Report type: Weekly Strategy

“On the Opposite Side of the Bad News for the Stock Market, Can SiC Drive the Market?”

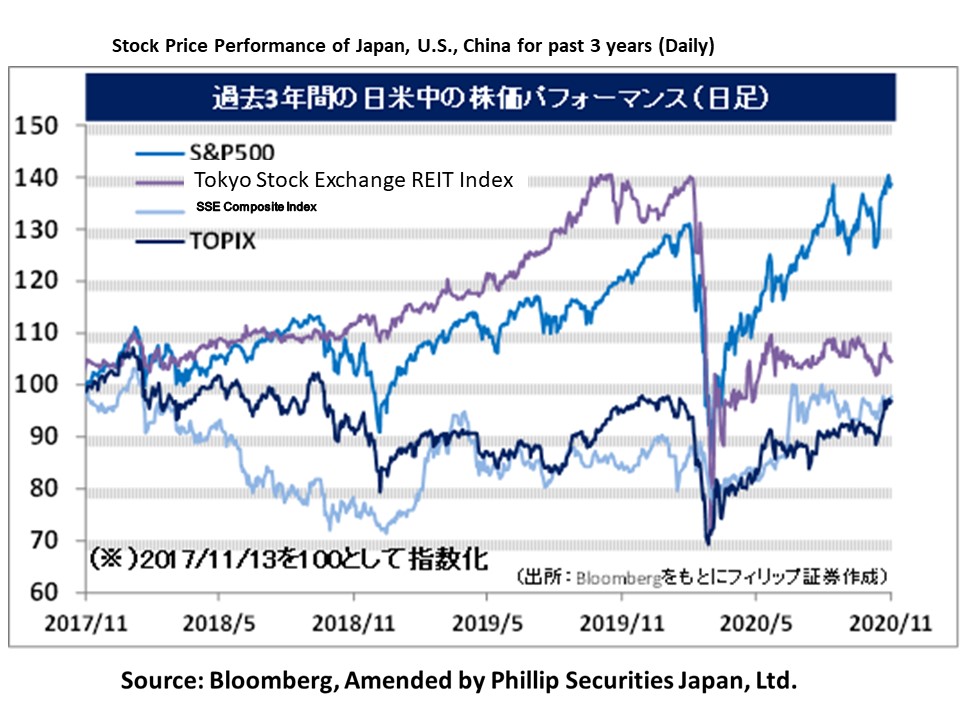

Following the joint development between the U.S. pharmaceutical corporation Pfizer (PFE) and the German BioNTech, on 16/11, U.S. biotechnology Moderna (MRNA) demonstrated high efficacy in clinical trials involving the development of a COVID-19 vaccine. Reacting favourably to this, the Nikkei average also rose to exceed 26,000 points on 17/11. However, in addition to the accelerated spread of COVID-19 in Europe, the U.S. as well as Japan, on the other hand, there has been added bad news for the stock market which did not surface up to now, and the Nikkei average turned towards a decline from 18/11 onwards to fall under 25,500 points on 20/11.

We can consider the following 3 points to be the main bad news for the stock market. ① Concerns of China’s financial crisis following the Chinese semiconductor giant, Tsinghua Unigroup, which is a subsidiary of Tsinghua University, the alma mater of President Xi Jinping, defaulting on a private placement bond, ② Softbank Group (9984)’s CEO Son expressing at the online summit hosted by the NY Times held from 17-18/11 on the possibility of a worst case scenario “of a level of the bankruptcy of the Lehman Brothers” occurring within the next 2-3 months, and that selling recent assets and raising the cash ratio was to prepare for the worst case scenario, and ③ the candidate Biden being elected in the U.S. presidential election and the Trump camp not showing signs of relent in their resistance to the bitter end in allegations on the election being rigged. Since it is believed that neither of these can be taken lightly, the reason for the market decline in the past few days was likely not only due to profit-taking from the sudden rise in the market. Perhaps a situation of a decline will be expected from 24/11 onwards which tests whether the Nikkei average will fall under around 24,500 points, which was a blank price range formed from the price jump from the closing price on 6/11 to the opening price on 9/11.

As a policy considered by the government and the ruling party towards achieving the government’s aim in having zero practical emission amount of greenhouse gases by 2050, it was said that they would introduce a tax incentive for investments (green investments) in production facilities of products related to the reduction of greenhouse gases. In green investments, in addition to wind power generation and the next-gen type of lithium-ion batteries, it includes power semiconductors which lead to electricity savings by controlling voltage. With the expectation of there being an importance in the role played by power semiconductors in self-driving cars, which are comprised of a multitude of different electronic systems, in terms of quality and as an element of it, the “silicon carbide (SiC)” wafer is regarded as leading. However, since there is an oligopoly in the SiC wafer market at the moment with a focus on the U.S. components manufacturer, Cree (CREE), there remains the issue of its stable procurement for semiconductor device manufacturers.

Also, since materials from fibres using SiC are light, have high strength and superior heat resistance, as a next-gen material, it is expected to contribute to the reduction of greenhouse gas emissions by enhacing fuel consumption performance with a focus in the aviation industry. It is likely that attention will be on the movements of corporations possessing its manufacturing technology.

In the 24/11 issue, we will be covering Showa Denko (4004), Ube Industries (4208), Godo Steel (5410), and ROHM (6963).

・Started from a merger between Nihon Electrical Industries and Showa Fertilisers in 1939. Manages petrochemistry, chemicals, electronics, inorganic, aluminium and other businesses. Hitachi Chemical became their subsidiary in April 2020. Holds the top spot in Japan for electric furnace graphite electrodes.

・For 9M (Jan-Sep) results of FY2020/12 announced on 5/11, net sales decreased by 8.6% to 635.977 billion yen compared to the same period the previous year and operating income fell into the red from 109.313 billion yen the same period the previous year to (15.41) billion yen. Although there was a factor of an increase in revenue from their consolidated subsidiary, Hitachi Chemical, the decline in the market condition of petrochemical products and the revenue decrease in the graphite electrodes business following a decrease in production in the steel industry, etc. have affected.

・For its full year plan, net sales is expected to increase by 5.9% to 960 billion yen compared to the previous year and operating income to fall into the red from 120.798 billion yen the previous year to (30) billion yen. While there are effects of an increase in revenue following the acquisition of Hitachi Chemical, it is predicted that expenses following it and the decrease in sales quantities of graphite electrodes, etc. will affect profits. Improvement in finances via the sale of businesses and the increase in production of silicon carbide (SiC) epitaxial wafers, which will serve as a material for power semiconductors for the purpose of voltage control, will likely contribute to an improvement in business performance from next year onwards

・Originated from coal mining in 1897 and established in 1942. Operates business segments, such as chemistry, such as nylon resin and synthetic rubber, etc., construction materials, such as cement and limestone, etc., machines, such as moulding machines, etc., and carries out the manufacture and retail of those related to them.

・For 1H (Apr-Sep) results of FY2021/3 announced on 30/10, net sales decreased by 16.4% to 280.013 billion yen compared to the same period the previous year and operating income decreased by 79.6% to 3.41 billion yen. The chemicals segment was mainly affected by the COVID-19 catastrophe, and the decrease in sales quantities of products related to automobiles, such as synthetic rubber and battery materials, as well as the drop in retail price of nylon, etc. have influenced the decrease in sales and income.

・For its full year plan, net sales is expected to decrease by 11.4% to 592 billion yen compared to the previous year and operating income to decrease by 36.8% to 21.5 billion yen. With only this company and Nippon Carbon (5302) in the world which are able to manufacture fibres of silicon carbide (SiC), which is light, have high strength and superior heat resistance and which is expected to be the ace in improving fuel consumption such as in aircrafts, etc., towards achieving the government’s target of “zero greenhouse gas emissions by 2050”, it is predicted that there will be an increase in the number of uses of the material in addition to in aircrafts, such as automobiles, etc.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: