Possibility of an “Abe-Trump Show” in the political arena?

As stated in the 8/4 Weekly Report, we believe that, in the new financial year, there will be movements in the Japanese stock market in response to the House of Councilors election in July. At this juncture, the postponement of the consumption tax hike has emerged as a major issue.

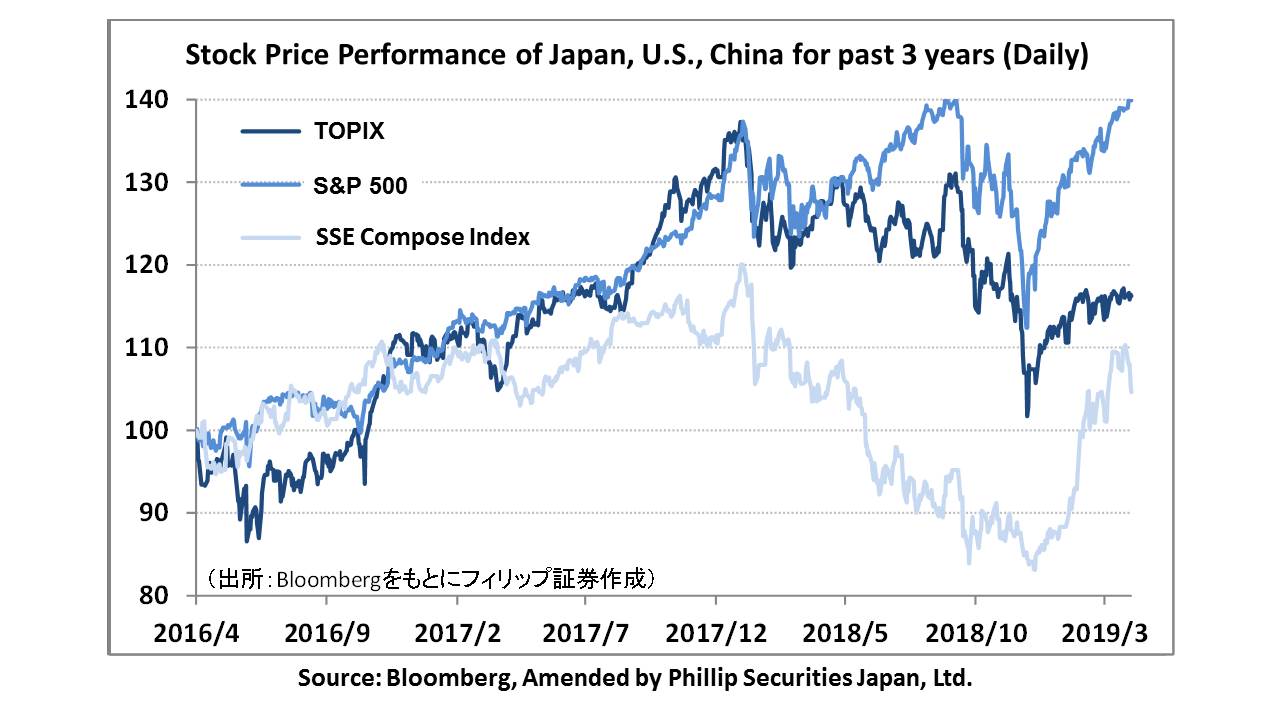

Both the NASDAQ and S&P500 closing prices have hit record highs with increasing expectations that corporate earnings announcements for the Jan-Mar period for US stocks will be better than market forecasts. The Japanese stock market has been quiet especially on 22-23/4 before the 10-day holidays. With the delivery date for 24/4 contracts being only after the end of the long holidays, concerns about realizations and stop-loss selling have taken a backseat for the time being. Expectations for the BOJ’s Monetary Policy Meeting on 25/4 and the Japanese yen’s depreciation have pushed the Nikkei average to the 22,300 points level.

On the other hand, regarding the issue of raising the consumption tax to 10% in October, on 18/4, Mr. Hagiuda, Executive Acting Secretary-General of the LDP, said that “there could be different developments depending on the figures of the June BOJ Tankan Survey”, thereby pointing out the possibility of postponement of the tax increase. Meanwhile, Chief Cabinet Secretary Suga had stated the traditional view that “the consumption tax will be raised to 10% in October unless there is an event arising equivalent to that of a Lehman-shock”. It therefore seems that the issue of the postponement of the consumption tax hike has suddenly broken out.

However, in the “March Economy Watchers Survey” issued by the Cabinet Office on 8/4, the DI for current conditions for all items had fallen below the standard value of 50.0, and that for future conditions for all items except “Services” had also fallen below 50.0, showing a worsening of results. There is strong concern that a recession might arise due to the consumption tax hike. In addition, since last year, the Trump administration has intensified its criticism that the export drawback on consumption tax has amounted to an “export subsidy” for auto motives. Therefore, it is easy to imagine that the consumption tax hike will be singled out during the Japan-Trade Agreement on Goods (TAG) negotiations on 15-16/4. For President Trump, who is aiming for re-election in 2020, he cannot afford to lose the casting votes held by the “Rust Belt” (rusted industrial area) states of Ohio and Pennsylvania. Protection of the US automobile industry, which is at the center of this belt, is a high policy priority.

Consumption tax increase is the premise for confidence in Japanese government bonds, and we should not look lightly upon fiscal reformation. By asking the people to have faith in the dissolution of the House of Representatives and the simultaneous elections for both the House of Councilors and the House of Representatives, it is perhaps a politician’s instinct and ambition to secure a large stable majority in both Houses and then go on to fight for constitutional revisions that no one had been able to do before. We therefore cannot ignore the possibility of an “Abe-Trump Show” in which, with the strong support of President Trump, PM Abe throws in everything he has in order to secure a major win.

In the 7/5 issue, we will be covering M3 (2413), Tear (2485), Sumitomo Dainippon Pharma (4506), Kyocera (6971), Net One Systems (7518) and Heiwa Real Estate (8803).

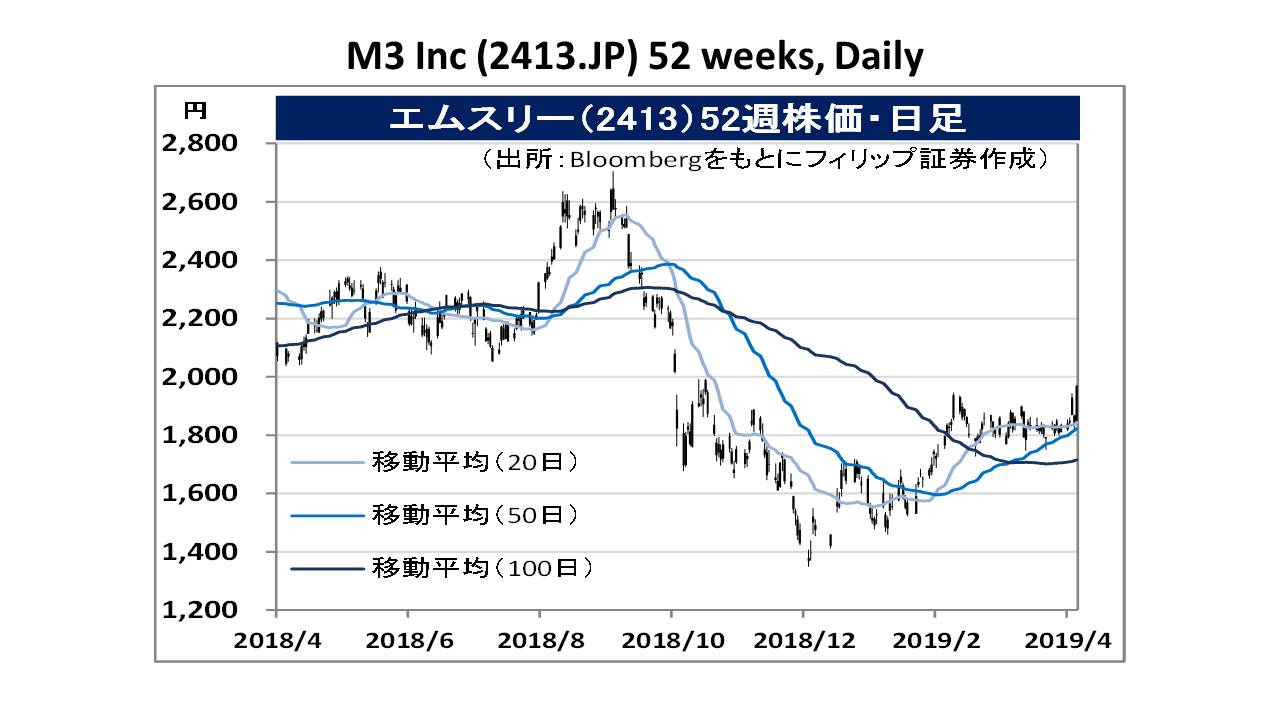

・Established in 2000. Providing a variety of services centering on platforms for healthcare professionals such as “m3.com”, used by more than 250,000 doctors as members in Japan, “MDLinx” in the US, and “Doctors.net.uk” in the UK. Also provides outplacement support specific to the medical industry. Developing business in more than 10 countries worldwide.

・For FY2019/3 results announced on 24/4, sales revenue increased by 19.7% to 113.059 billion yen compared to the same period the previous year, operating income increased by 12.1% to 30.8 billion yen, and current income increased by 9.4% to 21.414 billion yen. Career Solutions had increased owing to strong steady inflow of doctors and pharmacists. Temporary profits from reorganization of group companies have also contributed to increase in profits.

・For FY2020/3 plan, sales revenue is expected to increase by 15.0% to130.0 billion yen compared to the previous year, operating income to increase by 13.6% to 32.0 billion yen, and current income to increase by 12.4% to 22.0 billion yen. The electronic medical record business, which will be the engine of growth for the future, will accelerate its input after changing its product name to “M3 Digital” last November. Inputs have increased by 2.5 times compared to the previous year.

・Established in 1997. Conducts funeral business centering on funeral services including funeral consultation and a membership “Tear Club”. Also has a franchise business franchising the “Tear Funeral Hall” management to companies in other business sectors.

・For 1Q (Oct-Dec) results of FY2019/9 announced on 7/2, net sales increased by 8.2% to 3.266 billion yen compared to the same period the previous year, operating income increased by 17.6% to 461 million yen, and net income increased by 16.3% to 308 million yen, showing increase in both income and profits. Absorbed increase in SG&A expenses by increasing directly-managed stores, and decreasing sales-cost ratio by reviewing product content and having in-house production of funeral incidental services.

・For FY2019/9 plan, net sales is expected to increase by 4.7% to 12.885 billion yen compared to the previous year, operating income to decrease by 16.9% to 1.1 billion yen, and net income to decrease by 21.9% to 700 million yen. Company revised its 1H (2018/10-2019) results for FY2019/9 upwards on 24/4. 1H operating income and net income will reach 89% and 75% respectively of full-year results. Even with expected increase in SG&A expenses due to opening of new concept stores in the Kanto region, let’s look forward to results from the upward revision of full-year results.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: