Report type: Weekly Strategy

“Maritime Transportation, Warehouse and Iron & Steel Stocks in the Omicron Fears Market”

The new COVID-19 variant (Omicron) detected in South Africa was reported in Japan on 26/11, which cast suspicion on immune escape that evades existing vaccines due to it having greater transmissibility than the Delta variant and having many mutations. There has been an increase in price fluctuation in major financial markets, such as the U.S. and Japan stock markets and the WTI Crude Oil futures market, which were flung up and down as it went from rejoicing to worrying over information on Omicron.

While the “short selling ratio” tabulated by JPX shifted generally in the first half of the 40% level from the start of the month to the 25th, after rising sharply to 51.5% on the 26th, it then also shifted to a high level in the range of 46.6-47.8% from the 29th to 2/12. The “up-down ratio”, which is the index that monitors a sense of overheating based on the ratio of the number of stocks with a price drop and the number of stocks with a price rise in the market, also shifted to under 80% from 24/11 onwards and reached under 70% on 2/12, which is said to be the rock-bottom zone which has oversold. Also, in the Japanese stock market on the 3rd, stock prices rebounded via buybacks focusing on land transport sector (54.9%) and air transport sector (56.5%) stocks, which had high short selling ratio levels on the 2nd.

If the governments of each country are to decide on implementing movement restriction devices one after another as prevention or measures against the spread of the Omicron variant, we can imagine that there will be an increase in skyrocketing container freight rates in maritime transportation. Also, since there has been stagnant container loading and unloading at harbours due to reinforcements in each country’s epidemic control system, we can also expect a rise in storage demand in freight warehouses. In that sense, we can likely say that key stocks among warehouse stocks and maritime transportation stocks, which have been shifting in a steady rising trend up to around September this year, would be those that are able to have relatively good business performance forecast under the uncertain circumstances due to fears of Omicron infection. For warehouse stocks, there ought to be considerations on the possibility of a broadening of industry reorganisation led by maritime transportation companies that are aiming for business diversification, such as Daibiru (8806) and Utoc (9358) becoming wholly-owned subsidiaries via a TOB from Mitsui O.S.K. Lines (9104).

Regarding economic downturn concerns following movement restrictions by governments, beginning with the large-scale infrastructure investment plan that has already been passed and signed in the U.S., there is a high possibility that there will be advancement in the implementation of infrastructure investments worldwide focusing on the renewal of lifestyle-related infrastructure that has severely deteriorated. In that sense, there will likely be focus on iron and steel stocks. Nippon Steel (5401) and JFE Holdings (5411) have raised a policy of a consolidated payout ratio of 30%. For Nippon Steel, their full year forecast EPS (earnings per share) is 565 yen and their actual results interim dividend is 70 yen. For JFE, their full year forecast EPS is 434 yen and their actual results interim dividend is 60 yen. There will likely be greater expectations of a dividend increase in both companies. Since there are expectations of a reduction in crude steel production in Chinese enterprises following China’s policy on “phasing out coal”, the unlikely occurrence of a price collapse in iron and steel due to low cost exports will also likely be beneficial.

In the 6/12 issue, we will be covering Nippon Suisan Kaisha (1332), M3 (2413), Nippon Kodoshi (3891) and Fukuoka Financial Group (8354).

・Established in 1943 after being founded by Ichiro Tamura in 1911 in Shimonoseki. Operates the fisheries business, such as fishing and fish farming, the foodstuff business, such as chilled and processed foodstuff, the fine business, such as medical raw materials and functional foodstuff, and the distribution business, such as cold storage warehouses.

・For 1H (Apr-Sep) results of FY2022/3 announced on 5/11, net sales increased by 13.1% to 339.611 billion yen compared to the same period the previous year and operating income increased by 2.0 times to 13.866 billion yen. Although the processed Alaska pollock business in North America and domestic fishery struggled, there was improvement in the domestic and overseas fish farming business under the fisheries business, and commercial and industrial retail performed strongly in the West for the foodstuff business.

・Company revised its full year plan upwards. Net sales is expected to increase by 9.4% to 673 billion yen compared to the previous year (original plan 642 billion yen) and operating income to increase by 36.1% to 24.5 billion yen (original plan 20 billion yen). A reinforcement in constitution in the domestic fish farming business and chilled business is expected. In the 2021 product ranking by Nikkei Inc. announced on 2/12, “frozen food economy” was elected as the Komusubi on the west side (fourth rank in sumo). With the increasing presence of frozen food on dining tables in households, Nissui Frozen Foods hold the top share in the domestic market.

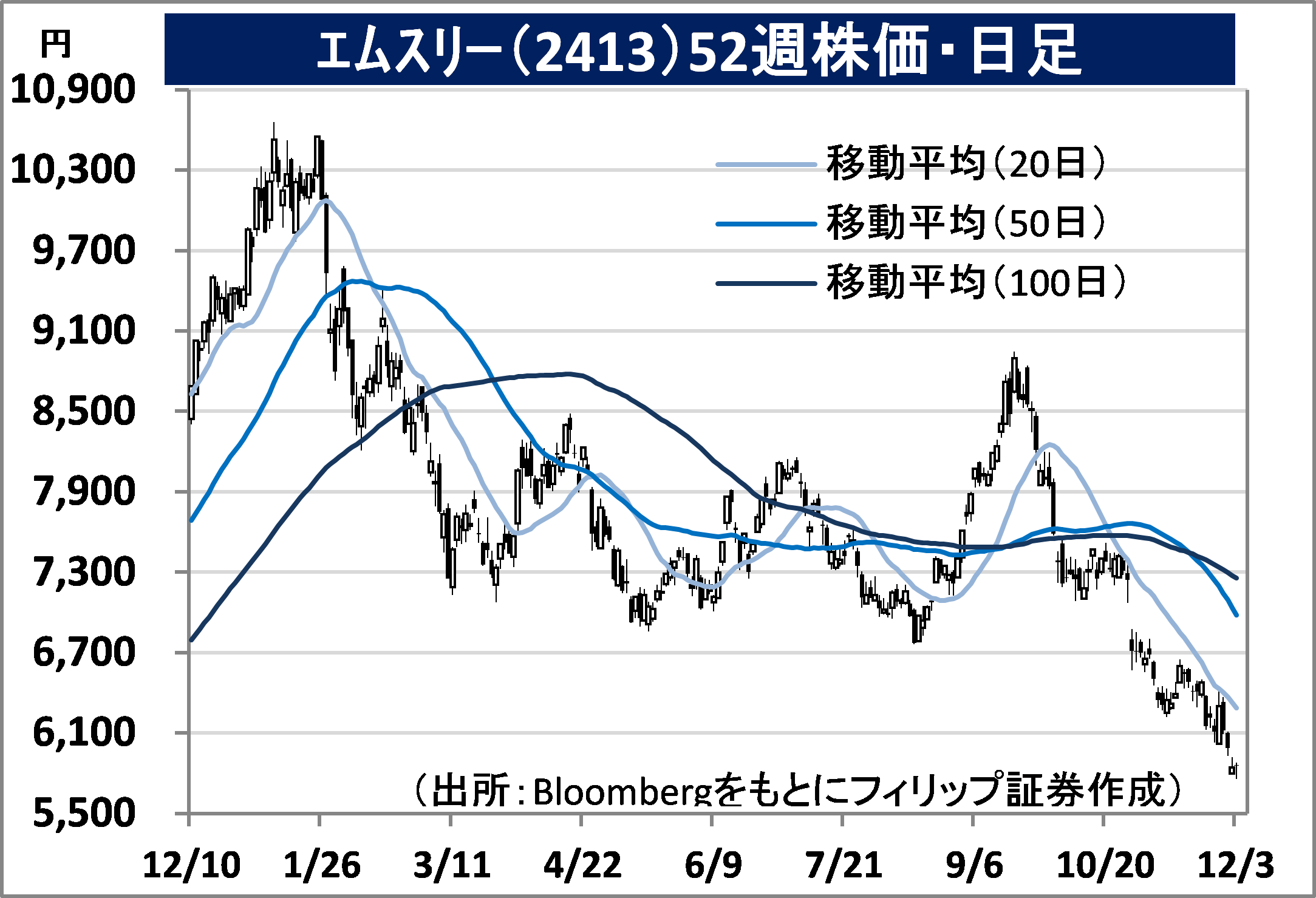

・A related company of Sony Group (6758) that established in 2000. Operates healthcare practitioner platforms, such as “Doctors.net.uk” in the UK, “MDLinx” in the U.S. and “m3.com”, a specialised website for healthcare practitioners used by over 300,000 member doctors in Japan.

・For 1H (Apr-Sep) results of FY2022/3 announced on 27/10, sales revenue increased by 30.2% to 97.647 billion yen compared to the previous period and operating income increased by 2.6 times to 61.941 billion yen. In addition to a 24.2% increase in revenue in their mainstay medical platform business involving marketing support for pharmaceutical companies, the expansion of their COVID-19 vaccination support project contributed to pushing up business performance.

・Their full year company forecast is undisclosed due to the inability to reasonably calculate the impact from the global spread of COVID-19. The number of doctors registered in the doctors’ panel and the website for healthcare practitioners operated globally by the same company’s group have reached a total of approx. 6 million. With growing concerns on the spread of the COVID-19 Omicron variant, the policy of each country in the world is to raise their alert level and reinforce PCR and antibody testing. There will likely be increased demand for the company’s businesses.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: