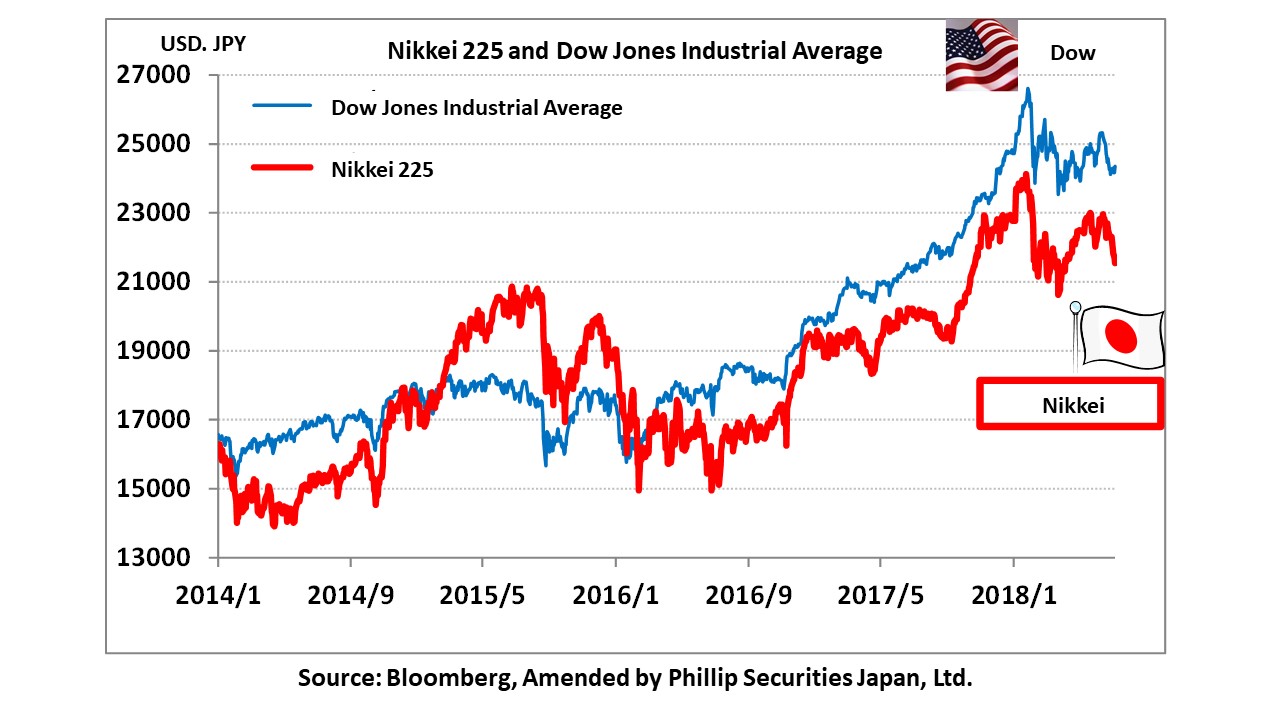

On 7/6, trade war started when both the US and China invoked sanction duties. However, Japanese and Chinese stock prices reversed their declines and trended upwards instead. Since its recent peak of 23,011.57 points on 6/12, the Nikkei average had been falling, and dropped temporarily to 21,462.95 points on 7/5, representing a decline of 1,548.62 points (6.7%) during this period. However, it reversed upwards since 7/6, and temporarily peaked at 22,692.86 points on 7/13. In the process, it regained about 80% of the decline for that period. The following are possible reasons for this: 1. Chinese stocks which are increasingly linked to Japanese stocks had hit bottom and are showing solid growth again, 2. sudden depreciation of the yen against the dollar, 3. a sense of cheaper pricing with the Nikkei average at about 13 times expected PER.

The Shanghai Composite Index fell 437.29 points (14.0%) from its recent peak of 3,128.44 points on 6/7 to 2,691.15 points on 7/6. However, it bottomed out and hit 2,843.93 points on 7/12. This is a rise of 152.78 points (5.7%) from its most recent low value. Hedge funds in Singapore are reporting the possibility of Chinese stocks rising by up to maximum 50% within the next three years as a result of easing of tensions between the US and China.

However, on 7/10, the Trump administration announced the policy to newly apply 10% tariff to Chinese products equivalent to 200 billion dollars (about 22.6 trillion yen), and publicized the target list. Meanwhile, on 7/11, the Commerce Department of China warned that such actions would hurt the WTO framework and adversely affect its globalization, and expressed that they would be forced to adopt countermeasures. It also pointed out that these US actions would hurt both China and the world, while also impairing US interests at the same time. Currently, trade talks between the US and China are stalled, but both parties are showing positive signs of resuming talks. On 7/12, US Treasury Secretary Mnuchin said that both he and the Trump administration officials “can respond” to negotiations, and that they “are advocating fair trade rather than tariffs”. We need to continue to pay attention to both the status of the US-China negotiations and the trend of Chinese stocks.

There is concern about the impact on the world economy through this trade friction, but at present, we can ascertain positive economic indicators in both Japan and the US. The US is entering performance results season for 2Q (Apr-June) of FY2018/12, while in Japan, Yaskawa Electric (6506) and Fast Retailing (9983) are expected to announce results. Indeed, investors are beginning to shift their focus onto performance trends. Investors are shifting from their cautious attitude and beginning to concentrate funds on specific stocks. As a result, big gaps in stock price performance are appearing. We should examine corporate performance and proceed with selection of stocks based on PER levels and stock prices.

In the 7/17 issue, we will be covering Jason (3080), Treasure Factory (3093), Bellsystem24 HD (6183), Yaskawa Electric (6506), Star Micronics (7718) and Fast Retailing (9983).

Selected Stocks

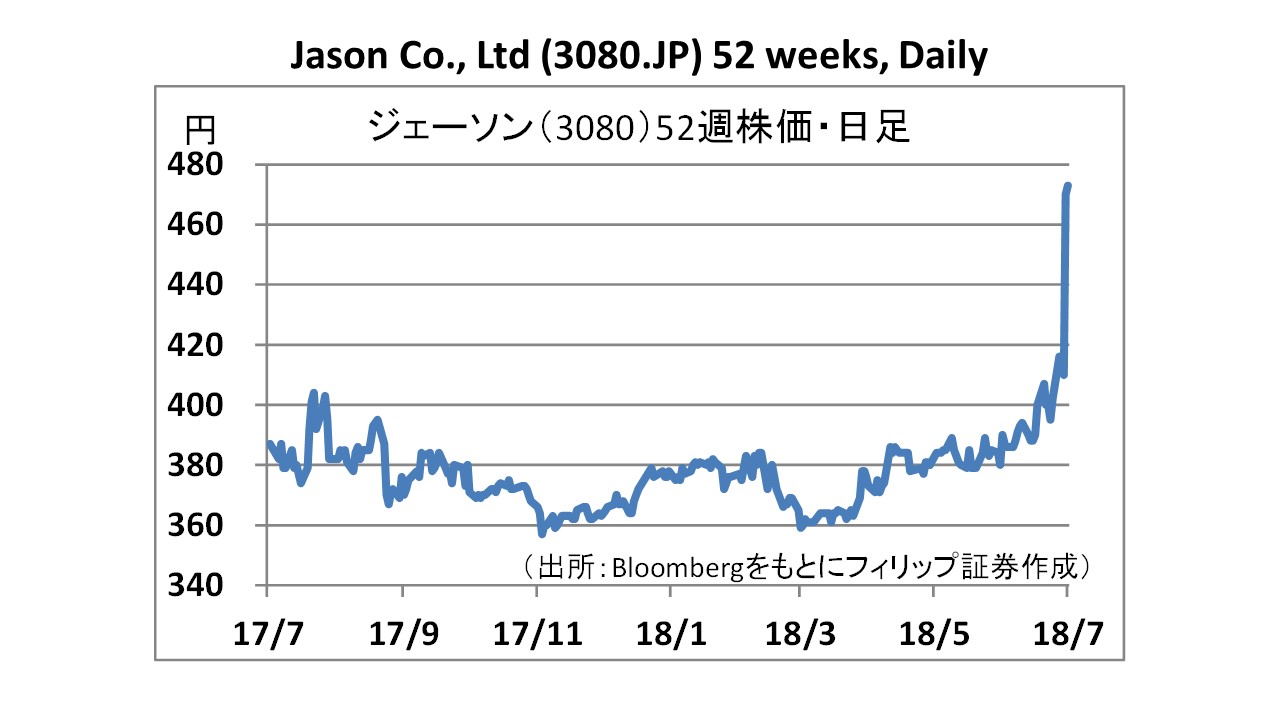

Jason Co., Ltd (3080)

・Established in 1983. Comprehensive retailer of household necessities with high consumption frequency. Also expanding partially through franchising. Implementing the “Jason” brand at variety stores and discount store chains. Has opened 101 stores in the Kanto area (as of 2018/3). From 1998/4 onwards, had focused on opening stores based only on the variety store concept.

・For 1Q (Mar-May) of FY2019/2, net sales increased by 1.5% to 6.022 billion yen compared to the same period the previous year, operating income increased by 27.0% to 253 million yen, and net income increased by 26.6% to 161 million yen. Company continued to strengthen product lineup of low-priced daily necessities and pursue low-cost store management. Reduction of logistics costs through implementation of in-house logistics has also contributed to increase in profits.

・For FY2019/2 plan, net sales is expected to increase by 3.4% to 24 billion yen compared to the previous year, operating income to increase by 21.0% to 680 million yen, and net income to increase by 11.1% to 410 million yen. Monthly sales in June maintained a strong 4.1% increase year on year. Sales of directly-managed stores in operation for more than 13 months since inception were also up 2.1% from the previous period, which is an improvement from the previous month’s 1.2% decrease over the previous period.

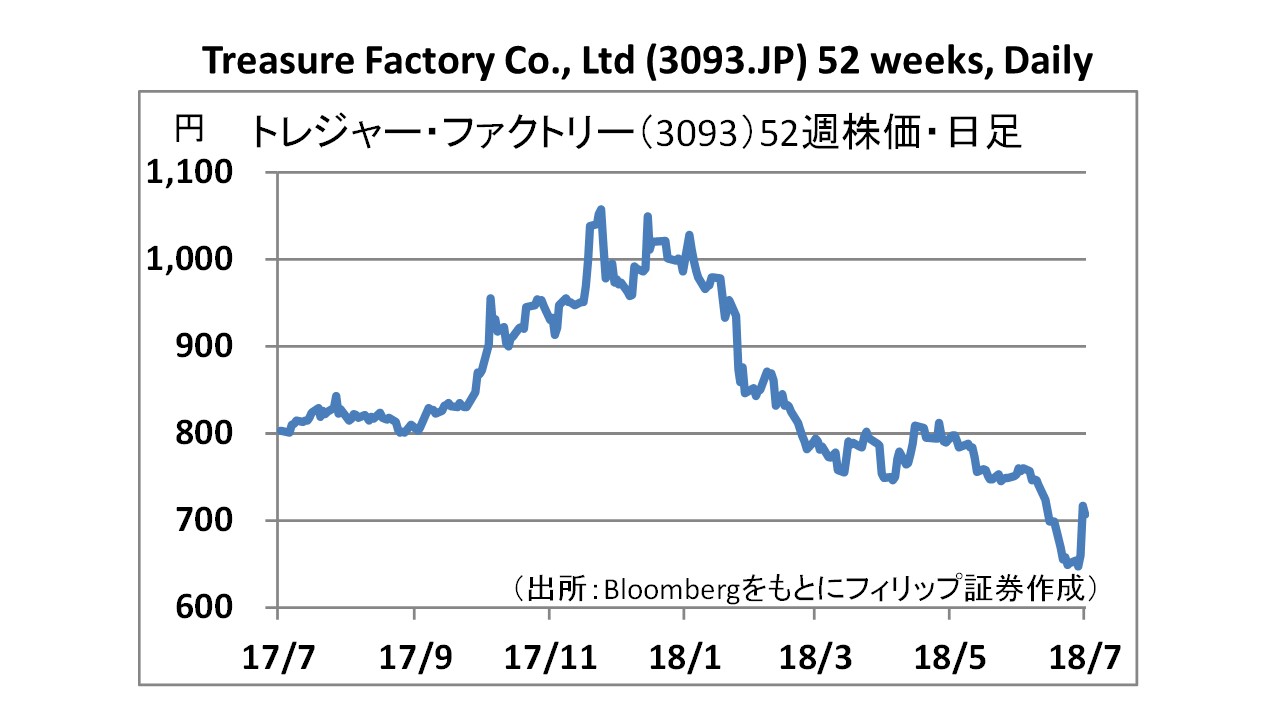

Treasure Factory Co., Ltd (3093)

・Established in 1995. Operates re-use shops selling clothing, home appliances, furniture, household goods, branded goods, sports/outdoor goods, musical instruments and hobby supplies, etc. Also conducts fashion rental business and the Treasure Factory moving service providing one-stop moving and purchasing services. Has a total of 116 stores including 112 directly-managed stores and 4 FC stores (as of 2018/5).

・For 1Q (Mar-May) of FY2019/2, net sales increased by 8.6% to 4.354 billion yen compared to the same period the previous year, operating income increased by 28.4% to 306 million yen, and net income increased by 12.5% to 195 million yen. In addition to strengthening business trips purchases and online purchases / sales, also promoting campaigns utilizing own apps and pushing alliances with other companies. Increased efficiency in personnel allocation also contributed to increase in profits.

・For FY2019/2 plan, net sales is expected to increase by 8.3% to 17.799 billion yen compared to the previous year, operating income to increase by 31.6% to 818 million yen, and net income to increase by 60.2% to 554 million yen. Company intends to utilize the appraisal know-how and appraisal information pertaining to Golf Kids, which became a subsidiary in 2018/3, as a whole for the entire group, and to the expansion of the golf equipment sector.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: