|

Report type: Weekly Strategy |

Mega Platform Providers and the Resolution of Parent-Subsidiary Listing

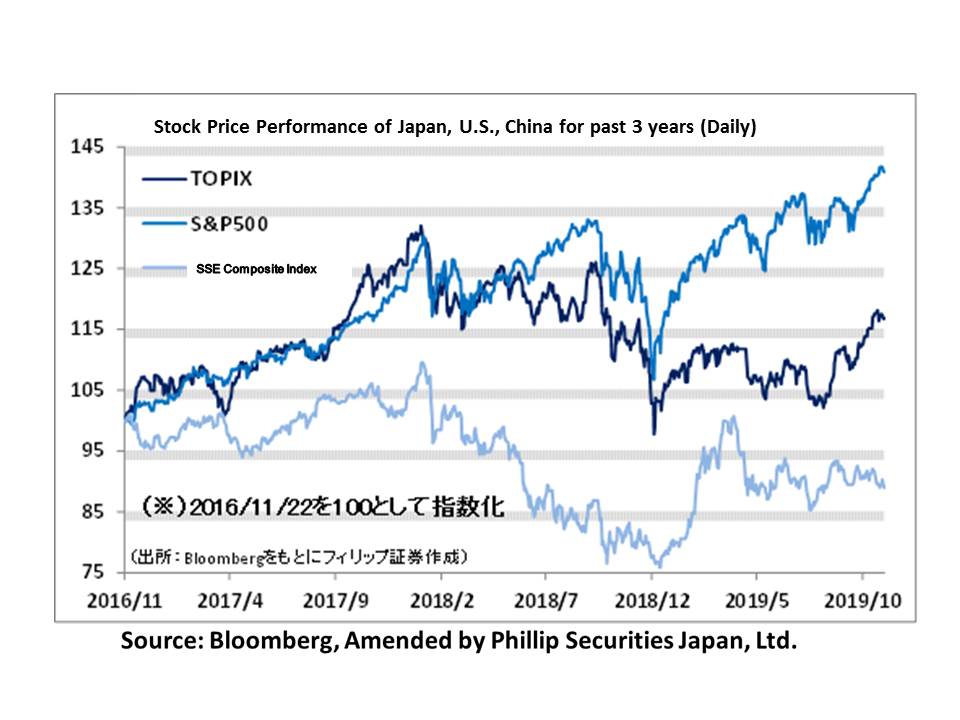

In the Japanese stock market in the week of 18/11, net buying by foreign investors continued for the 7th consecutive week up to 15/11, in addition to the extended positive influence from the supply and demand aspect, such as continued spot buybacks following the relief of positions from the amount of “unsettled selling balance of arbitrage” exceeding the “unsettled buying balance of arbitrage” on 15/11, which caused the Nikkei average to rise until 23,420 points at the start of the week on 18/11. However, the “Hong Kong Human Rights and Democracy Act” was passed unanimously at the US Senate, which saw predictions of a backlash from China regarding the interference into internal affairs that led to concerns of an agreement being reached in the trade negotiations. This caused the Nikkei average to plummet to 22,726 points on 21/11. After which, due to reasons such as China’s Vice Premier Liu He’s positive statement regarding the US-China agreement, the Nikkei average rose to the 23,200 point level on 22/11.

In the week of 18/11, there were 2 major movements which indicated future trends for Japanese stocks. Firstly, on 18/11, the conclusion of a basic agreement on a business merger between Yahoo’s parent company, ZHDS (4689), and LINE (3938) was announced. Yahoo is the nation’s largest portal site, while LINE holds an immense volume of shares in Japan as a communication app. Furthermore, there are also expectations of a merger between fierce rivals in cashless payment, PayPay and LINE Pay. Although there are remaining problems involving competition law, if the merger is finalised, it would likely pose a significant influence on the management strategies of Rakuten (4755), an e-commerce platform provider competitor, and Mercari (4385), a cashless payment competitor. Especially since LINE has strong brand presence in Thailand and Taiwan, they would be competing against Alipay and WeChat Pay, and we can also expect a possibility of them becoming a mega platform provider in Asia.

The next important movement involves the listed subsidiary, Mitsubishi Tanabe Pharma (4508) of parent company Mitsubishi Chemical Holdings (4188), becoming a wholly-owned subsidiary. In terms of corporate governance and from the parent company’s point of view, the resolution of parent-subsidiary listing is considered desirable from the perspective of enhancing ROE by incorporating minority interest as well as the selection and focusing of businesses. The market capitalisation of Mitsubishi Chemical Holdings is lower than the total market capitalisation of their 2 listed subsidiaries, which has seen the phenomenon of a parent-subsidiary reversal. Also, in terms of handling environmental issues, the chemical business tends to view plastic products, etc. in an unfavourable light, and growth prospects are slim. We may see an increase in movements in the future where parent companies who handle businesses with poor growth prospects, deciding to fully own their subsidiaries in order to tap into growth of the businesses carried out by their subsidiaries.

In the 25/11 issue, we will be covering Capital Asset Planning (3965), Terumo (4543), KYORIN Holdings (4569), Nihon Unisys (8056), Nippon Sharyo (7102) and PARCO (8251).

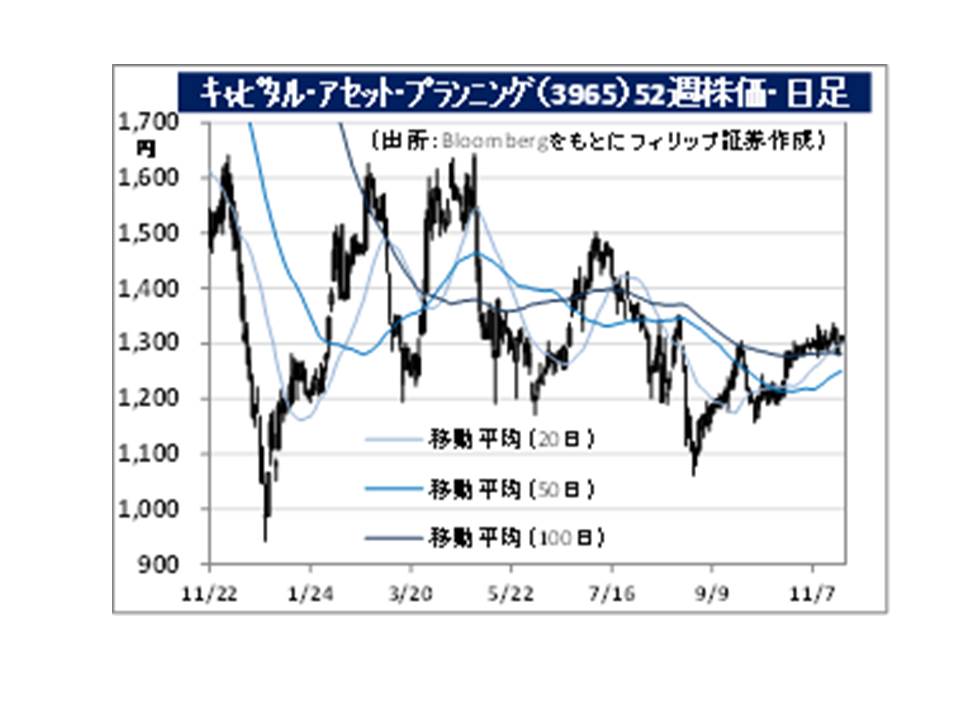

・Established in 1990. Provides optimized work process systems in the financial retail business for financial institutions, etc. Their main services involve the retail flow and business management for life insurance companies as well as asset advice functions for the wealthy.

・For FY2019/9 results announced on 8/11, net sales was 7.29 billion yen (company plan: 7.2 billion yen) and operating income was 625 million yen (company plan: 590 million yen) (Comparison with the same period the previous year was not included as the company prepared their consolidated financial statements from FY2019/9.). Development and retail of integrated asset formation advice systems for non-financial institutions in addition to systems for life insurance have performed strongly.

・For its FY2020/9 plan, net sales is expected to increase by 12.5% to 8.2 billion yen compared to the previous year and operating income to increase by 13.6% to 710 million yen. Company is currently focusing their efforts on SaaS-based continuous billing businesses involving life plan app integrated platforms. Profit margin is expected to increase if it popularises in local financial institutions, securities companies and accounting firm networks, etc. There is also a forecasted increase projects being entrusted for life insurance. Attention will likely be on them as a prospective fintech stock.

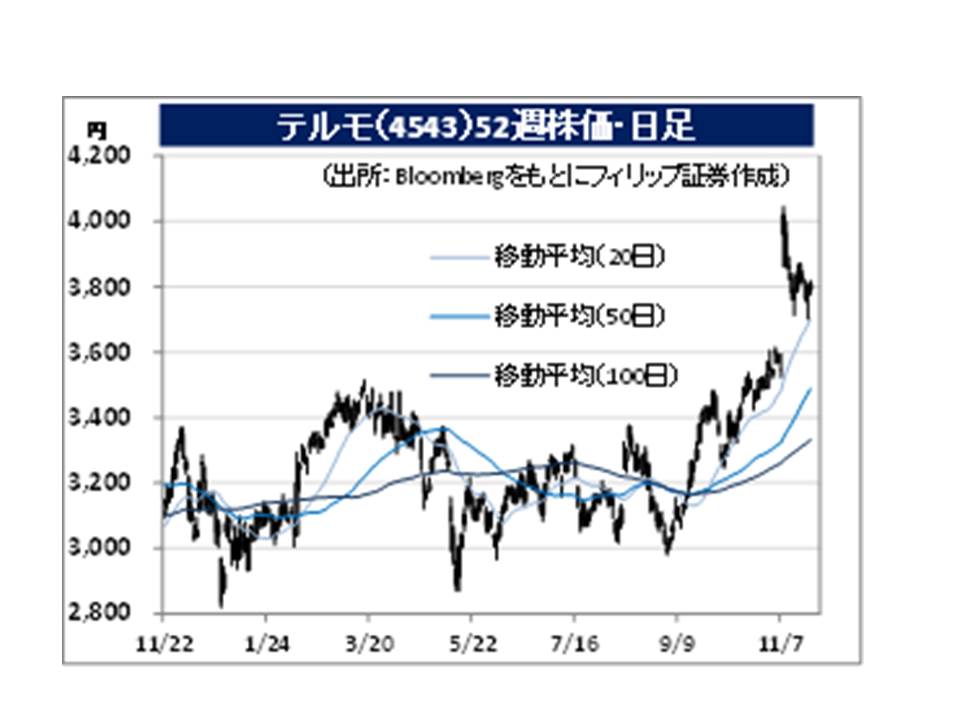

・Founded in 1921 for the purpose of manufacturing thermometers in Japan due to a stop in thermometer imports as a result of WW1. Carries out the manufacture and retail of various disposable medical equipment, pharmaceutical / nutritional foods, blood bags, artificial cardiopulmonary systems, catheter systems, artificial blood vessels, the peritoneal dialysis-related, blood sugar measurement systems, ME equipment and electronical thermometers, etc. Has expanded to over 160 countries.

・For 1H (Apr-Sep) results of FY2020/3 announced on 7/11, sales revenue increased by 7.8% to 307.278 billion yen compared to the same period the previous year, operating income increased by 24.3% to 59.15 billion yen and net income increased by 32.7% to 45.711 billion yen. Their cardiovascular company has performed strongly, and the launch of direct sales of stent grafts and the cerebral aneurysm sac device, “WEB”, served as the driving force. A double digit growth was also observed in the TIS business.

・For its full year plan, sales revenue is expected to increase by 5.9% to 635 billion yen compared to the previous year, operating income to increase by 2.2% to 109 billion yen and net income to increase by 1.9% to 81 billion yen. The content announced on 9/5 remains unchanged. On 20/11, the company decided to acquire the US medical technology startup, Aortica Corporation, and aims to contribute to “personalised medicine” involving aortic diseases.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: