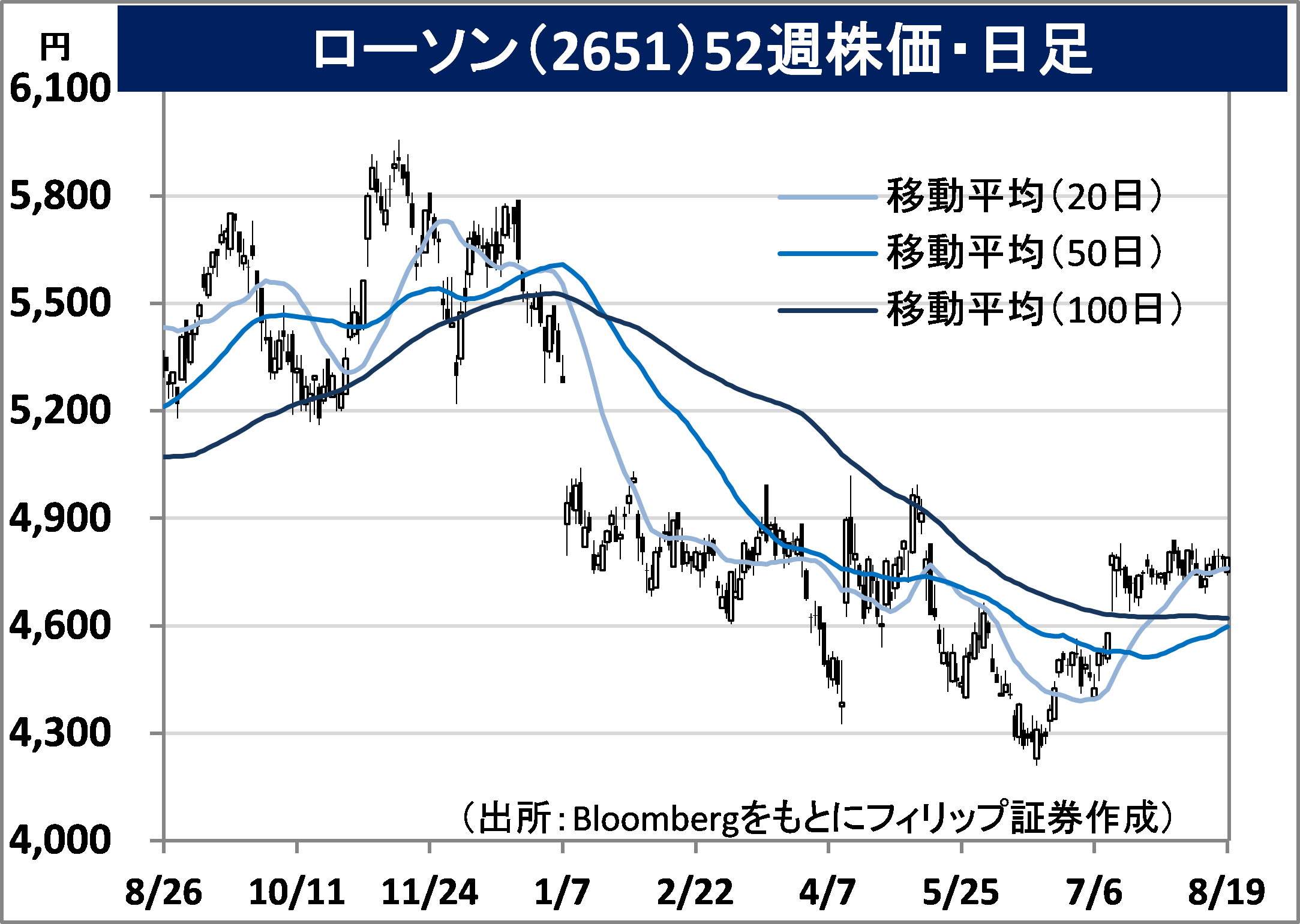

・Established in 1975. Subsidiary of Mitsubishi Corp (8058). Operates domestic convenience stores (LAWSON, NATURAL LAWSON and LAWSON 100 HQ), Seijo-Ishii, entertainment-related, finance-related, and overseas (China and Thailand) businesses.

・For 1Q (Mar-May) results of FY2023/2 announced on 11/7, gross operating revenue increased by 40.5% to 237.756 billion yen compared to the same period the previous year, and operating income increased by 25.1% to 13.279 billion yen. Domestic convenience store operations, which account for about 70% of gross operating revenues, saw a 58.4% increase in gross operating revenues due to successful store remodeling and frozen food enhancements. Segment income grew 23.2% YoY.

・For its full year plan, gross operating revenue is expected to increase by 46.6% to 1.024 trillion yen compared to the previous year, operating income to increase by 12.5% to 53.0 billion yen, and annual dividend to remain unchanged at 150 yen. In the convenience store sector where 7-Eleven is strong, company appears to be facing similar challenges as FamilyMart, which ITOCHU (8001) has taken full ownership of. The EV (enterprise value)÷adjusted EBITDA multiple, known as the “simplified acquisition multiple”, is undervalued at approximately 2.6 times. Parent-child listings are also attracting attention.

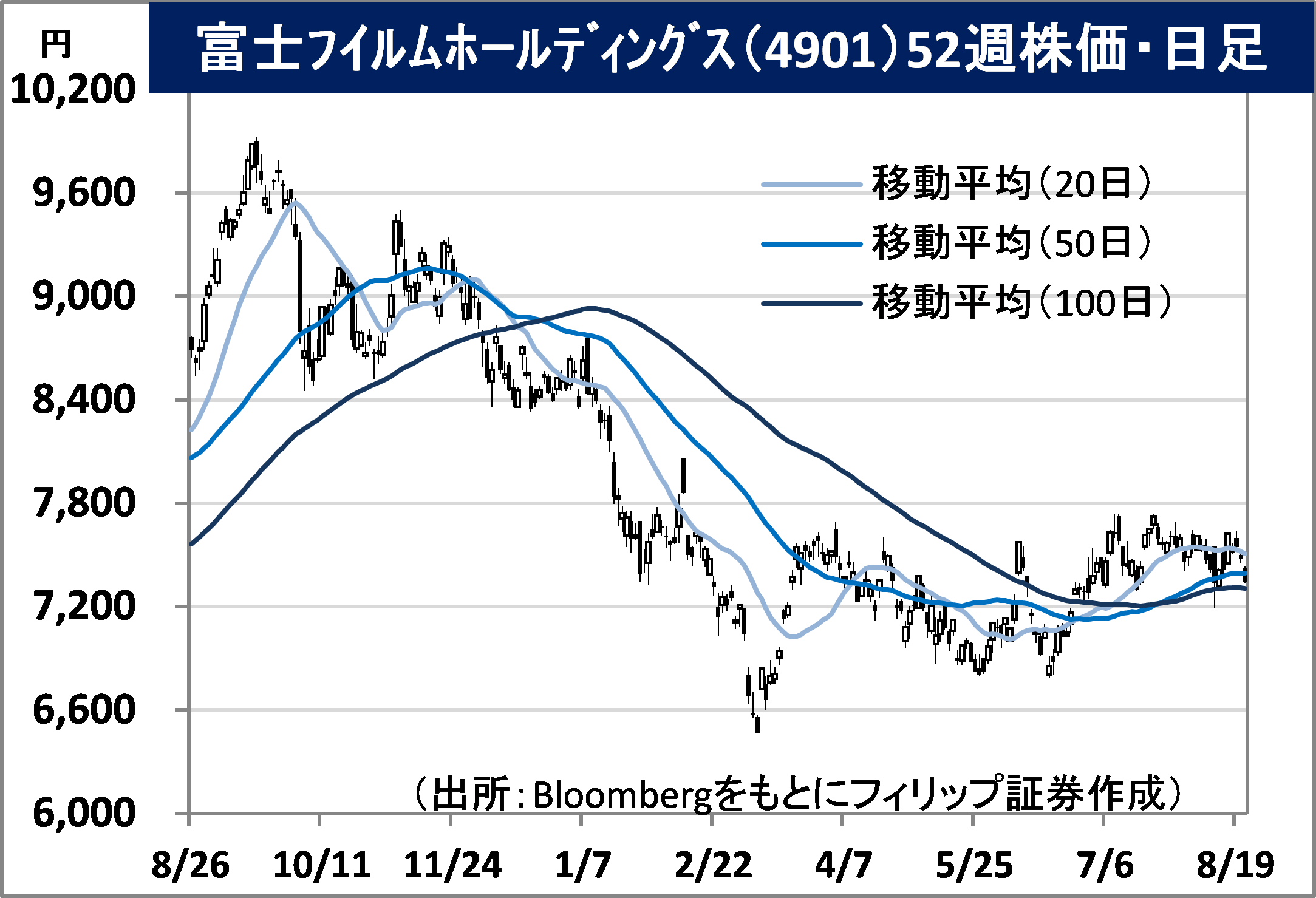

・Established in 1934. Operates four divisions, namely Imaging (images, etc), Healthcare (medical systems, bio-CDMO (contract development and manufacturing)), Materials (electronic materials, etc), and Business Innovation (digital MFPs, etc).

・For 1Q (Apr-Jun) results of FY2023/3 announced on 10/8, net sales increased by 7.4% to 625.86 billion yen compared to the same period the previous year, and operating income decreased by 12.0% to 49.55 billion yen. While all four divisions, especially Materials and Business Innovation, posted solid sales growth, operating income in the Healthcare division declined 47.7% YoY due to a shortage of semiconductors and other components in the medical systems business.

・Company has revised its full year plan upwards, taking into account the current exchange rate trend and other factors. Net sales is expected to increase by 6.9% to 2.7 trillion yen (original plan 2.65 trillion yen) compared to the previous period, and operating income to increase by 8.8% to 250.0 billion yen (original plan 245.0 billion yen). The May-July earnings announcement on 17/8 by Cisco Systems, the world’s largest US network equipment manufacturer, also showed an easing of the semiconductor supply shortage. The medical systems business, which had been a drag on earnings, is likely to recover.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: