Report type: Weekly Strategy

Nikkei Average VI at “major bottom” – beware of soaring volatility

The Nikkei Average is showing signs of a stalemate ahead of the announcement of the appointment of a new deputy governor of the BOJ, which is reported to be submitted to the Diet on 14/2. The Nikkei Stock Average Volatility Index (Nikkei VI), which reflects investor sentiment toward Japanese stocks and is also known as the Japanese version of the fear index, fell to 15.92 at the close of trading on 8/2, the lowest level since 6 July, 2021.

When it was reported in the early morning of 6/2 that the government had approached Deputy Governor Amamiya about succeeding BOJ Governor Kuroda, the market reacted with a weaker yen and a stronger dollar, a decline in long-term interest rates, and higher stock prices due to expectations and conviction that the BOJ would maintain its course of large-scale monetary easing. In response, the PMO denied the report, and PM Kishida himself stated that he would place importance on the ability to disseminate information both domestically and internationally. As a result, the name of former BOJ Deputy Governor Nakaso, a leading figure in the “global camp”, is surfacing rapidly in financial markets. If Deputy Governor Amamiya were eliminated from consideration, it is likely that the yen will appreciate against the US dollar and the Nikkei Average will fall.

Looking at overseas markets, European equities are performing well along with expectations of a recovery in the Chinese economy. The risk of recession in the European economy is receding as inflation growth is slowing as a result of easing energy shortages owing to falling natural gas prices. The UK FTSE 100 index hit record highs during trading hours for consecutive days through 9/2, and the German DAX index reached its highest level in a year on 9/2. Against this backdrop, it is worrisome that there is growing concern that Russia may launch a large-scale offensive in late February, one year after its invasion of Ukraine.

Given this outlook for domestic and overseas conditions, it is important to note that from mid- to late February the volatility of Japanese stock prices may expand from a “major bottom”. It should be noted that, against the backdrop of the declaration of a state of emergency due to the COVID-19 pandemic, the Nikkei Average had fallen from 28,600 points on 6 July, 2021 to below 27,000 points on 20 August, 2021 before reversing and rising due to rising expectations towards the “post-PM Suga” era.

Market volatility due to a BOJ governor appointment surprise will be a tailwind for banking and insurance stocks owing to the expectation of large-scale monetary easing corrections. In addition to investing in individual financial stocks for dividends, the NEXT FUNDS TOPIX Banks ETF (1615) will also be of interest. The financial sector is also likely to benefit from higher US long-term interest rates following the release of the December US jobs report, and the scope for benefits both domestically and internationally is expected to be relatively broad. In addition, regarding risks of the situation in Ukraine, focus will likely be on trading company stocks and other stocks that are likely to benefit from a sharp rise in commodity prices due to the tight supply-demand conditions for commodities such as energy, grains, and precious metals produced in Russia.

In the 13/2 issue, we will be covering Panasonic Holdings (6752), Nintendo (7974), Nippon Building Fund Management (8951), and TV Tokyo Holdings (9413).

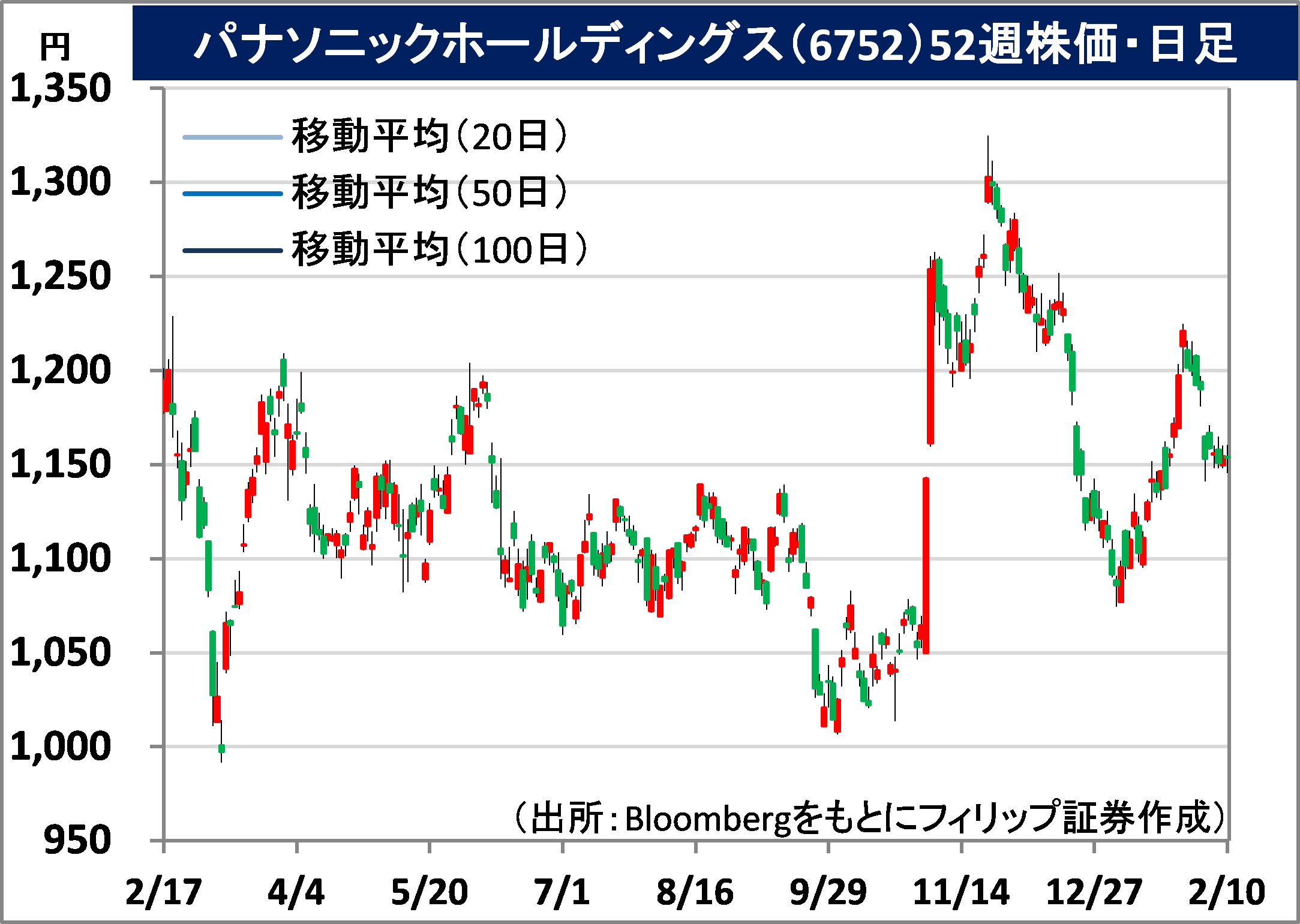

Panasonic Holdings Corp (6752) 1154 yen (10/2 closing price)

・General electronics manufacturer established in 1935. Produces, sells, and provides services for home appliances, FA equipment, information and telecommunications equipment, and housing equipment. Besides lithium-ion batteries and devices, focus is also on the expanding automotive business.

・For 9M (Apr-Dec) results of FY2023/3 announced on 2/2, net sales increased by 14.8% to 6.2245 trillion yen compared to the same period the previous year, and operating income decreased by 14.6% to 234.22 billion yen. 3Q (Oct-Dec) sales increased 14% YoY and operating income increased 16% YoY. 3Q sales by segment were up 27% YoY in Automotive business, and up 26% YoY in Energy business, which includes the automotive battery business for Tesla.

・Company has revised its full year plan downwards. Net sales is expected to remain unchanged, increasing by 11.0% to 8.2 trillion yen compared to the previous year, and operating income to decrease by 21.7% to 280.0 billion yen (original plan 320.0 billion yen) as a result of deteriorating market conditions in China (ICT etc). Tax credits under the US Inflation Control Act, which was passed in August last year and enacted from the end of December, cannot be factored into the earnings forecast because the detailed forecast for the Nevada plant for Tesla, which is currently in operation, and the new plant in Kansas, which is scheduled to start operations in fiscal 2024, has not been announced.

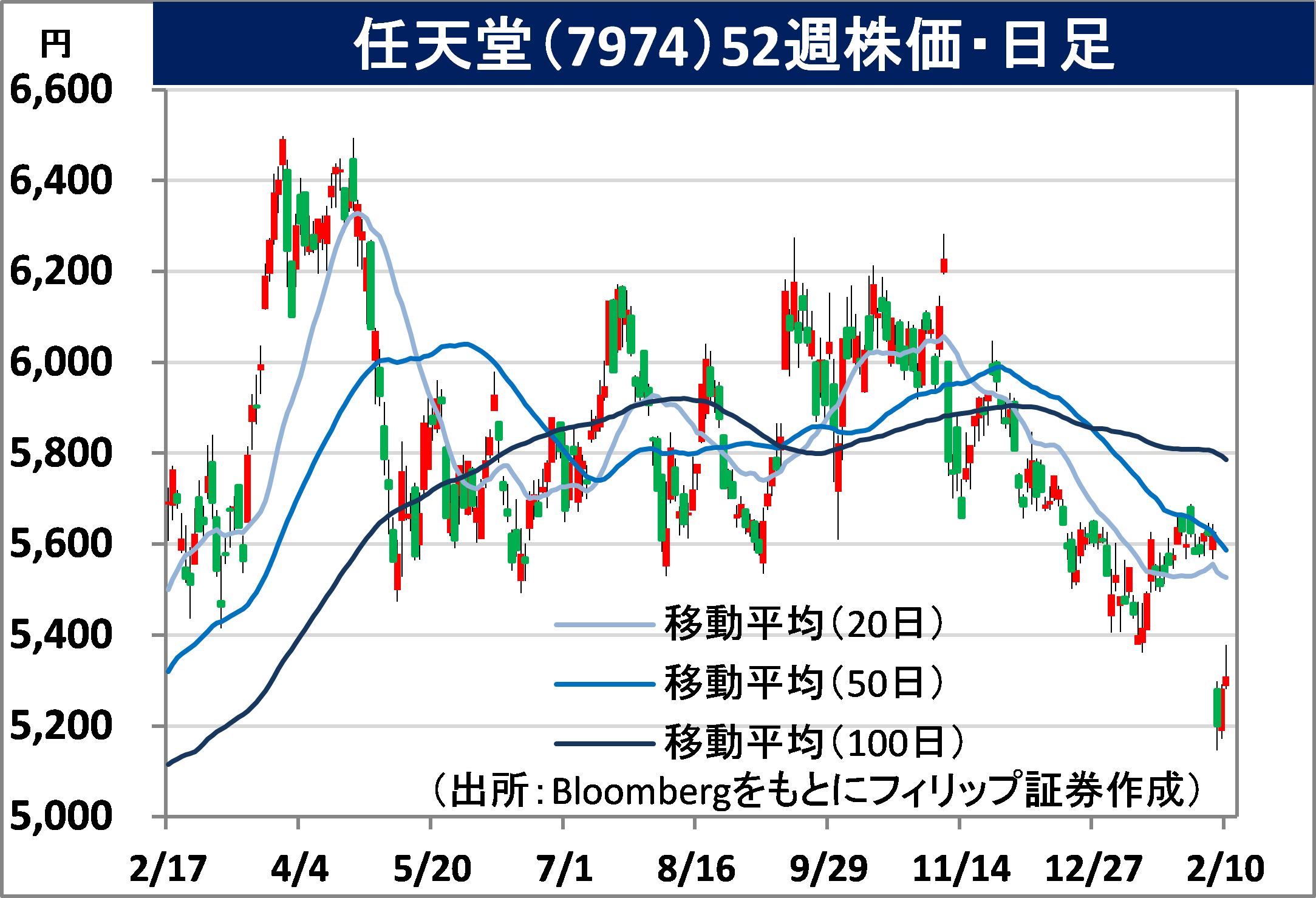

Nintendo Co., Ltd (7974) 5307 yen (10/2 closing price)

・Founded in 1889 as a manufacturer of “Hanafuta” (Japanese playing cards). Started manufacturing and selling “Karuta” (Japanese traditional playing cards) and western playing cards in 1947. Principal product is a “game console” using a computer. Has a 32% stake in The Pokemon Company, an equity-method affiliate.

・For 9M (Apr-Dec) results of FY2023/3 announced on 7/2, net sales decreased by 1.9% to 1.2951 trillion yen compared to the same period the previous year, and operating income decreased by 13.1% to 410.5 billion yen. In 3Q (Oct-Dec), when year-end sales is concentrated, sales declined 8.3% YoY and operating income fell 24.7% YoY. “Switch” hardware consoles reached a cumulative total of 125.55 million units sold, with sales volumes slowing.

・Company has revised its full year plan downwards. Net sales is expected to decrease by 5.6% to 1.6 trillion yen (original plan 1.65 trillion yen) compared to the previous year, and operating income to decrease by 19.0% to 480.0 billion yen (original plan 500.0 billion yen). Annual dividend to reduce by 44 yen to 159 yen. An increase in software unit sales is expected even with the decline in hardware console sales volume. “Super Nintendo World” will open at Universal Studios Hollywood on 17/2 while “The Super Mario Bros. Movie” will open worldwide in April. New frontiers are being explored.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: