Report type: Weekly Strategy

Nikkei Average Accelerates Above 21,000 Points

The Japanese stock market remained strong even after the Nikkei Average exceeded 22,000 points on 1/6, rising to a high of 22,907 points on 4/6. It rose from a low of 16,358 points on 19/3, exceeded 20,000 points initially on 30/4, and exceeded 21,000 points after another 15 business days on 26/5. Thereafter, the market accelerated above 21,000 points to reach 22,000 points four business days later on 1/6.

The Nikkei Average of 21,000 points is positioned as an important milestone in market pricing in the medium term. It reached a high of 20,952 points in June, 2015 before meeting resistance at 20,946 points in August of the same year. In 2018, in the middle of the down market from late January to March, it dropped to 20,950 points on 14/2 and then rose to 22,502 points on 27/2. Again, during the down market from early October to late December of that year, it fell to 20,971 points on 26/10 before rebounding to 22,698 points on 3/12. In that sense, the 21,000 points level is looked upon as an important market level that separates bullish and bearish market conditions. If an important price level often corresponds to the center or average level of the market range, and if the negative limit of the bear market is the low level of 19/3 (21,000 points minus 4,642 points), then the positive limit of the bull market may be seen as the level with a similar positive price range above 21,000 points.

In addition, the movement from a low of 19,239 points on 8/9 of 2017 to a high of 23,382 points on 9/11 of that year can serve as a reference for the Nikkei Average level of 23,000 points. After hitting a high of over 23,000 points on 9/11, it was pushed down by strong selling, resulting finally in a low of 22,522 points that day. Partly due to wild market fluctuations that day, even though it reached the 23,000 points level several times during the period from May to September of 2018, it would always be prevented from rising further due to market selloffs. In that sense, the Nikkei Average of 23,000 points can be viewed as a price range where upside tends to meet resistance. However, on the other hand, if it manages to break out of that price range, it may be possible that the surge will accelerate. It is therefore important to note that the major SQ date (the final settlement date for futures/options trading once every three months), which is set for 12/6, is likely to become such a turning point.

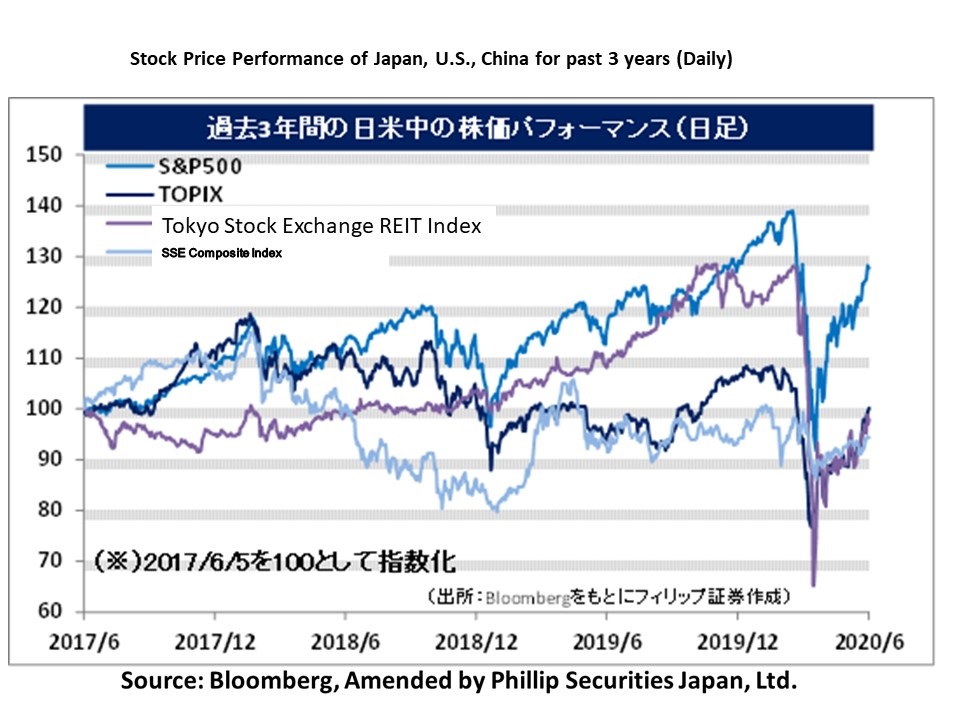

In the current financial markets, US long-term interest rates have risen due to expectations for resumption of economic activity in major countries and improvement in economic indicators, and financing via yen carry trade, which sells yen and raises US dollars, is beginning to revive. In addition, the Fed’s monetary easing measures have led to a shift in global investment funds from the US dollar to the Euro, currencies of resource-rich countries and currencies of emerging economies. In particular, the expansion of the ECB’s measures to purchase emergency bonds as a countermeasure against Covid-19 may accelerate risk. The US employment statistics announced on 5/6 will be important in terms of forecasting the continuation of risks.

In the 8/6 issue, we will be covering UACJ (5741), Mitsubishi Heavy Industries (7011), Japan Airlines (9201), and NTT (9432).

・Formed in 2013 with the merger of operations of Furukawa-Sky and Sumitomo Light Metal Industries. Furukawa Electric (5801) is the largest shareholder with a 24.9% stake. Has the highest rolled aluminum production capacity in Japan, and third in the world after Alcoa and Novelis in the US.

・For FY2020/3 results announced on 19/5, net sales decreased by 7.0% to 615.15 billion yen compared to the previous year, operating income decreased by 31.9% to 10.126 billion yen, and current income increased by 82.6% to 2.038 billion yen. Sales declined due to a decline in aluminum ingot prices, while operating income declined due to a deterioration in inventory valuation, but current income increased due to the recording of deferred tax assets.

・Company plan for FY2021/3 has not been decided because the impact of the spread of Covid-19 cannot be reasonably determined at this time. Announced that it is in the process of implementing structural reforms based on the medium-term management plan for FY2018 to FY2020, and will be integrating the three coil center subsidiaries on 1/10. With increasing global interest in reviewing easily recycled aluminum cans owing to movements away from plastic usage, we can expect market reviews of the stock’s low PBR.

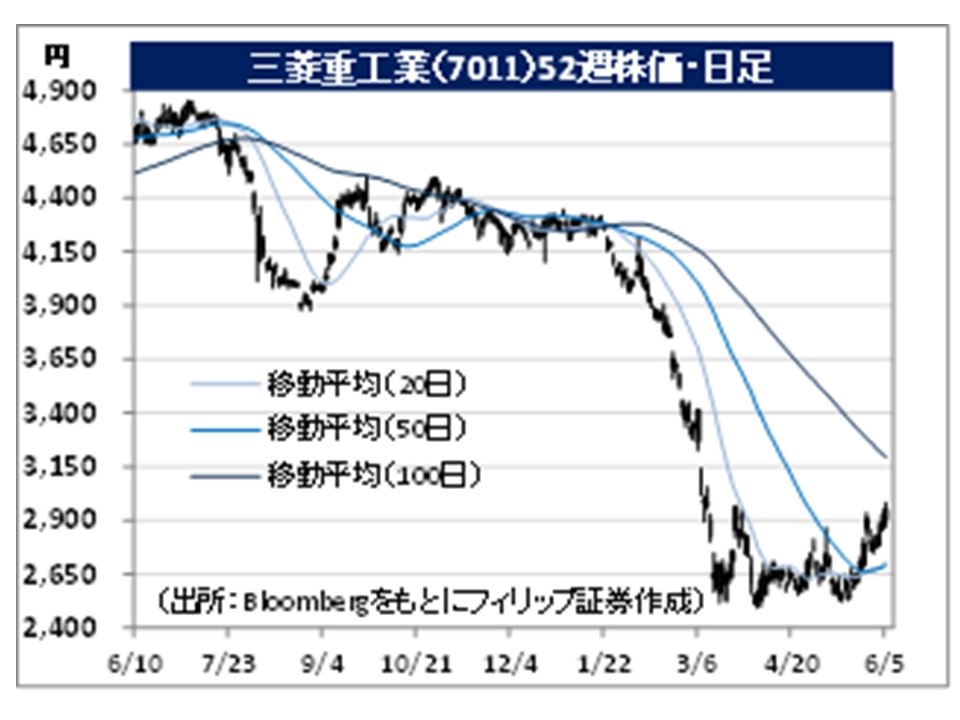

・Founded in 1884 by Yataro Iwasaki with the opening of Nagasaki Shipyard. The three main business segments are “Power Systems” including power generation systems, “Industry & Infrastructure” including ships, and “Aircraft, Defense & Space” including aircrafts.

・For FY2020/3 results announced on 11/5, revenue decreased by 0.9% to 4.0413 trillion yen compared to the previous year, and income from business activities turned from a profit of 200.57 billion yen in the previous year to a loss of 29.538 billion yen. Orders received increased 8.2% year-on-year to 4.1686 trillion yen, but profits were impacted by the recording of the impairment loss of SpaceJet-related assets handled by subsidiary Mitsubishi Aircraft.

・For FY2021/3 plan, net sales is expected to decrease by 6.0% to 3.8 trillion yen compared to the previous year, and income from business activities to recover to zero from a loss of 29.538 billion yen the previous year. Amid adverse headwinds such as the impact of Covid-19 and the additional cost of the SpaceJet business of 260 billion yen, company is aiming to capture huge demands through lower costs via the development of the next generation domestic rocket “H3”. We can look forward to company to play a leading role in the “Space Industry Vision 2030” national policy

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: